(Bloomberg Opinion) -- New year, new attitude. Despite all the forecasts of doom and gloom that rippled through global markets in December, investors across almost all asset classes and regions are in a much better mood in the early days of 2019. The MSCI All-Country World Index is up 8.18 percent since Christmas as volatility measures plummet. Oil entered a bull market on Wednesday. Junk bonds are soaring. Emerging-market currencies are the strongest since July. Heck, even pariahs such as Saudi Arabia and Turkey are able to borrow in the global debt markets with no trouble.

That’s not to say that last month’s sell-off was unjustified. Global growth is slowing, just not to the degree suggested by the rout in asset prices. The World Bank on Tuesday came out with its latest forecasts for global economic growth this year, and the surprise was that its estimate was reduced by just 0.1 percentage point, to 2.9 percent from 3 percent. Investors are also heartened by signs of progress in resolving the trade war between the U.S. and China. Global stocks rose more than 1 percent Wednesday as the U.S. wrapped up three days of midlevel talks with China in Beijing, noting a commitment by President Xi Jinping’s government to buy more U.S. agricultural goods, energy and manufactured products. On top of that, Federal Reserve policy makers seem a little less tone deaf to the messages sent by markets last month. Four Fed regional chiefs on Wednesday declared that the central bank can take its time to assess market turbulence and risks to the U.S. economy before adjusting monetary policy again, solidifying support for a pause from further interest-rate increases, according to Bloomberg News.

Of course, a lot could still go wrong for markets. The U.S-China trade talks could break down as more senior officials join the discussions. The U.S. economy could continue to be just strong enough to warrant another rate hake from the Fed in March, especially if oil continues to rebound and push up inflation expectations. Also, the U.K.’s exit from the European Union could become even messier, and the euro zone economy is looking shaky with Germany faltering. Nevertheless, there’s nothing like a dovish Fed to stir those animal spirits again.

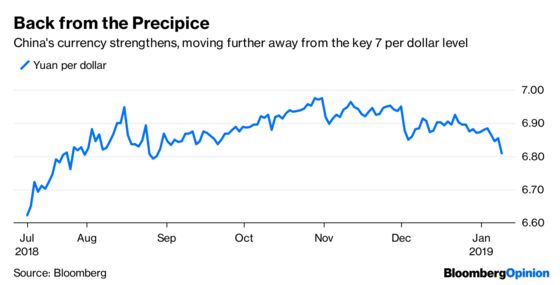

TRADE TALK PROXY

Perhaps the best proxy for investors’ assessment of the trade talks between the U.S. and China is the yuan. China’s currency rose on Wednesday to its strongest level against the dollar since August. At 6.8160 per dollar, the yuan has appreciated from 6.9757 in late October. That’s significant because many investors and strategists have warned that if it were to breach the psychologically important 7 per dollar level, it just might spark a flight of capital from China and throw global markets into a crisis-like tailspin. President Donald Trump and Xi have given their officials until March 1 to reach an accord on “structural changes” to China’s economy on issues such as the forced transfer of American technology, intellectual-property rights and non-tariff barriers. It’s a tight window in which to nail down deep changes to China’s economic model, some of which past U.S. administrations advocated for years and U.S. lawmakers on both sides of the aisle support, according to Bloomberg News’s Andrew Mayeda. Also supporting the yuan are some moves China has made to shore up its economy, including allowing banks to make more loans and other fiscal stimulus. The yuan’s gains helped propel the MSCI Emerging Markets Currency Index to its highest since July, rising some 3.56 percent from last year’s low in September.

OIL MAKES A COMEBACK

The 44 percent collapse in the price of West Texas Intermediate crude oil between early October and Christmas Eve had a lot to do with the negative sentiment in global markets in the final quarter of 2018. Yes, lower oil prices translated into lower gasoline prices, which Trump trumpeted as something akin to a tax cut for consumers. But what had investors on edge was the sense that the drop was due to a plunge in demand, a sign that maybe the global economy was weakening much faster than expected. Since then, though, oil has stormed back into a bull market, with West Texas Intermediate crude closing Wednesday at $52.36 a barrel to complete a 23 percent recovery, according to Bloomberg News’s Alex Nussbaum. One big reason for the rally is confidence that Saudi Arabia, Russia and other top exporters will follow through on last month’s pledge to slash production, with Saudi Energy Minister Khalid Al-Falih saying on Wednesday that the plan was on track. Progress in ending the U.S.-China trade war has turned the economic outlook brighter, adding to oil’s momentum, Nussbaum reported. Investors better hope that oil prices don’t get much higher because if they do, it could prompt bond investors to price in faster inflation. And if that happens, it could force the Fed to return to its hawkish leanings and decide to raise rates at its March meeting. That would quickly put a damper on animal spirits.

