A Decent Year for Hedge Funds Is Still Not Good Enough

(Bloomberg Opinion) -- There’s good news and bad news in last year’s hedge fund numbers. While the industry has recovered some of its swagger, its performance continues to suggest that active portfolio managers aren’t living up to their promise to outpace passive returns, even during bouts of market volatility.

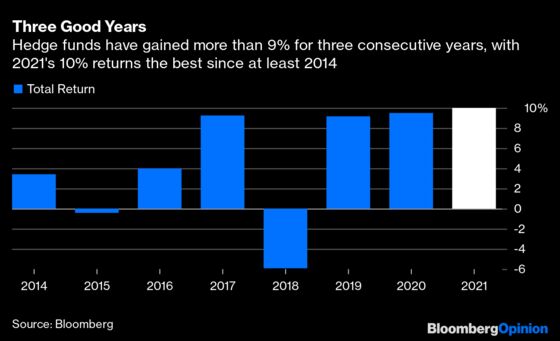

The industry can point to its highest average returns since at least 2014 and the fresh cash being allocated to firms by investors. Skeptics will note that customers would have made more money buying a low-cost equity index tracker tied to the benchmark U.S. stock index. I count myself in the latter camp.

Hedge funds gained 10% on average last year. A three-year winning streak culminated in their best performance in the seven years since Bloomberg began compiling data on the industry.

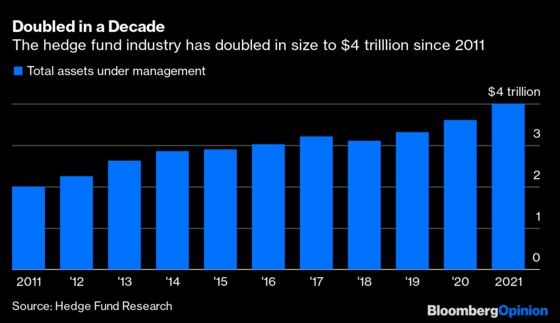

Those returns have lured investors. After dipping in 2018, hedge fund assets climbed to a record $4.01 trillion by the end of December, according to figures compiled by Hedge Fund Research. That’s an increase of about $400 billion in the year, with the pile reaching double the amount managed a decade ago.

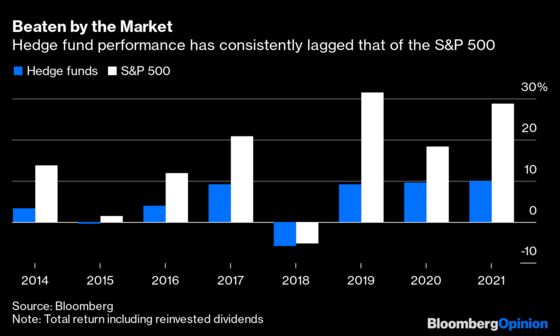

Last year’s double-digit gains posted by the hedge fund community look healthy enough to justify those inflows – until you compare them with the total return available from the S&P 500 index. Including reinvested dividends, the stock market benchmark delivered almost three times what hedge funds made for their clients last year, extending a losing-out-to-beta streak that’s persisted for several years.

In November, volatility in stocks, bonds and currencies soared amid concern about the omicron virus variant, rising consumer prices and an energy market squeeze. That’s supposed to be the kind of environment in which hedge fund traders shine. Instead, they lost 1.63% in aggregate, double the slump in the S&P 500’s total return.

Even during the market downturn of 2018, investors would have lost less in an index tracker than they did in hedge funds. So the shaky start made by markets so far this year doesn’t augur well for the active crowd’s ability to start to outperform.

For sure, the aggregate performance masks a wide dispersion in individual returns. Crispin Odey’s fund ended last year with a gain of about 54% — but that was after a disastrous fourth quarter wiped out half of the 108% increase he’d made by the end of September, Bloomberg News reported earlier this month. And Michael Hinze’s flagship fund had its best performance in five years, with a 2021 gain of 21.4% — after declining by almost 35% in the previous year.

But even for investors who can stomach that kind of volatility, it’s impossible to predict which portfolio managers will succeed in delivering alpha and which will fail. Until and unless the industry average can consistently outpace the benchmark index, investors would be well advised to save on fees and continue allocating capital to index tracking products.

More from Bloomberg Opinion:

-

The Paranoid Style in American Investing: Chris Bryant

-

Don’t Panic, Europe. That’s Not Inflation. It’s Just Gas: Marcus Ashworth

-

Rokos Investors Sign Up for a Wild Hedge Fund Ride: Mark Gilbert

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2022 Bloomberg L.P.