A $44 Billion IPO Isn’t the Win SoftBank Needs

(Bloomberg Opinion) -- For SoftBank Group Corp. Chief Executive Officer Masayoshi Son, selling a stake in Arm, the British semiconductor firm that kicked off his tech spending splurge, cannot have been part of the plan. At least, not yet.

When SoftBank agreed to buy the Cambridge, England-based firm for 24 billion pounds ($32 billion) four years ago, the expectation was that it wouldn’t return to the markets in the foreseeable future. Son’s vision was framed in decades, not years. A sustained period nestled within SoftBank would allow the chip designer to invest for the long-term, substantially improving its value.

Yet SoftBank is considering an initial public offering or stake sale as soon as next year, the Wall Street Journal and Bloomberg News reported on Monday. In October, Arm CEO Simon Segars mooted 2023 as the earliest date.

The accelerated timeline follows a slew of writedowns prompted by poor-performing investments made by SoftBank’s Vision Fund venture arm in WeWork, Uber Technologies Inc. and others. The Vision Fund lost almost $18 billion in its last fiscal year. Activist Elliott Management Corp. seized upon its tribulations to build a stake in SoftBank, calling for improved governance. Son responded with debt-cutting plans and a potential 2 trillion yen ($19 billion) share buyback.

The cash raised from an Arm IPO would be only one benefit. A successful deal would be a much needed win for Son: something to convince the world that he’s still got what it takes.

Arm is valued internally at its acquisition cost. Listing the shares publicly would give better visibility into what people think it’s worth. That might benefit both the paper returns at the Vision Fund — which holds 25% of the business — and SoftBank’s own shares, which trade at a discount to the value of its constituent investments.

The problem is that, right now, Arm doesn't look quite ready to return to the markets.

The company licenses semiconductor designs to chipmakers whose silicon goes into almost every smartphone in the world. Revenue, mainly from royalties, jumped more than threefold between 2009 and 2015. When SoftBank bought the British firm in 2016, it was atop the crest of Apple Inc.’s success with the iPhone.

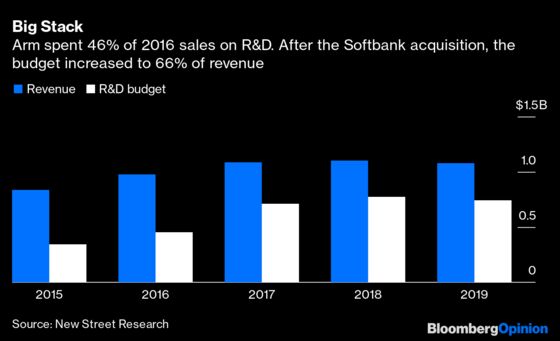

But the acquisition coincided with the peak year of global smartphone sales. The pace of growth at Arm has since slowed. Revenue increased just 1% in the 12 months through March 2019, the most recent year for which data is available. When he announced the deal, Son predicted that the number of Arm-based chips shipped each year would rise from 15 billion to 71 billion within five years. That number looks all but unattainable: It hit just shy of 23 billion chips last year.

At the same time, investment in research and development means that profitability has also dipped. Paring back such spending could lead to a rapid increase in profit that would boost the IPO financials. But cutting back too quickly would also risk wasting the spending to date. Some new chip architecture is overdue by Arm’s standards (the last generation was released in 2011). The next offering will likely include features geared towards machine learning, and augmented and virtual reality. For now, investors buying in this time around are taking more of a bet that Arm’s R&D will bear fruit.

That might be enough to get a listing done. There’s strong appetite for tech IPOs even amid the broader market volatility, and Arm is well positioned to capitalize in the long term as fifth-generation mobile networks mean that ever more computing power is built into cars, machines, factories and homes.

But a substantial uplift on the purchase price could be a challenge. New Street Research estimates Arm could fetch a valuation of $44 billion were it to list at the end of 2021, a gain of roughly 40%. That would be a poor return compared to the benchmark Philadelphia Stock Exchange Semiconductor Index, which has climbed nearly 160% since the original acquisition.

Buying Arm wasn’t easy. Son had to pay a punchy asking price and assuage U.K. worries about how the firm would be run. But selling a stake back to the stock market at a valuation that suits his own agenda may be harder.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2020 Bloomberg L.P.