(Bloomberg Opinion) -- Why have Australia’s big four banks been suffering over the past year? Is it the Royal Commission into misconduct in the financial sector, due to publish its final report after local markets close on Monday? Or is it the effect of a housing market entering a once-in-a-generation slump?

While the real answer is probably a mixture of the two, it’s worth trying to pick apart the factors if you think commissioner Kenneth Hayne is set to deliver a fatal blow to one of the world’s most richly valued banking industries.

The share prices of major banks move closely in line with Australia’s housing market: Westpac Banking Corp. and National Australia Bank Ltd. show a correlation of 0.87 with CoreLogic Inc.’s index of prices in the country’s five largest state capitals, while Australia & New Zealand Banking Group Ltd. is on 0.61 and Commonwealth Bank of Australia on 0.46 (a figure of 1 implies a perfect correlation, with 0 suggesting no relationship).

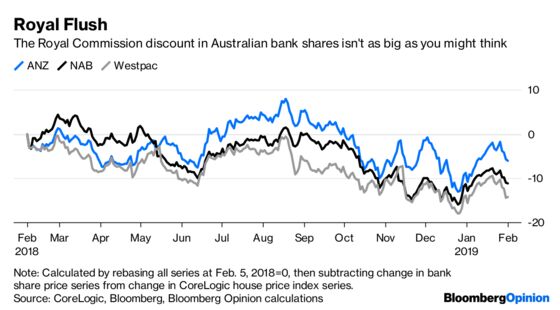

Another rough way of visualizing this is to assume that a fall in the housing index will correspond to a fall in share prices, and strip out the two effects. Do that exercise with Commonwealth Bank shares, and you have a picture of a company that suffered a dramatic “Royal Commission discount” whenever hearings were going on, before reverting to the housing market-implied mean whenever the noise died down.

ANZ’s share price weakness, similarly, can largely be explained by real estate, with Westpac and National Australia Bank and Westpac suffering more dramatic effects.

That’s not nothing – and indeed, it’s probably not unconnected to the Royal Commission, since the lending drought that’s helping drive the housing slump is probably being fueled by banks that have become gun-shy under Commissioner Hayne’s scrutiny.

At the same time, it underlines the conclusions of his initial report: The problems besetting Australia’s financial-services industry have happened in spite of the existence of generally sensible black-letter regulation, not in its absence. Changing that will involve shifting the incentive structures, business models and cultures of the big banks and the agencies that regulate them – by no means a certain process.

What can we expect from Monday’s final report? It seems clear that the recommendations will focus on ways to fix those latter issues – from reducing incumbents’ hold on the distribution of mortgages, insurance products and retirement savings accounts; to beefing up Australia’s weak corporate regulators; to removing the culture of sales targets which appears to have underpinned much of the abuse chronicled in Hayne’s public hearings.

Most of that is likely to be implemented whichever government wins the federal election due by May, with the Labor opposition – which has led in opinion polls for almost three years – likely to put through the toughest set of measures. Still, any lasting damage to Australia’s financial sector will depend upon consistent enforcement by governments for years after the hearings of the past 12 months have been forgotten.

Right now, MSCI’s Australia financials index, a basket in which the big four banks constitute about three-quarters of the weighting, is at some of its lowest price-book multiples in a decade, and has all but lost its historic premium to the equivalent U.S. benchmark.

Anyone predicting an acceleration of that trend is forecasting a market that will be much harsher to Australian bank shareholders (and kinder to their customers) than the current one. Such an outcome is far more likely to result from the cracks spreading in Australia’s housing market than anything that will come out of this Royal Commission.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.