Sainsbury Faces Tough Times in Its Asda-Free Future

(Bloomberg Opinion) -- Now that J Sainsbury Plc’s 7.3 billion pound ($9.4 billion) purchase of Walmart’s Asda has gone out with the spoiled salad, the U.K. listed supermarket must show it has a good shot at going it alone.

Mike Coupe, chief executive officer of Sainsbury, says he is confident in the group’s strategy. Investors clearly don’t share that view – at one point on Thursday the stock fell to the lowest in 30 years.

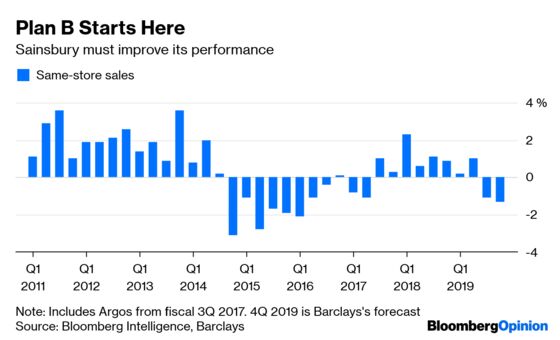

Sainsbury’s same store sales have been deteriorating since the merger was announced almost exactly a year ago. The deal was clearly a distraction. The company is likely to insist that its been addressing the lackluster performance when it announces full-year results next week. But the question is whether it can avoid becoming the sick grocer of Britain, and the target for rivals to steal market share.

To avoid this fate, it must lower the prices it charges for everyday essentials, and improve basic operations. Neither will be easy.

The march of the German discounters, and their recent push into upmarket ranges, means every echelon of the food sector is under pressure. Domestic rivals Tesco Plc and Wm Morrison Supermarkets Plc have responded by taking their prices closer to those of Aldi and Lidl.

But Sainsbury is far from the value end: shoppers go there for quality products, particularly from its own-label ranges. Like all big supermarkets, it can afford to charge more than the discounters because it can offer a broader range, better services and expanded parking facilities. But if the premium shoppers must pay drifts up too far, then customers will notice, and go elsewhere.

While Sainsbury has been holding its own in more specialist and premium areas, it is losing share in everyday items. It needs to lower prices for essentials, but without losing its appeal at the higher-quality end. This will require some finely balanced decisions.

Given that Sainsbury’s strength isn’t price, the appeal of its stores and products is crucial. But it has struggled to maintain standards. Last summer was a difficult period – the group cut store managers at what should have been a quiet time of the year for the changes to take hold. Instead, the staff reductions coincided with a heatwave that drove up demand for salad, soft drinks and burger buns, leading to empty shelves.

Coupe said in November that the company had addressed these issues. But poor availability and shabby stores seems to be a continuing problem. The company has a battle ahead to convince investors that it is making operational improvements and enhancing its supermarkets.

And there’s an opportunity in doing so. Tesco is cutting some of its food service counters. If Sainsbury can make its stores more inviting, there is a chance to lure customers from both its bigger rival, and the discounters.

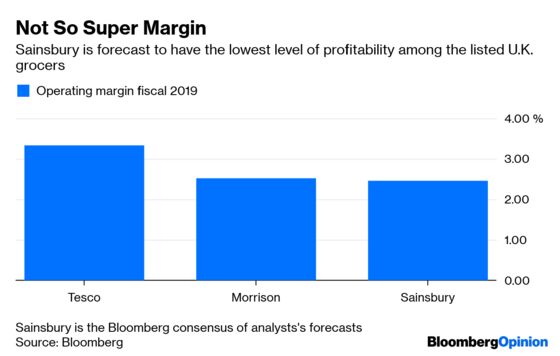

But addressing price and standards may mean increased investment, and Sainsbury doesn’t have a large amount of financial firepower. It is forecast to have a lower operating margin than Tesco’s when it reports next week.

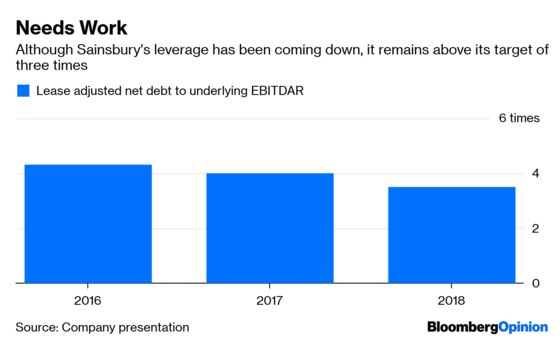

Lease-adjusted net debt to earnings before interest, tax, deprecation, amortization and rent was 3.5 times in 2018. Although that’s an improvement on the previous two years, it is still above the company's target of 3 times. The Asda deal would have reduced leverage because its partner would have brought more freehold property to the enlarged company.

Sainsbury does have some wiggle room. It has been investing in its bank and in integrating Argos. These calls on its funds should start to subside, freeing up resources to invest in stores and prices.

Coupe nevertheless faces an uphill struggle to reinvigorate his company. The drop in the share price shows investors are aware of the risks and costs of turning the business around. If he can’t get the job done, then he might be faced with another deal. But this time an activist investor, or a predator clamoring to take over the business, will be in the driving seat.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.