Foreigners Like U.S. Debt As Much As They Ever Have

The idea that international investors are shying away from Treasuries is a good argument that falls flat in light of evidences.

(Bloomberg Opinion) -- There is no shortage of the threats that could push interest rates even higher from here, from the rapidly expanding U.S. budget deficit to the Federal Reserve’s hawkish leanings to even the European Central Bank’s plan to start tapering its bond purchases by the end of the year. Also, some would argue that the economy is doing well enough to provoke at least a bit more inflation. And then there’s the crowd that says foreigners are shying away from U.S. debt.

The last one is a good argument that falls flat when encountering a broad array of evidence suggesting that foreigners have been buying, are likely to continue to buy, but are being crowded out by other buyers. The upshot is that while $1 trillion budget deficits for the foreseeable future are scary for a variety of sound reasons, the lack of demand, especially on the foreign front, isn’t one of them. That should reassure markets, especially after the U.S. Treasury Department said Monday that government borrowing this year will more than double from 2017 to $1.34 trillion as the Trump administration finances a rising budget deficit.

First consider the motivation, the Fed is hiking, which has and will give support to the dollar. Also, the very high rates in the U.S. relative to the rest of the developed world remain a very compelling enticement. Second, Europe’s geopolitical woes, from Brexit to Italy’s budget and German politics, hardly make for a confident currency or bond stance. And strange as this may sound — relatively speaking — President Donald Trump’s penchant for creating geopolitical jitters hasn’t inhibited foreign investors — or domestic buying for that matter — which I’ll suggest is something of a surprise. His trade policy is inflaming domestic inflation, but between that and the deficit-boosting tax plan, it seems reasonable for the Fed to counter with a return to neutral rates or beyond via more tightening, which should further bolster the dollar’s appeal to foreign investors.

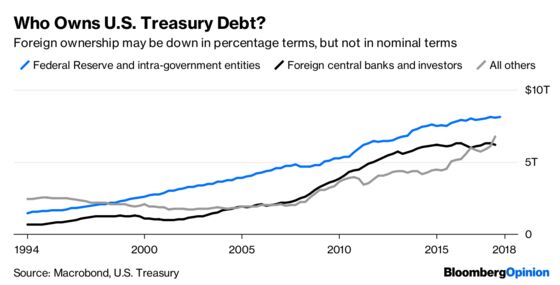

Let’s look at this in terms of flows. The chart below shows who owns Treasuries. Foreign ownership is flat at $6.2 trillion, or 47.8 percent of privately held debt. Although that’s down from 59 percent in 2014, foreign ownership is flat in nominal terms. This is mainly due to rising demand a category of buyers dubbed “other” as well as purchases by mutual funds and governmental entities including the Fed. Foreigners are not shying away; others have just been more assertive.

I don’t see these trends changing. If anything, with somewhat higher yields will make Treasuries that much more competitive with, say, the S&P 500 Index dividend yield of 1.80 percent and foreign rates in general. Plus, we are at a stage late in the cycle where stocks are showing some sign of anxiety and a simple rebalancing that favors bonds seems prudent, especially for pension funds.

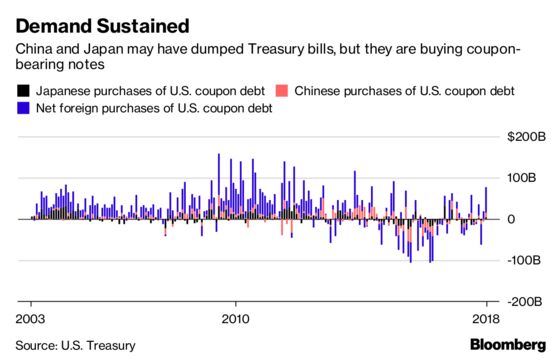

Yes, the latest Treasury International Capital, or TIC, report from earlier this month showed that overall holdings of U.S Treasuries by America’s two biggest foreign creditors — China and Japan — were down in in August, that’s a half-empty view. Although they cut their holdings of Treasury bills, China and Japan actually bought Treasury notes and bonds, which seems like a bullish view. China bought almost $9.44 billion of notes and bonds, while Japan purchased $4.45 billion in its most active month since June 2017. Overall, foreign investors bought a whopping $63.1 billion of coupon-bearing Treasuries in August, the most in more than three years.

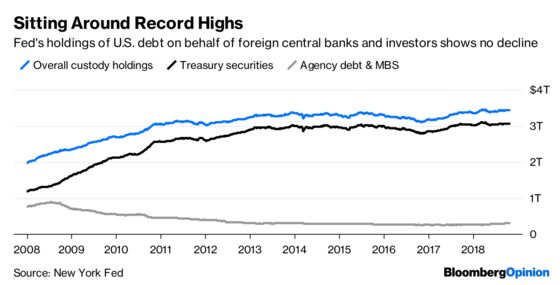

Further evidence of overseas demand can be seen in the Fed’s weekly custody holdings. At $3.43 trillion, they’re pretty right around record highs. And then there’s Japan’s Ministry of Finance statistics on Overseas Investments in Notes and Bonds. There, the six-week moving average is at $7.92 billion. It is possible Japanese investors were buying other markets such as Italy or Turkey and not the U.S., but that’s unlikely.

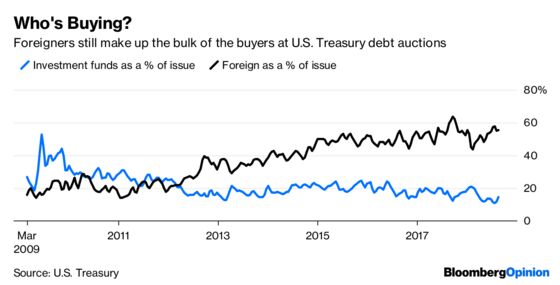

To be fair, a somewhat bearish case can be made of foreign activity if you’re dissecting Treasury auction participation. Even there, though, participation hasn’t diminished outright but only in relative terms. In other words, due to the increasing auction sizes, foreign buying has come off a very little bit from three to five years ago, and has held quite steady in the last two years. That’s because of rising domestic demand.

We should be worried about higher budget deficits because at some point in our lives, or our children’s lives, they will have to be paid for somehow, which means higher taxes and/or less spending, which will ultimately constrain economic growth. That’s both true and apolitical. But for now, the demand seems ample and will constrain the level to which interest rates will rise.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Ader is the former chief macro strategist at Informa Financial Intelligence and held similar roles at CRT LLC and RBS/Greenwich Capital. He was the No. 1 ranked U.S. government bond strategist by Institutional Investor magazine for 11 years, and was No. 1 in technical analysis for five years.

©2018 Bloomberg L.P.