What’ll Spark the Next Crisis? Here’s One Candidate

(Bloomberg Opinion) -- Now that everything has been said about the 10th anniversary of the Lehman Brothers bankruptcy, it’s worth asking how close we are to the next crisis. In the market for corporate loans, investors have fulfilled at least one prerequisite: They’re dropping their guard.

The financial cycle has a lot to do with inattention. When something bad happens, people are careful for a while. Then if all is fine for long enough, they forget that bad things can happen. This false sense of security leads to precisely the kind of behavior that precipitates the next crash.

The corporate debt market has a sort of proxy for inattention: the prevalence of covenants. When lenders are being vigilant, they require that borrowers avoid taking on too much debt or generate ample cash for interest payments. When they loosen up or get desperate for someone to take their money and pay interest, such covenants disappear.

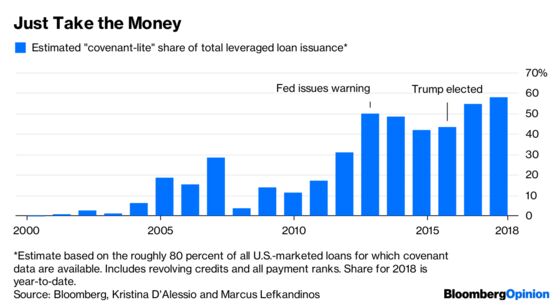

So what’s happening these days? “Covenant-lite” deals are booming among leveraged loans, a sort of subprime debt often employed in corporate acquisitions. So far in 2018, they have constituted an estimated 58 percent of all issuance by dollar value. That’s the largest share in at least a couple decades, with the exception of 2017. Here’s a chart:

The lack of caution has coincided with the ascendance of Donald Trump to the presidency. Back in 2013, regulators issued a warning about the mounting risks and declining vigilance in the leveraged finance market — an unusual move that, judging from the subsequent decline in covenant-lite lending, might have had some effect. But after the Trump administration arrived with its tax cuts and deregulatory agenda, the party resumed.

It’s not likely to end well. Although leveraged loans — and the structured investments, known as collateralized loan obligations, into which they are often packaged — performed well in the last crisis, Moody’s has warned that next time will probably be worse. Given the weaker protections, default rates will most likely be higher and losses steeper.

None of this means that leveraged lending will precipitate a full-blown crisis. Much depends on where the risk is concentrated. If investors are widely dispersed and defaults cause the market to seize up, the biggest problem could be on Main Street as companies fold because they can neither pay nor refinance their debts. If losses crystallize in institutions central to the financial system, the repercussions could be greater. It’s something to which regulators should definitely be paying attention.

To contact the editor responsible for this story: Philip Gray at philipgray@bloomberg.net, James Greiff

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Whitehouse writes editorials on global economics and finance for Bloomberg Opinion. He covered economics for the Wall Street Journal and served as deputy bureau chief in London. He was founding managing editor of Vedomosti, a Russian-language business daily.

©2018 Bloomberg L.P.