A Subprime Lender Tries the Ultimate Cutthroat Deal

(Bloomberg Opinion) -- It would usually be laughed out of town. A hostile bid with no takeover premium for a company that’s seven times bigger, in one of the most controversial parts of U.K. financial services: Subprime lending. Non-Standard Finance Plc’s attempted takeover of Provident Financial Plc exploits a gaping hole in the credibility of the target’s management.

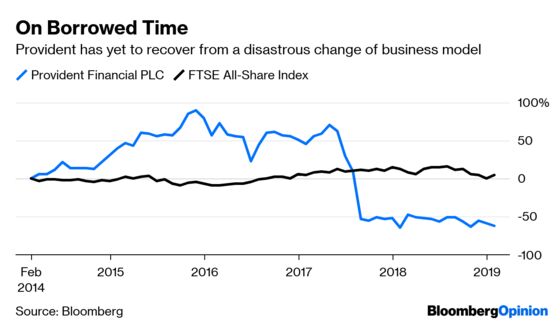

NSF is led by former Provident CEO John van Kuffeler. He failed with a friendly approach to Provident last year. Back then, the latter was in a troubled state after a botched change of business model, moving from using agency debt collectors to in-house staff. Its shares are even lower today. This time, Van Kuffeler is aggressively making a formal offer with the support of big shareholders who own chunks of both companies – including half the Provident register.

Provident was worth 1.3 billion pounds ($1.7 billion) before the bid was made. NSF’s market capitalization was just 180 million pounds. In an all-share deal, that caps the premium NSF can offer. Indeed, the terms of the bid contained no premium at all, offering Provident shareholders an 88 percent share in the combination, matching Provident’s share of the pair’s total market value as of Thursday.

But the warm market reaction to the deal has created a premium out of thin air. Based on the bump in NSF’s share price, its offer is worth 11 percent more than Provident’s undisturbed value. That’s better than nothing but it’s still an unacceptable top-up for a change of control. Minority shareholders should demand more. The snag is that unless NSF’s share price travels much higher, any premium from tweaking the terms will be more symbolic than lucrative.

Provident threw mud at NSF’s bid on Monday, and its shares are trading above the offer. The market sees both the possibility of NSF winning or of Provident getting a higher bid.

The choice for Provident shareholders is between two very different strategies. Van Kuffeler wants to jettison its car loans and digital unit to focus on the core doorstep lending business. That shrinkage would offer a quick capital return. By contrast, Provident sees value in its full portfolio, given overlapping customer bases and younger customers’ preference for digital products. That’s for the long haul.

While Van Kuffeler used to run Provident, NSF’s offer comes from outside and with no recent access to the company. But Provident’s credibility in championing the current strategy is stretched. Melrose Industries Plc’s successful bid for GKN last year showed how hard it is for out-of-favor boards to win back the initiative once they’ve received a hostile bid, especially when bidder and target shareholders overlap. Provident CEO Malcolm Le May can keep fighting but, without a competing bid, his best bet may be to force Van Kuffeler to pay a bit more for an agreed deal.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.