(Bloomberg Opinion) -- And now for my next trick.

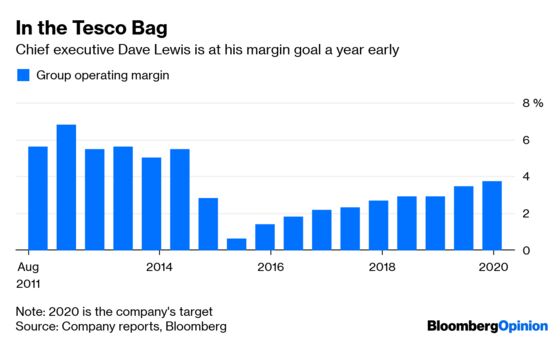

Dave Lewis, chief executive officer of Tesco Plc, is within a whisker of reaching the ambitious profitability targets he announced in October 2016.

His goal was to achieve an operating margin of between 3.5 percent and 4 percent by February 2020. For the full year to Feb. 23, the group operating margin was 3.45 percent. For the second half of the year it was 3.96 percent, and excluding wholesaler Booker it was 3.79 percent, comfortably within the range.

Unless there is a dramatic dropoff in performance, Lewis will be able to declare “job done.” No doubt he has been ably assisted by the arrival of Charles Wilson from Booker. The question is what Tesco does next, and at long last there is the potential to return capital to shareholders.

The group has come a long way. Prices are closer to those of the discounters thanks to new, cheaper, brands. There’s now a significant advantage in wholesale purchasing with the acquisition of Booker, and the balance sheet has been repaired. It should also be getting some oxygen from the struggles at rival Sainsbury Plc.

There are still a few things that could knock Lewis off course.

The international arm was disappointing in the first half, although it improved in the second six months. And German discounters Aldi and Lidl are still expanding their store bases, which is fueling sales growth and market-share gains. The pressure to keep prices low and cut costs will continue.

Investors are certainly looking through any potential pitfalls. The shares have had a great run so far this year.

The focus will now be on the capital markets day in June, which will outline some of the “untapped value opportunities.”

Lewis is typically tight-lipped, but these could include exploiting Booker’s substantial skills, and potentially developing it into Britain’s answer to America’s Costco Wholesale Corp., where shoppers can achieve substantial savings by buying in bulk. There’s also potential to draw on the purchasing alliance with Carrefour SA.

Tesco’s substantial debt load had weighed on funds available for distribution. But this has improved. Net borrowings were broadly stable at 2.9 billion pounds ($3.8 billion), with total indebtedness, including store leases, at 12.2 billion. That’s a big reduction from the 22 billion pounds in February 2015.

That paves the way for Tesco to continue to rebuild its dividend, and potentially return capital to shareholders.

Lewis may well come up with some other new goals, or he might see that his work at Tesco is complete, and consider a role elsewhere, for example at Reckitt Benckiser Group Plc, which is searching for a new chief executive.

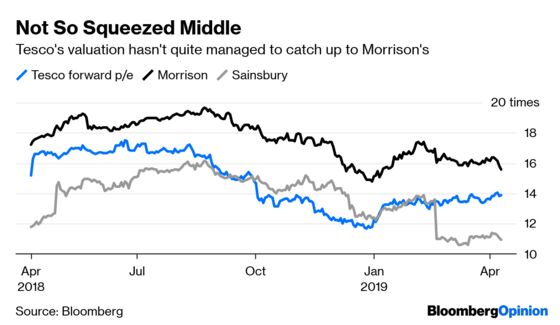

In the meantime, the shares trade on a forward price earnings ratio of about 14 times, at a deserved premium to Sainsbury, but still at a discount to Wm Morrison Supermarkets Plc.

To narrow the gap to Morrison, Tesco needs to show it will unequivocally meet its margin target and deliver on the promise of capital returns, which will now become more important to investors.

At least Lewis has an opportunity to capitalize on rival Sainsbury’s misery. He should take it.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.