(Bloomberg Opinion) -- Rakesh Kapoor’s impending departure from the top job at Reckitt Benckiser Plc has taken on new urgency following the disastrous outcome of a spin-off made on his watch. The U.K. consumer goods group will need to clear the slate.

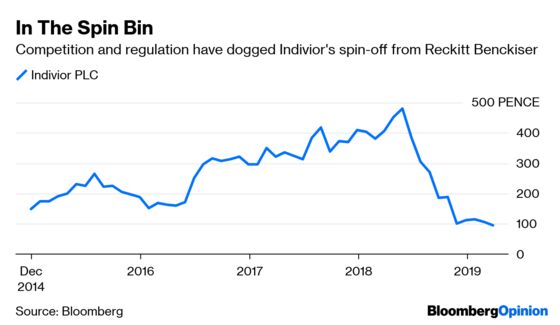

There were many reasons for Kapoor and fellow managers to demerge Indivior Plc in 2014. Before long, generic competition would hit the drugmaker’s leading opioid-addiction treatment. In the background was the sort of early-stage litigation that often plagues the pharma industry. Reckitt got the demerger away before the competition struck. On Wednesday, litigation risk became a stark reality, hitting Indivior and its former parent hard.

The U.S. Department of Justice has accused the drugmaker of misleading clinicians about the dangers of its product, fueling a deadly epidemic of opioid abuse. A possible $3 billion fine looms. The issue is long-running, and Reckitt disclosed a $400 million provision related to the case in its most recent annual report.

Investors had been hoping that Indivior would reach a settlement. But those talks failed, and court action looms. The drugmaker’s already battered shares slid as much as 80 percent on Wednesday, valuing it at 153 million pounds. Reckitt fell 7 percent, wiping 3.4 billion pounds ($4.5 billion) off its market value.

The guess must be that if a fine is levied, it will be split between the two companies. Indivior could scarcely afford even that. However, Reckitt's provision may relate to parallel, but separate, litigation. In that case, Indivior would get no help from Reckitt in paying. And the latter would be at risk of its own fine – however much that may be – if it can’t settle.

For Reckitt, the blow-back could go beyond any headline financial penalty. The company points out that it isn’t the target of the indictment. Even so, the allegations relate to a period when it still owned Indivior, and Reckitt’s $56 billion market value surely makes it a tempting target if Indivior can't pay.

As analysts at Jefferies point out, the market is worried about any spillover to Reckitt's U.S. infant formula business – its $18 billion acquisition of Mead Johnson in 2017 – and the risk that it could lose contracts as a consequence. In the worst case scenario, Reckitt could pay the full fine and lose a low single-digit share of group profit over a period of years, Jefferies cautions.

The episode reflects badly on Reckitt from start to finish. There may have been good strategic and financial reasons to jettison a business that didn’t fit well with its portfolio of household cleaning and consumer healthcare products. And Reckitt has been actively pruning its portfolio in recent years. But the demerger also removed what turned out to be problem child from the company – and neutralized a risk to management’s incentive plans, which have paid out richly since. Shareholders who held on to both shares haven’t fared so well.

Kapoor is set to depart by the end of the year. He may now have to go sooner. Reckitt will be hoping new management can help it put this crisis behind it.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.