KPN Rings the Bell for Round Two in European Telecoms

(Bloomberg Opinion) -- Round one of the great activist push into European telecoms is ending. Gear up for round two.

The news last week that Canada’s Brookfield Asset Management is considering an approach for former Dutch national carrier KPN NV bookends a 12-month period which saw a range of European carriers targeted for their attractive network businesses. Within the 50 billion euros ($57.2 billion) of telecom deals in Europe last year, the biggest noise came from activists sensing an opportunity to push often heavily leveraged companies to sell cell towers and fixed networks.

Their aim is to try to benefit from an anticipated surge in demand for data. This is the year when we’ll have a good idea if they can make it to the exit.

At this point, any fund still wanting to get into the space will find a shortage of big, realistic transactions.

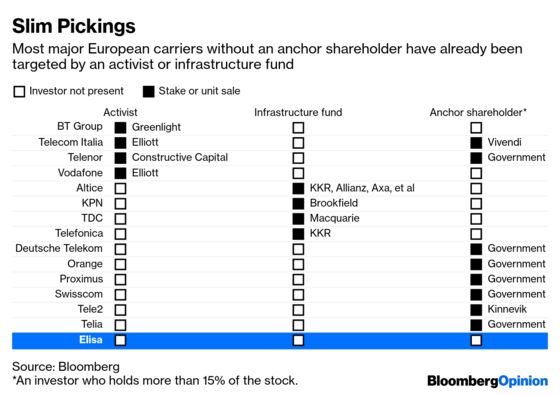

So Finland’s Elisa Oyj may be one of the last opportunities. Though the state and a series of pension funds hold close to 20 percent of the stock, a deal could be doable for an infrastructure fund that forms the right alliances.

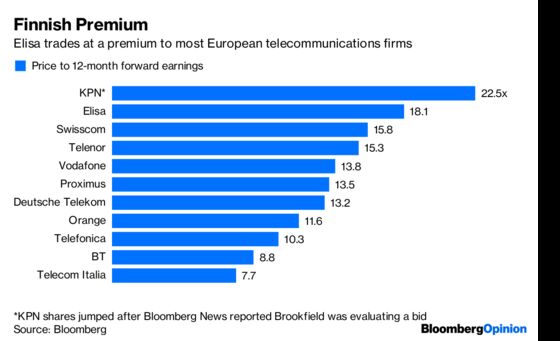

But there are downsides. Finland relies more heavily on mobile broadband, which generates less reliable long-term returns than a fixed service, since customers can switch providers a lot more easily. And Elisa is already valued more generously than most of its peers, trading at 18 times forward earnings, compared with the 14 times multiple of Vodafone or the 13 times of Deutsche Telekom.

Unless a bidding war for KPN develops, the infrastructure funds that still want a piece of the action have to play a waiting game.

And the activists won’t necessarily have an easy time. True, Vodafone seems open to the possibility of selling a stake in its cellphone towers. But Elliott is mired in a battle with Vivendi SA over the future of Telecom Italia. BT is loath to sell its OpenReach network business. Agitators facing a long slog to make their investments pay can create a serious distraction for management that weighs on shares, and there’s no guarantee of an end result that will lure would-be buyers.

However, if they are successful, then a slew of assets could become available this year. The problem is, picking them up could be costly, because the flurry of deals looks to have inflated valuations.

When KKR bought a 40 percent stake in Telefonica’s towers back in 2017, the deal implied an enterprise value of 11 times Ebitda. By the time the U.S. investor bought a stake in Altice’s equivalent French business in June, it had to pony up the cash for an implied enterprise value of 18 times Ebitda. Altice will be hoping to get a hefty premium for the slice of the fixed network business it’s selling in Portugal.

As the dust settles on 2018’s dealmaking, there might be further opportunities for infrastructure funds. But with premiums creeping up, and skepticism from carriers over the benefits of selling networks, the funds will need both patience and a hefty checkbook.

--With assistance from Elaine He.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.