(Bloomberg Opinion) -- 3M Co.’s largest ever deal calls for a stiff drink rather than a champagne toast.

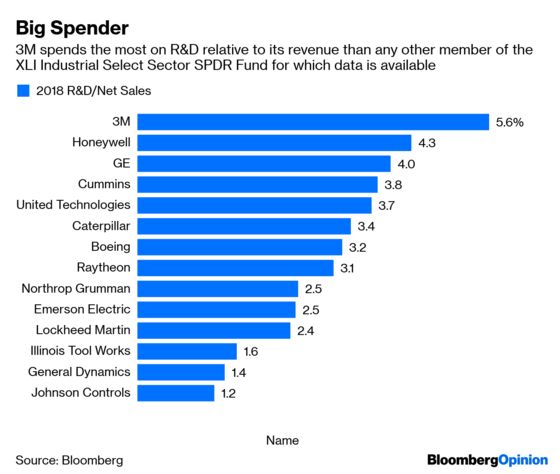

The maker of Post-it notes announced on Thursday that it would acquire wound-care company Acelity Inc. for $6.7 billion including debt. The takeover easily tops 3M’s $2.5 billion purchase of Capital Safety in 2015 as the company’s biggest. While the company has historically grown through innovation, as opposed to massive deals, there’s been a debate lately about whether 3M’s spending on research and development is delivering the returns that it once did.

The Acelity purchase suggests 3M has run out of better ideas as weak demand for automotive and electronics products and challenges in Asia weigh on 3M’s growth prospects. In a rough start for new CEO Mike Roman, the company last month announced its fifth guidance cut in a year and warned its revenue may decline in 2019, excluding the impact of M&A and currency swings.

3M’s takeover target Acelity, by contrast, is growing quickly right now. Its 2018 revenue of $1.5 billion was up about 10 percent from a year earlier. Acelity’s business benefits from an aging population and rising rates of obesity, diabetes and other chronic conditions that can cause wounds. Its dressings and other products for treating, cleaning and healing wounds will complement 3M’s existing medical tape and skin protectants and closures business. The purchase also strategically aligns with the company’s $1 billion takeover of M*Modal’s artificial-intelligence platform for doctors earlier this year. Taken together, it appears 3M is doubling down on a health-care division that was a rare bright spot in the company’s otherwise dour first-quarter earnings report. The health-care and consumer units were the only two primary businesses to report positive organic sales growth in the first three months of the year.

That being said, I’m highly skeptical of the wisdom of pursuing such a large takeover right now. I have a rule of thumb that the day a company announces its all-time biggest deal is the day you should start to worry, but this situation seems particularly acute. Asked about 3M’s disappointing first-quarter performance, CEO Mike Roman said the company “didn’t respond aggressively enough” to weaker demand. The sales weakness was mostly concentrated in the well-known trouble spots of China, automotive and electronic markets, though — so what exactly caught management by surprise? The earnings miss and the announcement of an aggressive step-up in restructuring including 2,000 job cuts suggest an operational foot fault. And now it has to pull off the biggest deal in its history? With all the integration issues it will entail? I am sure that will go just fine.

The purchase price isn’t outrageous relative to other health-care products deals, but it’s not a bargain either at 15 times Acelity’s adjusted 2018 Ebitda, or about 11 times the Ebitda 3M thinks it can achieve under the first year of ownership including expected cost savings. It’s not clear where it’s going to get all of those savings as Acelity already has an enviable adjusted Ebitda margin of 30 percent.

Also, the timing is curious. Acelity’s parent company, KCI Holdings Inc., had filed for an IPO in mid-April and its private equity sponsors had previously explored a return to public markets over the course of 2015 and 2016. So the deal talks appear to be a relatively new development and you have to think 3M offered a richer valuation than what Acelity’s backers thought they could get via a share sale. There was already a question about 3M’s recent announcement that it would shrink its five operating segments down to four and whether that was really about streamlining or about spreading its automotive pain around and reducing disclosure. The announcement of 3M’s biggest deal just one week after its earnings disappointment gives a similar impression that it’s trying to paper over, or at least distract from, its sales woes.

There aren’t many CEOs who can survive a series of guidance cuts in their first year on the job. There are even fewer that can survive a major M&A flop.

It reported a net loss in 2018 in part because of hefty interest expenses tied to its debt load.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.