(Bloomberg Opinion) -- Once again, private equity is writing a check when stock market investors are tightening the purse strings. Carlyle Group’s purchase of a minority stake in Spanish oil refiner Cepsa from Mubadala Investment Co. appears to exploit the Abu Dhabi investment fund’s desire to sell and the IPO market’s hesitation to buy. But an opportunistic investment isn’t always a bargain.

To recap, Mubadala had been looking to cash in some or all of its holding in the business. It has owned a stake since 1988 and enjoyed full ownership since 2011. It set about preparing an initial public offering while also seeking a full sale.

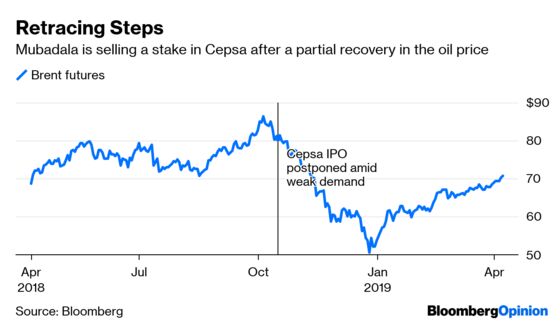

By October, plans for the IPO were further advanced than the M&A route: Mubadala got as far as setting a price range for a sale of 25 percent of the company. The deal was pulled at the last minute as the equity markets and price of oil started to fall. The offering prospectus also included a warning about a potential U.S. Department of Justice investigation linked to Malaysia’s 1MDB scandal, something that wouldn’t have helped sentiment.

Now Mubadala is selling 30 percent to Carlyle, with the option of offloading a further 10 percent. The deal values the whole business at $12 billion on a debt-free basis, or just under six times trailing Ebitda. That’s in line the both top of the IPO range and with the valuations of other integrated oil companies. The transaction allows Mubadala to sell a larger chunk than it would have done in an IPO – and gain a partner with experience in the industry.

True, the stake sale doesn’t give Cepsa the public listing and acquisition currency that the IPO would have provided. An offering would also have made it easy for Mubadala to drip further stakes into the market. Still, Carlyle will want an exit from the business one day, so it is safe to assume an IPO will return to the agenda before long, giving both sides the chance to get out.

Carlyle could be seen as a pre-IPO investor here. The firm is putting funds to work in a familiar industry. But it won’t have the controlling stake a private equity firm typically enjoys, even if Carlyle has taken minority stakes before. It could surely have afforded a 50 percent-plus stake if it had been available; after all, the buyout firm’s financial firepower is colossal and it could have roped in a partner.

This isn't a conventional buyout. If it sours, it will be fresh evidence of an industry groaning under the weight of capital it still has to deploy.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.