(Bloomberg Opinion) -- The fearsome beast that’s menaced Australia’s financial services industry for the past year turns out to have been a paper tiger.

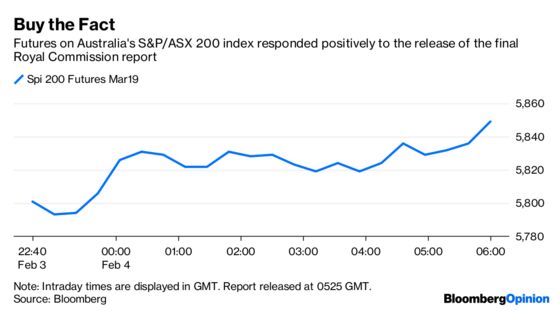

The final report of the country’s Royal Commission into misconduct in the sector will be a relief for bank investors. Futures on the S&P/ASX 200 index — the only immediate way to take a wager on the news, given the report’s release after equity markets closed — immediately jumped as much as 0.3 percent. When you consider that the companies under scrutiny make up only around a quarter of the benchmark, that’s significant.

To be sure, there are significant reforms embedded in Commissioner Kenneth Hayne’s 76 recommendations, which the government has promised to act upon. At bottom, the report is a full-frontal attack on the welter of intermediaries who sell mortgages, retirement accounts, insurance and other financial products to Australian consumers, often with ill-disclosed conflicts of interest.

Borrowers will have to pay the fees of mortgage brokers, a provision that ought to undermine the big banks’ stranglehold on distribution which has allowed them to maintain and expand market share in home loans despite offering more costly products than their competitors.

In superannuation (Australia’s system of employer-funded compulsory retirement savings) there’ll also be an end to the system of duplicate accounts, whereby savers can end up with new pension fund managers each charging their own set of fees every time they move jobs. “Fees for no service” — a practice that got a lot of airing during the commission hearings, and that is as egregious as it sounds — will be outlawed.

Still, a law is only as strong as its enforcement, and it’s there that the report falls down. One of the core issues behind much of the misconduct detailed in Hayne’s hearings over the past year has been the remuneration structures in financial companies. The push to increase revenues and shareholder returns has permeated financial companies from top to bottom. For front-line sales people, that’s resulted in strong incentives to get a sale, regardless of whether it’s done honestly.

The remedy for this deep-seated structural issue will be regular reviews of remuneration systems overseen by the Australian Prudential Regulation Authority, the government agency tasked with overseeing fiscal stability. Perhaps that will be sufficient, even in the presence of all APRA’s other responsibilities. But one of the most resounding themes of this report and the interim one in September is the conviction that simply exhorting people to be more honest will never succeed when their interests are better served by dishonesty.

More fundamental reforms were avoided. Companies won’t be forced to spin off the peripheral businesses with which they’ve had conflicts of interest, despite the fact that a fire sale of bundled life insurance and asset management units is already underway. Nor will there be an attempt to further encourage more responsible mortgage lending and underwriting.

Regulators that have historically been captured and misled by the companies they’re tasked with supervising will now bear the lion’s share of the responsibility for policing future misconduct. Perhaps the flurry of legislation that’s been passed to address this weakness in recent years will help, from laws to hold senior executives to account and a tougher range of penalties for the Australian Securities and Investments Commission, to a fresh inquiry into the superannuation system published just weeks ago.

Ultimately, though, preventing the weeds of misconduct from growing depends not on design, but on the vigilance of the gardeners. Given the way the current government cut real-term funding for ASIC to a 15-year low even in the midst of this Royal Commission and the opposition Labor party’s more laissez-faire attitude when it was last in government, it’s hard to feel confident that the current desire for tougher regulation will persist.

As Hayne wrote today, “Misconduct will be deterred only if entities believe that misconduct will be detected, denounced and justly punished.” The jury is still out on whether that’s going to happen any more than in the past.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.