(Bloomberg Opinion) -- It’s only when the tide goes out that you find out who’s been swimming in the nude, billionaire investor Warren Buffett famously opined. And as the bull market in global stocks starts to ebb, asset management companies will find themselves dangerously exposed — with medium-sized firms the most at risk of finding themselves naked and shivering on the beach.

Investment firms have been living on borrowed time. When indexed back to 2007, profits grew by a staggering 20 percent in North America and Asia last year, and by 18 percent in Europe, according to a study just published by consultancy firm McKinsey & Co. The picture was flattered, though, as booming stock markets helped swell global assets under management by 11 percent to a record $88.5 trillion.

Those market gains, for example, added almost $12 billion to the U.S. profit pool, boosting it to $44.5 billion in 2017, the McKinsey study shows. Rising costs, lower fees and a shift to cheaper products combined to knock $6.7 billion off the total available. So take away the market gains, and the picture of the industry’s underlying profitability is very different.

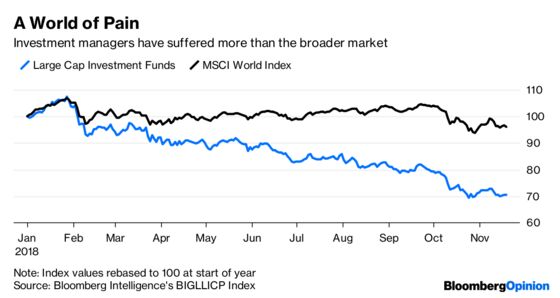

That poses a problem for this year. Equity market performance has been lackluster at best, with the MSCI World Index of global stocks down by a handful of percentage points in 2018. Benchmark U.S. indexes have eked out minimal gains this year; their counterparts in Europe and Asia are pinned firmly in the red.

But the industry headwinds from costs and fees remain as relentless as ever.

So it’s little wonder that investors have punished the shares of fund managers disproportionately. The Bloomberg Intelligence index of large investment firms, among them BlackRock Inc., Janus Henderson Group Plc and Amundi SA, is on track for its worst year in a decade after falling by about a third this year.

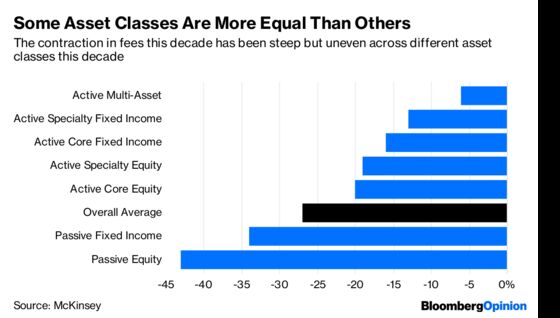

There are some bright spots. Fixed-income margins are holding up better than those on equities, and actively managed products in general are not seeing the same precipitous drop on fees as index trackers. So while the enthusiasm for low-cost passive investments continues unabated, the corresponding decline in fees across the investment universe is hurting some asset classes much more than others.

McKinsey calculates that $653 billion exited active equity funds in North America last year, with their passive brethren benefiting to the tune of $505 billion of inflows. Contrast that with the picture in fixed income, where inflows of more than $500 billion were split about evenly between passive and active strategies.

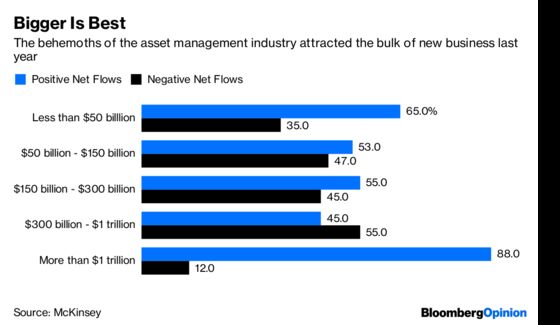

The report delivers cold comfort to the squeezed middle of the investment industry. The $1 trillion club continued to run away with most of the next asset flows; the next bracket down failed, on balance, to win new business last year, with the smallest subset of asset managers doing better than the ranks directly above.

McKinsey’s advice to those medium-sized managers echoes an oft-repeated refrain these days: Bulk up to achieve economies of scale, invest in technology to customize the products available to investors, and try to add more complex investment strategies that can command higher fees.

That’s sound advice. But when the biggest determinant of profitability for asset managers is completely out of their control — as the performance of the global stock market most assuredly is — you have to wonder how long some firms will continue to tread water before being washed away.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2018 Bloomberg L.P.