India Should Beware of Saudi Aramco's Billions

The country is already too reliant on imported crude. Cozying up to the Middle Eastern giant will only make matters worse.

(Bloomberg Opinion) -- It’s funny how friendly someone gets when they’re trying to sell you something.

Saudi Arabian Oil Co. is doing its best to make nice with one of its biggest customers. With the ink barely dry on the takeover of 70 percent of the country’s chemical giant Saudi Basic Industries Corp. and the issuance of its first-ever corporate bond, Aramco is looking to buy a stake in the world’s biggest oil refinery.

Indian billionaire Mukesh Ambani’s Reliance Industries Ltd. is seeking to sell as much as a quarter of its refining business for at least $10 billion and is entertaining offers from Aramco and Abu Dhabi National Oil Co., people with knowledge of the matter told Bloomberg News this week.

That represents quite a prize. Reliance’s Jamnagar refinery is about twice the size of the biggest U.S. plant, Aramco-owned Port Arthur, and is so massive that maintenance work occasionally skews India’s entire trade balance.

Trade is also the reason India should be cautious of Aramco’s embrace. The country has a dangerous addiction to imported crude, and it should be wary of getting too cozy with its dealer.

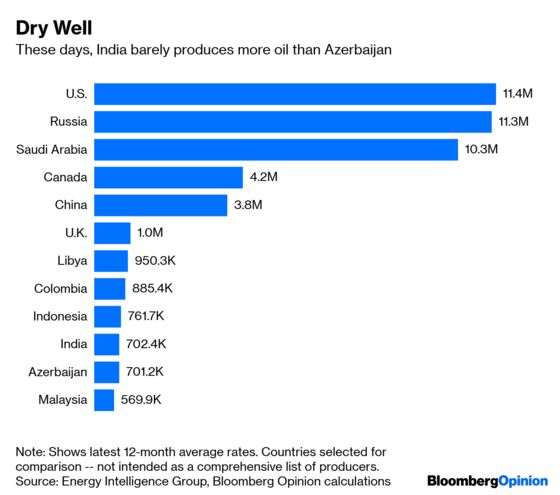

For more than a century, the rise of major economic powers has been fueled by petroleum. The U.S. is both the world’s biggest oil consumer and its biggest producer. The Soviet Union was built on its oilfields in the Caucasus and Siberia. While China has overtaken America as the biggest oil importer, it’s also the biggest producer outside the Middle East after the U.S., Russia and Canada.

India is different. The U.S. produces about 1.8 metric tons of oil a year per capita and even China manages 138 kilograms. India – at a far earlier stage of development than either country – ekes out just 30 kilograms. Production peaked all the way back in 2010, and shows no sign of recovery. Industrialization is an energy-intensive process. If India’s development is going to be powered by crude oil, it’s going to be buying a whole lot more from Aramco and its ilk.

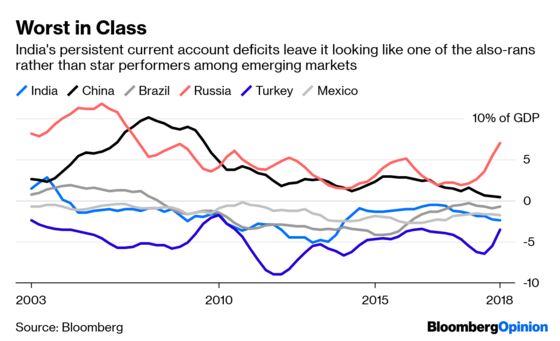

Such a future would pose some profound risks. Balance of payments crises are a recurring danger for emerging economies, and even at its current stage of development oil typically accounts for about a quarter of India’s imports. If prices spike higher – as, inevitably, they will from time to time – that’s good news for Riyadh, but potentially devastating for New Delhi.

When crude is averaging $85 a barrel – roughly the level at which Saudi Arabia can balance its budget, according to the International Monetary Fund – oil imports would reduce India’s gross domestic product by about 3.6 percentage points, according to a study this year by the Reserve Bank of India. Higher prices will also push up inflation and weaken the government’s fiscal position, the authors found.

At present, that dynamic is somewhat mitigated by the fact that about a third of India’s oil imports are re-exported as petroleum products, giving the country a natural hedge against rising prices. Jamnagar, for instance, produces almost exclusively for export, meaning that it probably makes a modestly positive contribution to the trade balance since oil products are more valuable than the crude they’re made from.

Should domestic consumption grow faster than export refinery capacity, though, India’s oil dependence will start taking a deeper bite out of its current account. In a worst-case scenario, a spike in oil prices could drive the country toward a balance of payments crisis like the one it suffered in 1991, when a splurge on oil imports over the previous decade resulted in New Delhi pledging its gold reserves as security for bailouts from multilateral lenders.

India is aware that its dependence on imported crude risks constraining growth. The government wants 30 percent of new cars and two-wheelers to be electric by 2030 and is already home to more than 1.5 million electric rickshaws. It’s also adjusted tax policies to encourage that transition. In a country at grave risk from climate change, whose cities are already choking on vehicle smog, reducing the reliance on imported fossil fuels is more than just an issue for the current account.

That goal isn’t an unrealistic one given the rock-bottom local cost of wind and solar. Still, no country has managed a low-carbon industrialization on this scale before, so it won’t be easy – and Saudi Arabia will be hoping it proves all but impossible. By promising to buy a chunk of Reliance and help fund a new $44 billion Jamnagar-sized refinery in western India, Aramco is counting on the country being unable to kick its self-destructive oil habit. Indians should hope that it’s wrong.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.