Aramco Can Do Whatever It Likes With Bond Money

Is it wise to lend money to a company that’s simply going to use it to pay its equity holders a fat dividend?

(Bloomberg Opinion) -- Is it wise to lend money to a company that’s simply going to use it to pay its equity holders a fat dividend? If it’s one of the world’s largest and most profitable businesses, the answer is probably yes.

Saudi Aramco is making its second big foray into the international bond markets with a bumper slab of five new bonds, ranging from three to 50 years in maturity. Expectations are that the giant oil producer will only raise about $6 billion, half the size of its hugely oversubscribed inaugural debt offering in April 2019. (My colleagues at Bloomberg Intelligence think a follow-up sale may be needed.)

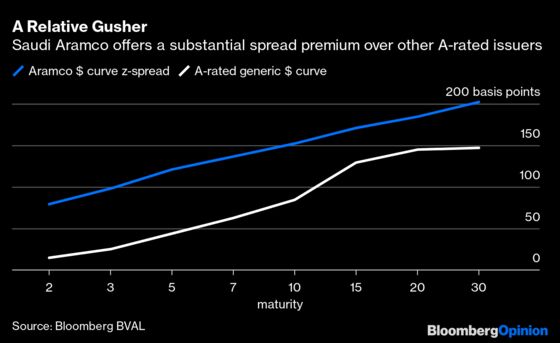

It will pay a slight premium to investors compared with what they get for the bonds of its majority owner, the Kingdom of Saudi Arabia. Last year Aramco debt priced at the same level as the sovereign. Regardless, it’s showing the market it can raise money easily.

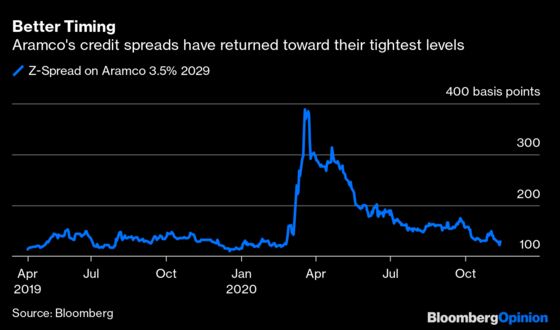

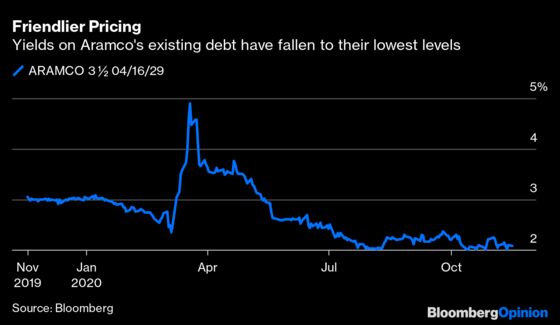

The world is a different place to 18 months ago, with the pandemic crippling economies and dragging the oil price down from $70 per barrel to about $40 now. But for bond investors hungry for yield, Aramco’s attractions remain. It’s a $2 trillion company with relatively little debt and the premium offered on the coupon — ranging from 140 to 230 basis points above the comparative U.S. Treasury — is too juicy to ignore.

During its record-breaking initial public offering last year, Aramco promised to pay $75 billion in annual dividends (the bulk of which will go to the Saudi state), and that’s proving to be an onerous pledge. With the company’s net income falling 45% in the third quarter to $11.8 billion, there’s a $7 billion or so shortfall in matching its dividend payout requirement. And this doesn’t look like a one-off: Fitch Ratings, which cut the company’s A-rating outlook to negative last week, expects Aramco will have negative free cash flow this year and next.

It also has to fund the $69 billion purchase of Saudi Basic Industries Corp.

Normally, the febrile oil market and that whopping dividend check would sound loud alarm bells. But debt holders can afford to look beyond the current relatively low crude price and still feel confident about the return of their capital — especially given the expected generosity of the yields on the new bonds.

The oil price has risen 20% in November, helped by Saudi Arabia ensuring OPEC supply cuts are largely adhered to, so Aramco’s timing of this issue is wise. The company wants to become a regular bond issuer, able to bring deals without too much regard to the oil price, so it makes sense to sell debt in 2020 — before liquidity dries up by the end of the year — to show it can build an established yield curve for investors (a suite of bonds at different maturities).

It will, however, keep having to pay that premium above its sovereign until its cash flow runs positive again.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.