THE PRICE OF TURMOIL

Investors are in such a good mood that both Saudi Arabia and Turkey — the subjects of some rather unsavory news last year — were finding plenty of takers for dollar-denominated bonds they were offering. Saudi Arabia was selling $7.5 billion of debt in the first test of how much damage the brutal killing of Washington Post columnist Jamal Khashoggi has inflicted on investor appetite, according to Bloomberg News. Turkey was doing the same after its lira was the second-worst performer in emerging markets last year and the nation’s dollar debt generated a 5 percent loss after turmoil that followed U.S. sanctions over the detention of an American pastor and tensions over Syria. To be sure, the sales came with a relatively expensive sweetener to entice investors. In the case of Saudi Arabia, one $4 billion tranche, due in 2029, was set to price at a yield of about 175 basis points more than what investors can get on U.S. Treasuries. The spread on a $3.5 billion tranche of 31-year debt was 230 basis points. Both are about 25 basis points over Saudi Arabia’s existing yield curve, Bloomberg News reported. That translates into about an extra $371 million in interest the kingdom will have to pay over the life of the bonds. “Saudi is a good credit and in Turkey, if you take a step backward and look at the big picture, there has been more positive news than negative news,” Michael Bolliger, the Zurich-based head of emerging-market asset allocation at UBS Wealth Management’s chief investment office, told Bloomberg News.

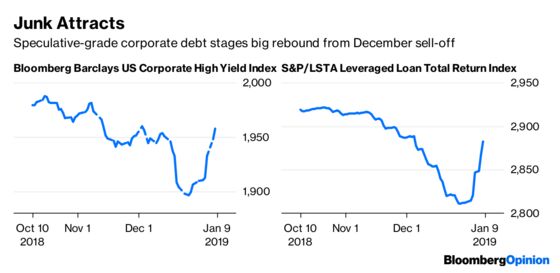

HIGH YIELD, HIGH RETURNS

Higher risk bonds globally are rebounding as well. Of 20 major parts of the global debt market tracked by Bloomberg, U.S. and global high-yield bonds are the best performers this month, generating returns of 2.53 percent and 1.77 percent through Tuesday, respectively. In the case of the U.S., returns have more than recouped their 2.14 percent loss in December. The boom extends to leveraged loans, or loans made to high-yield, high-risk borrowers. The S&P/LSTA Leveraged Loan Index has surged 2.46 percent this month, a monster move for a market that typically inches ahead month by month. “Valuations just got too cheap, unless you expect a recession and a spike in default activity,” Michael Marzouk, a portfolio manager at Pacific Asset Management, wrote in an email to Bloomberg News on Jan. 4, when the loan market enjoyed its best one-day rally in a decade. The SPDR Blackstone/GSO Senior Loan ETF, the largest actively managed loan ETF with ticker SRLN, posted the second-largest inflow in its history on Friday. Credit investors are clearly encouraged by the recent drop in volatility across riskier assets. The Cboe Volatility Index, known as the VIX or Wall Street’s “fear gauge,” has fallen eight of the past 10 trading sessions, dropping below 20 in Wednesday trading compared with 36 in mid-December. “It’s not at all a clear signal by any means, but it certainly is — I think — a reduction in panic,” Jay Pestrichelli, co-founder and managing director of ZEGA Financial, told Bloomberg News in reference to the money flowing back into high-yield corporate debt.

TEA LEAVES

Will the real Jerome Powell please stand up? When the Fed chairman addresses the Economic Club of Washington on Thursday, will he sound as hawkish as he did on Dec. 19, when he added to the turmoil in markets by largely dismissing the big drop in stocks and other risk assets as a referendum on the economic outlook? Or will he sound as dovish as he did on Friday, when he walked back those comments and said the Fed can be “patient” on monetary policy going forward in a nod toward shoring up market sentiment? It’s likely to be the latter, as the last thing Powell wants is to be viewed as a central banker who flip-flops on a whim, which would only upset markets that have come to thrive on certainty. But regardless, with the Fed’s target rate at the low end of what is considered neutral, markets will inherently become more volatile as the economic data waxes and wanes and Fed language responds to those changing conditions. Put another way, markets were relatively calm through 2016 and 2017 because the Fed’s plan was to get rates toward neutral as steadily as possible. Everyone knew what the Fed was going to do, when it was going to do it and by how much it was going to do it. There were no surprises. But now, investors can expect a lot more surprises from the Fed going forward, which may not be such a bad thing.

DON’T MISS

Gundlach Likens Buy-the-Dip Mentality to Crisis: Brian Chappatta

Saudi Arabia Is Set to Win Its Big Market Test: Marcus Ashworth

Aluminum Is the Market to Watch Closely in 2019: Jason Schenker

Maybe Trump Does Have Authority to Fire Powell: Stephen Mihm

Five Fiscal Messes India Can’t Blame on the RBI: Andy Mukherjee

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.