(Bloomberg Opinion) -- After abandoning its talks to merge with local rival Commerzbank AG, Deutsche Bank AG’s management says it won’t be rushed into ripping up its existing strategy. And, in fairness, there are no easy fixes to restoring profitability at the ailing German giant.

But with Deutsche Bank’s revenue outlook now even weaker than before the Commerzbank discussions, much deeper cost cuts look inevitable. A root-and-branch rethink of its investment bank – resisted until now – wouldn’t go amiss.

The two 149-year-old lenders explored a combination to tackle their common plight of feeble returns. Unfortunately, it was no surprise that they concluded a deal would have been too expensive and too risky. It wouldn’t have done much to ease the competitive pressure at home from cooperative and state-backed lenders. Even after cutting tens of thousands of jobs, they’d have gained little pricing power.

Nor would a merger have addressed the inefficiency of Deutsche’s investment bank. Concerns about the securities unit led the European Central Bank, the euro zone’s finance regulator, to question the wisdom of putting yet more deposits to work to finance its trading business.

For Deutsche Bank to find a credible path to sustainable profitability on its own, it will have to embark on a more ambitious reboot, scaling back the stocks and bond-trading unit. Until then, the division will keep dragging on the group and put off any other potential partners. Unlike some of its big European rivals, the German lender doesn't have a booming wealth management or consumer banking business to fall back on.

Group revenue in the first quarter fell 9 percent to 6.4 billion euros ($7.1 billion), Deutsche Bank reported on Friday. Across the firm, sales will remain stuck this year, after what is typically the strongest three-month period. The bank expects 2019 revenue to be flat in commercial and retail banking and flat in asset management, although the investment bank might see slightly higher revenue should the recent markets recovery continue. It’s hard to see how Deutsche will hit its 4 percent return on tangible equity target for 2019. It was 1.3 percent in the first quarter.

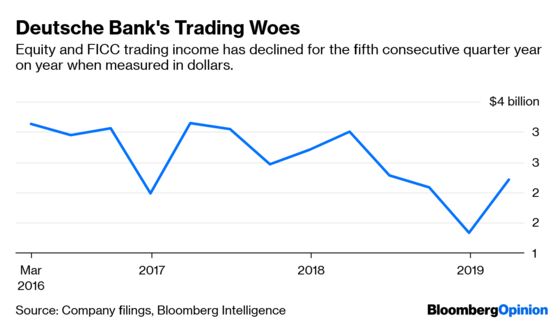

The trouble with the investment bank is that it still consumes about two-thirds of the group’s capital, while generating paltry returns. Last year, the unit’s cost to income ratio was 95 percent and the division swung to a loss in the first three months of 2019 after a 19 percent slump in trading income. The loss does reflect in part a levy it booked in the period and a pullback from some rates and equities businesses. But revenue fell too in foreign exchange and credit trading.

Chief executive Christian Sewing and his predecessor, John Cryan, have stopped short of a broad change of strategic direction on investment banking. Deutsche is still trying to compete with Wall Street firms on domestic U.S. business, for example. It boasted about being the joint No. 1 in managing American IPOs in the first quarter; an anomaly when you consider Deutsche Bank hasn’t ranked among the top five over the previous three years.

The U.S. securities operations are a particular drain. Deutsche Bank loses as much as 300 million euros ($334 million) yearly before tax on the equities business alone in the U.S., JPMorgan Chase & Co. analysts have estimated.

Time isn't on Deutsche's side. A slowdown in Germany's export-driven economy, coupled with the enduring squeeze to margins from record-low interest rates, will keep the pressure on revenue. Fears about the impact of a slowdown on Deutsche’s and Commerzbank’s turnarounds were allegedly what prompted Berlin to encourage the merger discussions.

Pressed by analysts on the firm’s future strategy on Friday, Sewing wouldn’t be drawn much. But one option is non-negotiable, he said: Deutsche Bank will remain a globally relevant financial services institution. That may become a matter of interpretation.

Given Deutsche Bank’s meager generation of free cash flow, paying for a bigger restructuring might require tapping investors for funds (assuming it doesn’t sell its asset management business). It’s a painful prospect, with the shares trading at about a quarter of book value. Regardless, a bold, standalone plan is what Sewing needs right now.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Elisa Martinuzzi is a Bloomberg Opinion columnist covering finance. She is a former managing editor for European finance at Bloomberg News.

©2019 Bloomberg L.P.