(Bloomberg Opinion) -- Construction equipment rental sounds like a dry, dispassionate business, but Ashtead Group Plc knows plenty about joy and despair.

The FTSE 100 company generates more than four-fifths of its sales in the U.S via its Sunbelt subsidiary. A succession of devastating hurricanes there has spurred demand for its generators, pumps and chainsaws. It also rents out flooring and forklifts for happier occasions, such as the Lollapalooza music festival.

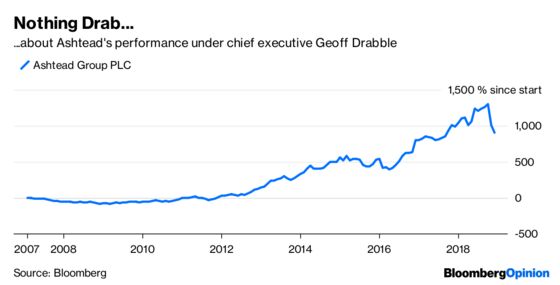

The shares have had a pretty intense few months too. Having touched a record high in October, the stock has since slumped 33 percent, erasing 4 billion pounds ($5.1 billion) of equity value.

Recent economic and homebuilder data have raised fears of a slowdown in the construction sector, which accounts for almost half the group’s sales. Traders fret that the narrowing spread between long- and short-dated Treasuries points to a recession on the horizon. American rival United Rentals Inc.’s shares have plunged too.

Perhaps investors have been too negative. On Tuesday, Ashtead’s soon-to-retire chief executive Geoff Drabble said there’s a “danger of people worrying about a recession that is not anywhere close to upon us.” In reality business conditions are “more sanguine than financial markets,” he told Bloomberg Opinion, referring to customers’ long order backlogs. He may have a point: The shares surged as much as 7 percent after Ashtead predicted full-year results would exceed its expectations.

In any case, Ashtead is now much larger and more resilient than it was when Drabble took over almost 12 years ago. When the next recession does hit, the company should cope.

How times have changed. When accounting irregularities got Ashtead into bother with its creditors in 2003, the stock plummeted to just 2.5 pence. Investors brave enough to jump in then have enjoyed astonishing rewards. With dividends reinvested, the shares have returned 93,000 percent since that nadir. That’s Amazon-esque, and the similarities don’t end there.

To be sure, the self-effacing Drabble is about as far removed from San Francisco and Seattle as you can imagine. Equipment hire is an unfashionably capital-intensive business (there’s 5.4 billion pounds of kit on Ashtead’s balance sheet) and requires plenty of face-to-face time with customers. Sunbelt has more than 700 U.S. stores.

That hasn’t stopped the company from talking up its “platform” credentials, though, and it’s not entirely spurious to suggest it’s becoming the “Everything Store” of equipment rental.

Ashtead is benefiting from the trend for renting and outsourcing, rather than ownership. Sales have quadrupled since 2011, via a combination of organic growth and deals. Big players such as Ashtead and United are squeezing out independent operators as they’re able to offer a wider range of tools and use their heft to buy equipment more cheaply. Increasingly, its customers order equipment via an app and want it delivered on the same day.

Opening new stores and a tight U.S. labor market haven’t stopped Ashtead from lifting profit margins and cash flows. Analysts surveyed by Bloomberg anticipate almost 600 million pounds of free cash flow for the year to April.

If sales do slow suddenly next year, Ashtead can stop buying equipment for a while and continue to generate cash. That’s one reason why analysts remain bullish. Their price targets compiled by Bloomberg imply a 55 percent upside over the next 12 months, one of the largest price-expectation gaps in the FTSE 100.

Another is that Ashtead hasn’t geared up to fund its expansion. Net debt is less than 2 times Ebitda, whereas United’s is closer to 3 times. Moody’s recently upgraded Ashtead’s debt to investment-grade, and it’s been returning surplus cash via buybacks. Keeping the money in reserve might be more prudent given worries about the economy, but it might attract unwanted attention.

Ashtead is valued at 11 billion pounds, including debt. That would be a lot for an acquirer to digest, but Ashtead's largely dollar-denominated cash flows and asset-heavy balance sheet might still make a tempting target. Cerberus Capital Management made a $5.5 billion offer for United before the last recession but withdrew when the credit taps ran dry.

Drabble has done an impressive job at Ashtead. Surrendering its independence probably isn’t part of his succession plan.

Residential construction is only about 5 percent of Ashtead's business, though.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2018 Bloomberg L.P.