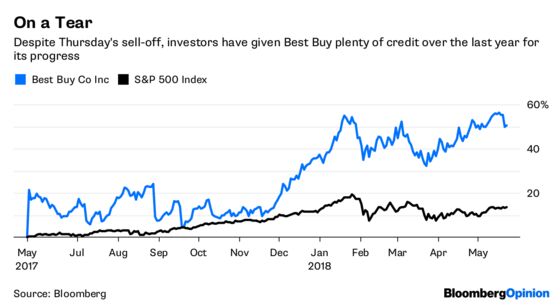

(Bloomberg Opinion) -- Best Buy Co.’s first quarter shaped up to be something of an encore to its robust holiday season. Investors, though, aren’t exactly cheering.

The big-box electronics and appliance giant reported Thursday that comparable sales rose 7.1 percent over a year earlier in the quarter, far higher than the 2.9 percent growth analysts had estimated. Adjusted earnings per share of 82 cents also surpassed expectations. But the strong quarter didn’t prompt the company to increase its full-year guidance, and so the stock, which initially popped in early trading, reversed course.

The restrained outlook effectively signaled to investors that they shouldn’t get used to the roaring performance they’ve become accustomed to lately. Isn’t it kind of obvious, though?

Best Buy investors have heard this sober talk before. Last year, when the company posted a 5.4 percent increase in second-quarter comparable sales, CEO Hubert Joly said investors shouldn’t consider such growth that to be “a new normal.” The truth is, the retailer is largely out of turnaround mode and is back on steady footing, so it makes sense that it’s no longer going to grow like it was when it was digging out of a hole.

Even with today’s declines, the stock is not far off all-time highs. And Best Buy shares had risen more than 50 percent in the past year through Wednesday’s close. So maybe investors got ahead of themselves. But it’s still a positive story.

Importantly, the financial outlook that management laid out last fall as part of its Best Buy 2020 strategy still looks plenty attainable.

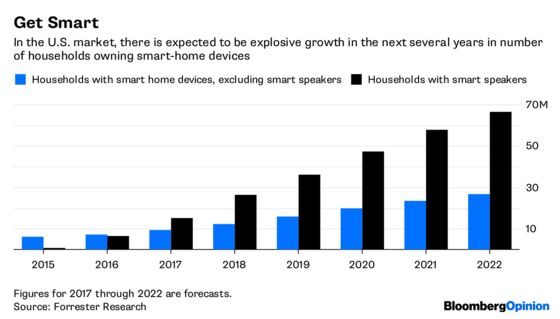

The adoption of smart-home devices is expected to grow explosively over the next several years, and Joly has positioned Best Buy well to tap into that opportunity. The retailer has already outfitted its stores with enhanced smart-home areas and has added 1,500 store employees that are specifically focused on this category.

In general, the emerging smart-home business is one where Best Buy’s ongoing focus on customer service should prove powerful. While many consumers are now on a rote replacement cycle with smartphones or laptops, smart-home gadgets and systems are new and confusing. It’s precisely the kind of highly considered purchase you’d want a knowledgeable staffer to guide you through.

Meanwhile, Best Buy is prudently putting increased emphasis on services, such as with offerings like its recently-launched Total Tech Support membership. For $199 a year, participants can get help with all of their gadgets, regardless of whether they were purchased at Best Buy. That program follows the debut of Best Buy’s in-home advisers, who will visit a customer’s house free of charge and offer a consultation on projects such as setting up a home-theater system.

Experiences and services are exactly the kind of thing that will make Best Buy stand out from its competition, and burnish its reputation as a place to go when you want real expertise.

Wherever Best Buy shares end up today, one thing is clear: The company remains in far better shape than it was five years ago, and is holding up better than many of its rivals in a changing retail environment.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

©2018 Bloomberg L.P.