(Bloomberg Opinion) -- It isn’t quite last orders for Anheuser-Busch InBev NV. But neither has it seen the bill.

The company said Thursday that sales growth improved in the final quarter of its financial year, and forecast a further escalation in 2019. The world’s biggest brewer said it expected strong expansion in both revenue and Ebitda.

The more upbeat performance is a stark contrast with recent announcements. In the third quarter the company missed profit expectations and halved its dividend.

The U.S., one of its biggest markets, contributed to the improvement. Although sales are still declining, the company is ceding less market share. There was also strength in some other key locations, including Mexico and China, offsetting weakness in Brazil and South Africa.

The shares rose as much as 6 percent. But investors may be getting ahead of themselves.

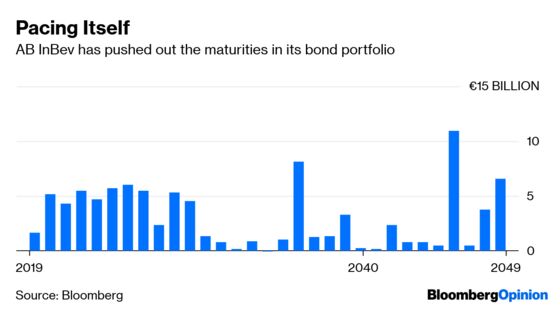

First, the company is still lumbering under a substantial pile of borrowings from its 2016 acquisition of SAB Miller. True, it is taking action here: Net debt fell over the second half from $108.8 billion to $102.5 billion. And the dividend cut announced in October will help – the company said it expected net debt to Ebitda to fall to below 4 times by the end of 2020, compared with 4.6 times at the end of 2018. Selling a stake in its Asian operation through an initial public offering would also speed deleveraging.

But there is still a very long way to go to achieve its goal of driving net debt down to just twice the level of Ebitda.

And there’s a further worry, thanks to Kraft Heinz Co. Its recent ugly earnings report and write-down of some of its biggest brands is a stark warning for companies that have expanded aggressively through acquisitions.

Though it may have dodged a bullet today, AB InBev is still vulnerable to serving up some serious disappointment. The company had $133.3 billion of goodwill on its balance sheet at Dec. 31, and $44.8 billion of intangible assets, which together exceed its market capitalization. This presents a risk if demand wavers for any of its big brands as they battle niche and local rivals.

And it is not just consumers’ tastes that have changed. Instead of margin expansion, investors now want to see a better balance between the top line and bottom line.

The improvement in revenue moves AB InBev closer to achieving this. But the company risks getting knocked off course. Its traditional model has been rampant cost-cutting to fatten profits, an approach that has been fostered by backer 3G Capital, also the second-biggest investor in Kraft Heinz.

The shares, which have fallen more than 20 percent over the past year, trade on a forward price earnings ratio of about 17 times, a discount to both Heineken NV and Carlsberg A/S.

To close the gap, AB InBev must show material progress on bringing down its borrowings, maintain its stronger performance, and show that it’s taking a different path from Kraft Heinz. Otherwise it could face a nasty reckoning with investors.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.