The Drip, Drip, Drip of Funds Fleeing Brexit Britain

(Bloomberg Opinion) -- The U.K. finance industry still has few clues about what the post-Brexit landscape will look like other than the certainty that doing business with the European Union will have more friction than it does now. Fund managers aren’t hanging around for the conclusion of the divorce negotiations, and the slow hemorrhaging of jobs and assets poses a clear and present danger to London’s future status as Europe’s financial center.

Commonwealth Bank of Australia’s asset manager First State said this week that it would transfer 4.3 billion pounds ($5.6 billion) of assets in 18 funds it manages to Dublin. That follows similar moves earlier this year by Columbia Threadneedle and Prudential Plc’s M&G unit, which are shifting 10 billion pounds and 34 billion pounds, respectively, to Luxembourg.

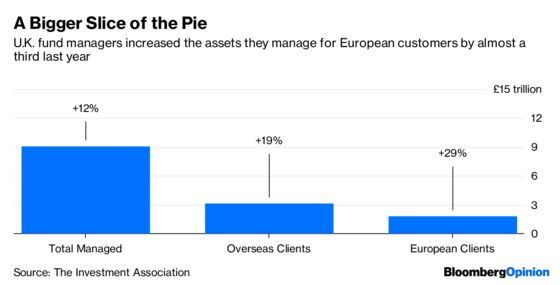

The U.K. fund-management industry is second only to the U.S. in global rankings, with more than 9 trillion pounds of assets by the end of last year, according to figures compiled by the Investment Association. Money managed for European clients climbed by 29 percent last year, the association said earlier this month.

To be clear, those three Brexit-inspired transfers represent a bit less than 50 billion pounds, a fraction of the 1.8 trillion pounds of European assets controlled by U.K. firms. Moreover, the moves are largely technical; most U.K. asset managers have funds domiciled elsewhere in the EU that are marketed to European customers, and asset allocation decisions about that cash can still be made by portfolio managers in London.

But in an industry facing persistent downward pressure on fees and a resulting focus on cutting costs, every job created in Dublin, Frankfurt or Luxembourg means less money is available to invest in London — and Brexit is forcing asset-management firms to spend more on their EU satellite operations to ensure they can service EU clients once they lose their so-called passporting rights to market and sell funds from the U.K.

Standard Life Aberdeen Plc said in February that it would establish an investment and distribution business in Dublin. Davide Serra, the chief executive officer of Algebris Investments, said in May that Brexit would “crush” London and that he was setting up a regulated entity in Luxembourg. He added that he might move to Milan.

Even Somerset Capital Management, the fund manager owned in part by arch-Brexiteer Jacob Rees-Mogg, said in July that it was starting a new fund to be based in Dublin.

There’s a subtle but distinct deterioration in the U.K.’s attractiveness as a place to set up shop. A survey released Wednesday by the CFA Institute of its U.K. members showed a 25 percent increase in the number of investment professionals expecting to leave the U.K. compared with last year’s poll, while the number of respondents who said their jobs are secure dropped to 54 percent from 60 percent.

For sure, these are incremental changes to the U.K.’s financial landscape. But as I’ve argued before, the biggest threat isn’t a one-time exodus of traders, bankers and portfolio managers around the time that Brexit becomes a reality. It’s the jobs that aren’t created and the investments that aren’t made that pose the biggest risk to London’s future status as the financial capital of Europe. And that risk is high — and rising.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2018 Bloomberg L.P.