Americans Feel a Little Down About a Decent Economy

(Bloomberg Opinion) -- In early 2017, a strange pattern began to appear. So-called soft economic numbers – surveys of business leaders and consumers -- started to look much more positive than the hard numbers of investment, growth and measures of business activity. Many wondered whether the optimism that people were expressing reflected their rational expectations of an improving economy, or whether it was merely a surge of partisan enthusiasm after President Donald Trump’s election victory.

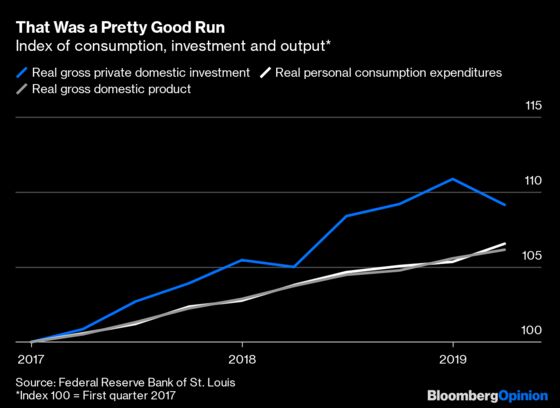

To make a long story short, the soft numbers won. Consumption, investment and economic output all rose as the U.S. recovery continued:

Unemployment, already low, fell even more, as the labor market shrugged off the last of its malaise from the Great Recession. And unlike in previous expansions, the less well-off saw their incomes grow as fast as those in higher brackets.

It seems very possible, therefore, that the optimists in 2017 actually knew that the economy was likely to keep powering along. Alternatively, their optimism itself may have been responsible for the continued expansion, their confidence becoming a self-fulfilling prophecy. A third, perhaps less likely possibility is that the optimism was unwarranted at the time, but that Trump delivered a round of tax cuts that boosted demand.

But 2 1/2 years later, the shoe is on the other foot. Perhaps due to Trump’s trade war, the soft numbers are heading down.

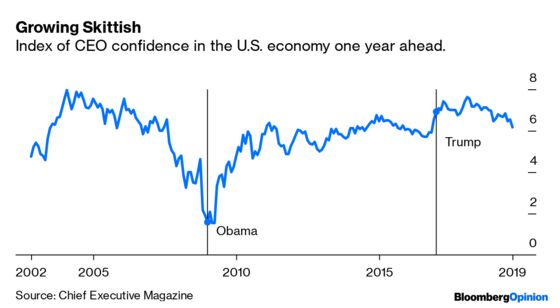

Chief Executive magazine’s index of CEO confidence in the U.S. economy, for example, has fallen below the level that prevailed just after Trump’s election:

Meanwhile, a widely watched survey of chief financial officers, compiled by Duke University, shows that half expect a recession in the next year – the most pessimistic they’ve been in three years.

Measures of small business and consumer confidence have fallen by less, but these too are showing signs of weakness. A survey compiled by the National Federation of Independent Businesses shows small-business optimism dropping, though not yet to pre-election levels. And the Conference Board's Consumer Confidence Index also just had the biggest monthly drop this year.

So while soft numbers are hardly catastrophic, they’ve taken a definite negative turn. These worries are no doubt one of the reasons why the Federal Reserve has begun cutting interest rates, a reversal of its previous plans to keep raising them.

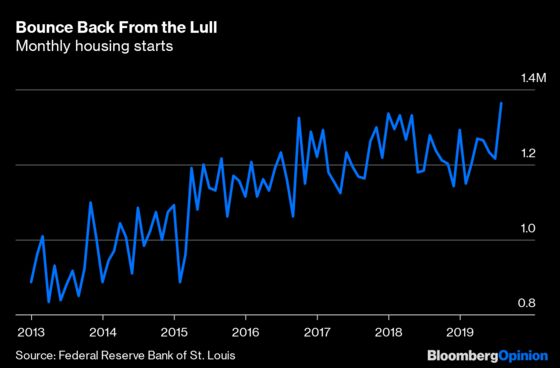

Interestingly, however, it’s now the hard numbers that are holding up. As my colleague Tim Duy points out, housing starts are rising, and had an especially good month in August:

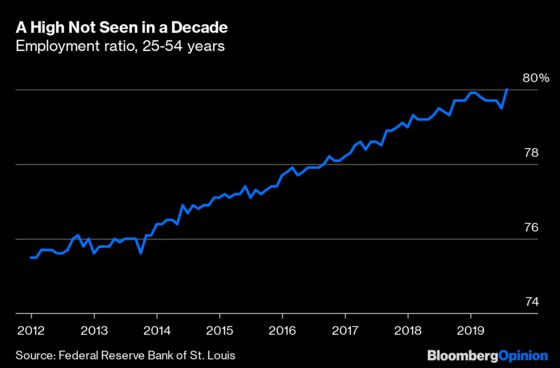

Personal consumption continues to grow, as do industrial production and gross domestic product. And the labor market also is strong -- the prime-age employment-population ratio, probably the best broad indicator of labor-market health, is still rising, and in August it hit 80% for the first time since the recession:

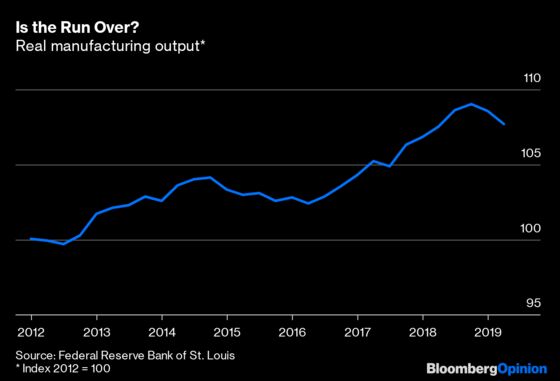

There are a couple of exceptions to this positive pattern. Investment fell in the second quarter of 2019. And real manufacturing output has been dropping since the beginning of the year:

But the general pattern is one of solid hard numbers and weakening soft numbers. This sets the stage for a rematch of 2017. Will the subjective sentiment surveys prove prophetic once again, or will the economy shrug off the doom and gloom?

There are cases to be made on both sides. The main argument for pessimism is the trade war, along with the wider global slowdown. With more China tariffs going into effect in October and no deal in sight, it’s looking more like Trump has no actual goal for his trade war, and simply intends to keep piling on tariffs in order to weaken China and/or satisfy his own appetite for destruction. The monetary cost of those tariffs is being borne almost entirely by American consumers and businesses, and some U.S. companies are being hurt by higher input prices. China is sure to retaliate, probably against the already beleaguered U.S. agriculture industry. Meanwhile, China’s own economy continues to slow for a variety of reasons, which may be taking countries like Germany and South Korea down with it. The stage may now be set for a global recession as the economies of China and the developed nations begin to disentangle.

The optimistic case for the U.S. economy is that none of this really matters, and might even be good news. China’s slowdown will simply make Chinese goods cheaper, canceling the effect of the tariffs. Slowdowns in China, Germany, Korea and elsewhere will weaken the competition, allowing U.S. businesses to grab market share. Capital will flow out of world markets and into the U.S., boosting asset prices and spurring a renewed boom in consumption and investment. The Fed will continue to cut rates. And through it all, the American consumer, holding less debt than before the recession, will keep the U.S. safe from the global storm.

A recession is far from a done deal. But the U.S. economy is entering an odd limbo, no longer clearly in a boom but not necessarily headed for a bust.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2019 Bloomberg L.P.