Best Coronavirus Response? QE Plus Infrastructure Spending

(Bloomberg Opinion) -- The economic threat from the coronavirus pandemic is profound. Stocks have plunged, oil prices have tumbled, the entire yield curve has fallen below 1% for the first time in history, and the country may already be in recession.

Boosting the economy will be difficult, because macroeconomic theory and policy are not set up to deal with pandemics. The U.S. economy hasn’t been rocked by a major disease outbreak for more than a century; instead, recessions have come from oil shocks, interest-rate increases or financial crises.

The simplest macroeconomic theory -- and the one that most people, on some level, use to think about the business cycle -- is called the AD-AS model. Those letters stand for “aggregate supply” and “aggregate demand.”

According to this simple theory, when the economy is hit with a negative shock to supply -- such as the oil price hikes of the 1970s -- growth and employment fall while inflation rises. This makes intuitive sense; if it gets harder to produce stuff because energy is more expensive, that will hurt the economy but also raise the prices of consumer goods. Meanwhile, a demand shock, like the financial crisis of 2008, will also slow growth and raise unemployment, but instead of raising inflation it will reduce it. When businesses stop investing and consumers stop consuming, prices fall.

But this simple model might not be an accurate description of reality. Many theorists have devised more complex models in which there’s no clear difference between a supply shock and a demand shock. For example, knowing that supply will be disrupted in the future can lead to a fall in demand today.

It’s also not clear where a pandemic like coronavirus falls on the old supply-demand dichotomy. On one hand, production will be harder to sustain amid supply-chain disruptions and people staying home from work. That could look like a supply shock. But the declines in financial markets, and a general loss of economic confidence, could make coronavirus look more like a demand shock.

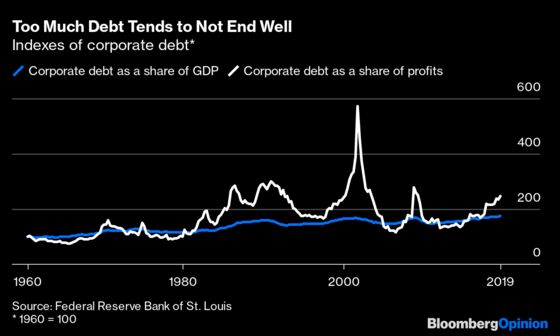

The biggest demand shock could be a financial crisis. During the last few years, corporations have built up a lot of debt, much of it in the form of risky leveraged loans. That debt was sustained by record earnings:

But coronavirus will eat into many companies’ bottom lines, as consumers avoid restaurants, stores, theme parks and other public places. That could lead to waves of defaults, which would put a burden on banks and other financial companies.

So saving the economy from a pandemic will be tricky. As of now, falling interest rates and oil prices look like a drop in demand, so the impulse will be to give money to consumers to get them to keep spending. That won’t hurt, but it might not make customers any more likely to go shopping, use transit or go out to eat when there’s a pandemic brewing. They might increase spending on home deliveries -- Amazon will likely be pleased -- but companies dependent on foot traffic will be hurt, meaning corporate defaults could spike.

Monetary policy can be used to allay the danger of a new financial crisis. Interest rates are already very low, but the Federal Reserve can use quantitative easing to buy corporate bonds and loans. This will lower corporate borrowing costs, allowing companies whose earnings are hit by the pandemic to borrow to weather the storm. In addition, it will take some risky debt off of financial institutions’ hands, reducing the danger of a 2008 repeat. To some, this will seem like a stealth bailout that rewards risky borrowing -- and to some degree, it is. But banks couldn’t easily have foreseen something like coronavirus, and they shouldn’t be punished for it.

Meanwhile, the best kind of fiscal stimulus remains the physical kind. Direct government spending on things such as infrastructure is even better at fighting recessions than mailing people checks. Furthermore, because the U.S. now needs a lot of infrastructure repair, this will boost supply as well as demand. And coronavirus has exposed major weaknesses in U.S. public-health infrastructure that could also benefit from an influx of federal and state dollars.

When it comes to infrastructure spending, timing matters a lot. Public health should be upgraded immediately to fight the pandemic. But now is probably not the safest time to send a lot of construction workers out to fix roads. And if supply-chain disruptions eventually do turn coronavirus into a supply shock in six months or a year, it will be good to have a positive supply shock such as infrastructure construction ready to fight it.

So a combination of QE and spending on public health today, followed by the promise of a major infrastructure push as soon as the pandemic threat has passed, would be a wise approach to fighting the impact of this novel economic shock.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2020 Bloomberg L.P.