Hedge Fund Titan Can't Stop the Tears From Flowing

(Bloomberg Opinion) -- As the world’s biggest publicly traded hedge fund, Man Group Plc is a bellwether for that beleaguered sector of the asset management industry. The outlook isn’t improving.

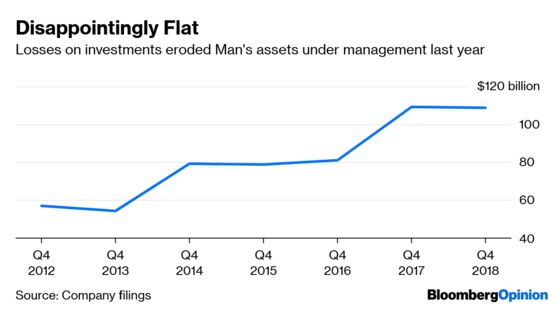

The modest decline in assets-under-management that Man reported on Friday for 2018 as a whole masks a sharper contraction in the final three months. The total declined to $108.5 billion by the end of December from $114.1 billion in the third quarter.

And chief executive Luke Ellis said that while the firm has won a “healthy number” of new mandates from clients recently, “as clients respond to changes in the market and adjust their portfolios we have also seen a pick-up in redemptions.” That doesn’t bode well.

Man’s 2018 inflows were equal to 9.9 percent of assets, down from 2017’s record 15.8 percent. Looking ahead, the firm has shrunk its target range to 1 percent to 6 percent, down from zero to 10 percent previously “to better reflect industry trends and the market environment.” In other words, Man doesn’t expect to match the inflows of either last year or the year before.

Net inflows of $10.8 billion last year were offset by $7.7 billion of investment losses by the firm’s portfolio manager, plus a further $3.7 billion erosion from currency market moves. Income from performance-related fees more than halved in the year. So much for more volatile markets, which arrived with a vengeance in the final months of last year, providing better opportunities for active managers to deliver returns.

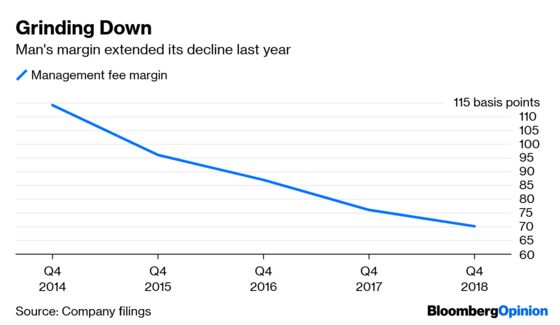

So it’s no wonder that the pressure on fees shows no signs of abating, with Man’s management fee margin declining by 6 basis points last year.

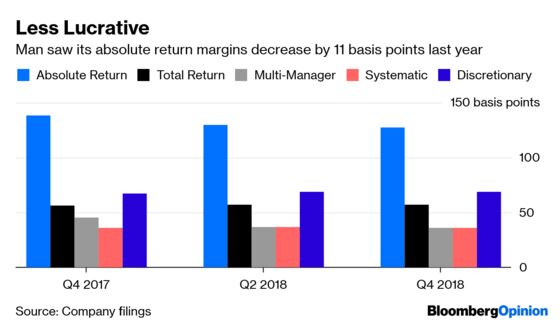

Perhaps more worrying is the drop in margins in the hedge fund’s most lucrative business category, its absolute return strategy.

While the decline can be blamed on a shift toward institutional assets, which typically attract lower levies, it still hurts Man’s ability to generate revenue. Moreover, the company says it expects those fees “will continue to gradually decline as this shift continues.”

Investors responded to Friday’s figures by driving Man shares down by as much as 6 percent, leaving the stock languishing at its lowest point this year and snuffing out a rally that saw double-digit gains in January. Shareholders would be forgiven if they started to get nervous about a repeat of last year’s stock decline of more than 35 percent. To misquote Samuel Beckett, the tears of the asset management industry are a constant quantity.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.