Hong Kong Banks’ Biggest Threat Could End Up Saving Them

(Bloomberg Opinion) -- In a poor, underbanked country, there wouldn’t be anything unusual about imposing a $6.40–a-month penalty on depositors unable to keep at least $640 in their savings accounts. That’s just how financial exclusion works.

But in rich Hong Kong, a city that gives banks more than $26 billion in annual earnings, it took a fintech revolution to make HSBC Holdings Plc drop its minimum-balance charge for 3 million customers — a fee it had levied for 18 years.

Scrapping charges that annoy retail customers will buy the lender some protection against the city's eight virtual banks, which are preparing to go online and looking to build their deposit bases from zero. The challengers are expected to pay higher interest; they’re also unlikely to impose minimum-balance penalties. Now that HSBC, the market leader, has made its move, other bricks-and-mortar lenders may have to follow suit.

While my colleague Nisha Gopalan and I remain skeptical about the impact of branchless, internet-only banks, the city’s established lenders like HSBC, BOC Hong Kong (Holdings) Ltd., Standard Chartered Plc and Hang Seng Bank Ltd. have another problem that can’t be papered over by tweaking fees: timing.

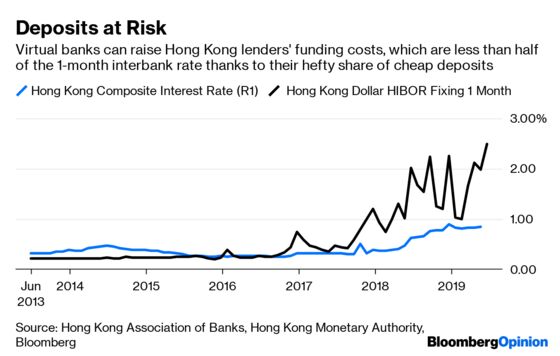

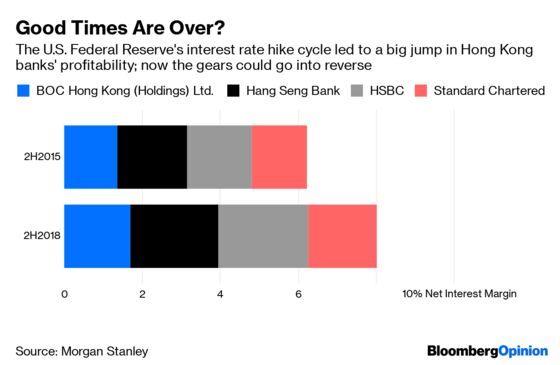

After years of struggling in the post-financial crisis world of quantitative easing and cheap cash, Hong Kong banks have made out like bandits since the Federal Reserve started raising rates in late 2015. Outsize gains in net interest margin helped them outperform most global banks. Even at present, Hibor, the local interbank lending benchmark, is more than twice as high as banks’ cost of funding, which stays in check because cheap deposits are always slower to reset than loans.

It may, however, prove to be a short-lived boom. With the Fed’s rate-increase cycle threatening to reverse, Hong Kong banks’ profitability is likely to come under pressure. Digital rivals, with deep-pocketed sponsors, are showing up just when weaker interest rates could shave 4% to 8% from earnings estimates of the city’s top deposit-taking institutions next year, according to Morgan Stanley. Profit expectations for 2021 have to be pruned by 6% to 13%, the investment bank’s analysts note.

Oddly enough, it's the tech disrupters that could end up saving the very banks whose profit pools – among the world's biggest – they're aiming to capture.

Five years ago, Hong Kong’s regulator had no room for Alibaba Group Holding Ltd.’s dual-class shares because holders’ voting rights would be unequal. Now, not only do the city’s investors want the company to return with a secondary listing, but its banks are also praying for a successful Alibaba share sale, which could raise as much as $20 billion. That might help lift sentiment, which has dimmed as China’s economy slows and trade tensions between Beijing and Washington fester.

In Hong Kong, the IPO market and bank profitability are joined by the common thread of liquidity. Large share sales tend to soak up cash from the banking system, albeit briefly, pushing up Hibor even without a lift from U.S. Libor.

That’s good for banks. Even then, Hong Kong lenders’ best season probably won’t last long after the June quarter ends. It could be some time before the Fed turns hawkish again. Meanwhile, the worst that can happen is its super-dovish stance drives Libor too low. A middling scenario would be one in which lenders nip a fee here, tuck a charge there to protect deposits from an assault by their virtual rivals, while a revived IPO market keeps Hibor — and banks’ interest margins — from crashing. If the city’s biggest share sale since 2010 can’t do the trick, then perhaps nothing will.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.