Drip. Drip. Asia’s Liquidity Taps Start to Gurgle

Whisper it for now, but we may see the region’s asset markets start to operate more smoothly in the second half of the year.

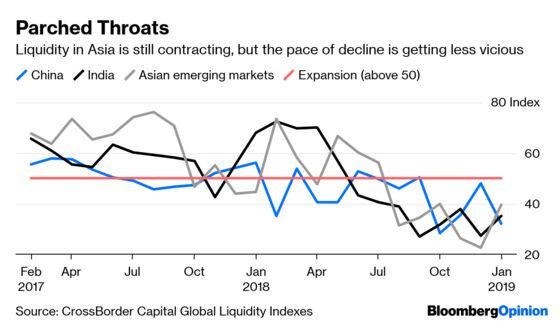

(Bloomberg Opinion) -- Last year marked the deepest deterioration in Asian liquidity conditions since 2008. While it’s nowhere close to over, the worst of the squeeze may have passed. The gears of the region’s asset markets could turn more smoothly in the second half of the year.

The signals are faint, so they’re easy to miss. In India, shadow banks’ liquidity crunch is still dangerously close to becoming an insolvency crisis for property developers. In China, economists’ forecasts of large-scale monetary stimulus are yet to materialize. Meanwhile, Chinese corporate defaults are also starting to look worrisome.

Look beyond the coming Indian elections and a keenly awaited China-U.S. trade deal, though, and there are reasons to turn cautiously optimistic. With inflation slowing, the dollar’s upward march temporarily halted, and the U.S. Federal Reserve hinting at a pause on its balance-sheet contraction, central banks in the region don’t have to worry that easing domestic monetary policies will collapse their currencies.

South Korea’s highest unemployment rate in nine years might give it room to delay tightening to beyond 2020. Countries such as Indonesia, which are still wisely putting financial-stability concerns ahead of growth, may also get more confident. Jakarta’s desire to squeeze domestic demand, which has resulted in an uncomfortably high current-account deficit, could diminish. That’s especially true if polls return the popular President Joko Widodo to power.

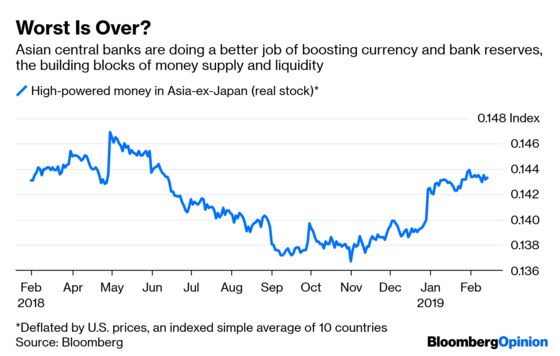

My measure of real Asian liquidity — the sum of currency and bank reserves deflated by U.S. prices — might already be signaling a turnaround in liquidity conditions.

Central bank liquidity is only part of the story. CrossBorder Capital Ltd. does a more comprehensive job of adding up public, private and international flows. It estimates that liquidity in global emerging markets improved in January to a rolling three-month average of $617 billion, a big change from six straight months of outflows through October. Could emerging markets be getting ready for money flows to resume? Analysts at the London-based research firm believe they might be.

It’s still a close call. Indian elections are unpredictable, and the ongoing trapeze act of simultaneous fiscal and monetary easing may lead to an accident if investors don’t like the makeup of the next government. Similarly, this week’s arrest of journalist Maria Ressa, a prominent critic of President Rodrigo Duterte, sparks fresh concerns about democracy and press freedom in the Philippines. Should the politics turn messier in the second half of the strongman leader’s six-year term, the central bank’s ability to ease monetary policy may be crimped. In Thailand, a handover of power from the ruling military junta to an elected government will pose its own challenge of credibility.

The trade talks between China and the U.S. are the most crucial unknown. China has been wary of interest-rate cuts in the event a weaker yuan gives President Donald Trump more ammunition in negotiations. An agreement would remove that concern. With both the U.S. and Chinese monetary policies leaning toward easing, last year’s liquidity drought in Asia would be conclusively over. However, if Washington pursues the more difficult aim of a broader accord encompassing trade, intellectual property theft, state surveillance and 5G supremacy, all bets will be off.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.