(Bloomberg Opinion) -- What’s an investor to do when a tech stock is no longer a tech stock?

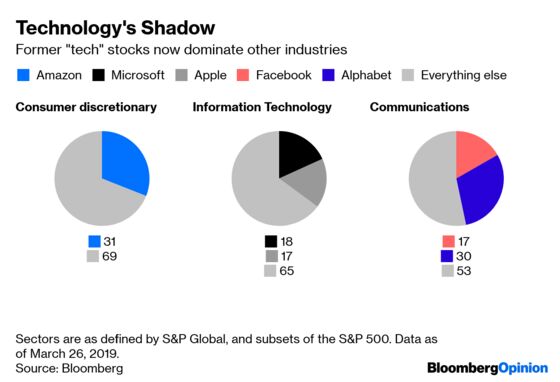

Bank of America Merrill Lynch’s U.S. stock market strategists said recently that investors should overweight technology shares. The catch is the group of tech stocks Bank of America recommended didn’t include Facebook Inc., Netflix Inc. or Google parent Alphabet Inc., three of the closely watched FANG stocks — the other in that group is Apple Inc. — that are usually associated with the tech sector. In fact, Bank of America said those stocks should be avoided. Even more confusing: Neither of those investment calls included Amazon.com Inc., which, along with the stocks of its sector — consumer discretionary — is a buy, according to Bank of America.

Six months ago, indexing giants S&P Global and MSCI jointly decided to break up the tech sector, moving some stocks out of the group that they classify as information tech. Alphabet and Facebook were reclassified from tech to the communication services sector. Netflix, previously in consumer discretionary, was also moved to communications. Amazon, on the other hand, stayed put. As such, the popular FAANG stocks, if Amazon is included for the extra “A,” span three different sectors.

The split may make more sense than it sounds. Last July, when Facebook’s troubles became apparent and the social network stock’s skid was leading the rest of the market down, I argued that the broad sell-off wasn’t as odd as it seemed. Yes, Facebook was facing its own privacy issues, but technology as a portion of the economy was bigger than ever. So if there was an issue with tech companies, there was an issue with the economy.

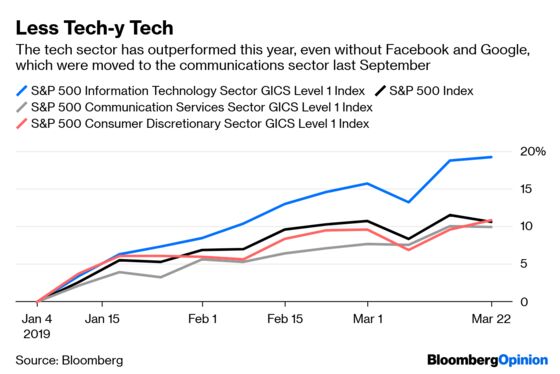

This seems to be a pretty accurate picture of the economy. Tech hasn’t just become big, it has become a big part of every sector. That being said, the stocks that have been traditionally considered tech stocks also seem a little less tech-y these days. Apple’s big product introduction this week wasn’t some new device or software but essentially a credit card and television shows. Chipmaker Intel Corp.’s earnings, feeling the affects of the trade war with China, will be up only 4 percent. Also in the top six largest components of the sector that S&P now calls tech are credit card company Visa Inc., at third largest, and rival Mastercard Inc., at No. 6, both of which should arguably be considered financial stocks.

The result is the expected growth rate of the S&P’s tech sector is just 5.9 percent this year. The communications sector, on the other hand, is supposed to be more than double that at about 12.6 percent. Tech stocks have also traditionally had relatively high profit margins. Yet this year, the profit margins of the S&P communications sector, based on earnings before interest, tax, depreciation and amortization, is expected to be 34 percent, compared with 32 percent for the tech sector. The one thing that does look most tech-y about the S&P tech sector is its valuation. The stocks in the group trade at an average 19.2 times earnings, despite the lower profit margins and growth. The S&P communications sector’s price-to-earnings multiple is 16.8.

The takeaway for investors is that, just like in the economy, it will become increasingly difficult to separate tech from everything else.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.