(Bloomberg Opinion) -- On the long list of challenges facing the European fund management industry, one issue can be crossed out, at least for the immediate future — the risk that Brexit will pull up the drawbridge that allow firms to sell and manage investment products across European Union borders.

The various regulatory bodies that oversee investment firms across the EU appear to be in agreement that the current arrangements will survive past March 29, when the U.K. is scheduled to leave the bloc. It’s a welcome — and unusual — outbreak of common sense as the Brexit process grows more convoluted with every passing day.

In a speech in Dublin last week, Central Bank of Ireland Deputy Governor Ed Sibley said he is confident that the memorandums of understanding required to maintain the status quo between the U.K. and the EU will be implemented by the departure date. “Firms that delegate portfolio management to the U.K. can have sufficient confidence that this will continue to be allowed,” he said.

That statement should bring a “sigh of relief” for the industry, according to Sean Tuffy, the head of market and regulatory intelligence for Citigroup Inc. in Dublin.

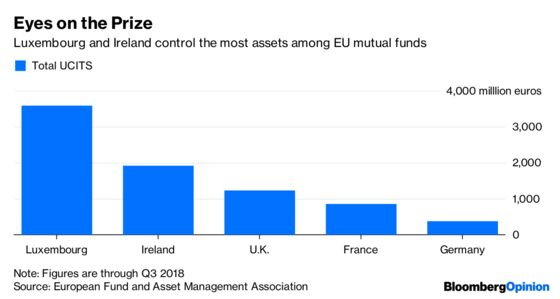

Investment firms have lobbied successfully against changes to the rules governing Undertakings for Collective Investments in Transferable Securities, the EU’s 10 trillion-euro ($11.4 trillion) equivalent of the U.S. mutual fund industry, a business dominated by funds listed in Luxembourg and Ireland.

Earlier this month, an attempt by the European Securities Markets Regulator to roll its tanks onto the lawns of domestic regulators was rebuffed by the European Parliament. ESMA had sought more control over so-called delegation rights, which allow funds to be listed and sold in one nation while the portfolios are managed in a different country. Lawmakers made it clear that national watchdogs will remain the arbiters of what’s acceptable in outsourcing those activities.

The world of finance, which barely featured in U.K. Prime Minister Theresa May’s proposals, has been quietly safeguarding itself from the consequences of Britain leaving the EU without a deal. Last month, Germany introduced draft legislation to allow U.K.-based institutions to continue to user their existing passporting rights through 2020.

And there’s been a similar extension in the derivatives market that should help London to keep its central role, for now. The European Commission has agreed that financial firms across the bloc will be able to use London Stock Exchange Plc’s LCH Ltd. clearinghouse for 12 months after Brexit.

What can possibly explain this unprecedented attack of logic and practicality, given that the entire Brexit process has thus far been characterized on both sides by short-sightedness, mistrust and muddled thinking?

Sibley, who handles regulation for the Irish central bank, gave a clue in his speech by referring to how London delivers “a very material amount of the financial services needs” of the EU. Barring a fund sold in Italy from being managed in London would deprive buyers of that investment product of the undoubted investment expertise that’s based in the City.

The current truce might not last. ESMA has already expressed its discomfort at having a large financial center on its doorstep but outside of its regulatory purview. If, as seems likely, London tries to soften its regulatory regime to give it a competitive advantage over the EU after Brexit, that unease may grow unbearable. And while French President Emmanuel Macron is more focused on fish than finance at the moment, Paris is likely to find the temptation to try and lure more of the euro-denominated fund management business away from the U.K. irresistible in the coming years.

It’s not all good news for the City. CME Group Inc. is moving its foreign-exchange forwards and swaps venue to Amsterdam from London, shifting about $15 billion of daily transactions. Cboe Global Markets Inc. plans to relocate most of its European equity trading, an $8 billion business, to the Dutch capital. And five of Europe’s biggest banks plan to move 750 billion euros of balance-sheet assets to Frankfurt, Bloomberg News reported on Wednesday.

But, for now, it looks like much of the investment-management industry has dodged the Brexit bullet. If only the rest of the negotiations were as pragmatic.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.