.jpg?auto=format%2Ccompress&w=200)

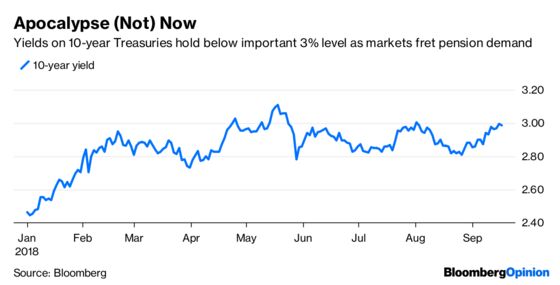

(Bloomberg Opinion) -- The bond market’s impending doom has been predicted so many times in recent years that it's hard to keep track, from the start of the Federal Reserve's interest-rate increases back in 2015 to the central bank finally beginning to shrink its balance sheet assets toward the end of 2017. And yet, while bond returns have been subdued and yields on average across all maturities are the highest since the start of 2014, it's been nothing even remotely close to the apocalypse-like scenario outlined by the mega-bears.

That brings us to Monday, the first trading day after Sept. 15, a date that many said would likely mark the final nail in the demand coffin for long-term bonds because of pending tax law changes. More specifically, companies with an unfunded defined-benefit pension liability could take a tax deduction at the old 35 percent corporate tax rate if they funded it before Sept. 15. After that date, the deduction rate fell to 21 percent. But instead of falling out of bed on a sudden lack of demand from pensions, 10- and 30-year Treasuries barely budged and yields held steady.

One of the things that the bond bears tend to discount is the tremendous amount of money created by central banks since the financial crisis that is searching for a home. The collective balance-sheet assets of the Fed, European Central Bank, Bank of Japan and Bank of England stand at 37 percent of their countries’ total GDP, up from less than 10 percent in 2007, data compiled by Bloomberg show. Another big thing the bond market has going for it is that more investors seem to be worried about relatively high stock-market values and the possibility of a looming equity sell-off. That should make fixed-income assets more attractive. JPMorgan Chase & Co. strategists noted in July that less than half the global tradeable bond universe is held by non-bank investors, the lowest share ever, which should provide support as those investors rebalance their portfolios. Goldman Sachs Group Inc. strategists wrote in a report Monday that they expect state and local defined-benefit plans will continue buying Treasuries. "Some rough calculations suggest the above factors could lead to buying totaling about $400 (billion) over the next (five) years, and would likely outweigh any marginal decline in tax-related buying," they wrote.

DOLLAR DOLDRUMS

It's fashionable to blame the struggles in emerging markets on a strong dollar, except it hasn't really gotten any stronger. Yes, the Bloomberg Dollar Spot Index had a moment between mid-April and late June, rising about 6.5 percent. But since then it's done nothing, falling over the past one, two and three months. "Despite rising expectations about the pace of U.S. rate hikes in 2019 and continued concerns about the impact of a trade war as well as ongoing volatility in a range of emerging markets, it's nevertheless noticeable that the (dollar) has underperformed over the past month against a surprisingly wide range of currencies," BNY Mellon chief currency strategist Simon Derrick wrote in a report Monday. Perhaps the greenback's struggles are just a reflection of the U.S.'s deteriorating fiscal position. The U.S. budget deficit widened to $898 billion in the 11 months through August, exceeding the Congressional Budget Office’s forecast for the first full fiscal year under the Trump presidency and up from $666 billion in all of fiscal 2017. "A budget deficit that's heading toward ($1 trillion) at a rapid pace while the economy's growing above potential is going to scare the FX market when the slowdown hits, as it surely will," Kit Juckes, a global strategist at Societe Generale SA, wrote in a Friday report. "The dollar's going up by the stairs and risks coming down by the elevator, starting sometime in 2019."

METALS MELTDOWN

The Trump administration is on the verge of releasing the final list of as much as $200 billion of Chinese products that will be hit with a new 10 percent tariff, according to Bloomberg News. Few areas of the markets have been impacted more by the trade war between the world's two-largest economies than industrial metals. The Bloomberg Industrial Metals Subindex, which tracks aluminum, copper, nickel and zinc, fell as much as 1.56 percent Monday, bring in its decline since early June to about 30 percent. The decline suggests that at least commodities traders are concerned that the showdown will derail otherwise strong economic growth in the U.S. and China, according to Bloomberg News. “We can see no winners in this conflict, and believe that global trade and the global economy will suffer mainly as a result,” Commerzbank AG analysts including Daniel Briesemann wrote in a research a note, referring to the new round of U.S. tariffs on Chinese imports. “Base metals are very dependent on economic cycles and therefore react sensitively to them.” Already, the Paris-based Organization for Economic Cooperation and Development said late last month that international trade in merchandise by the world’s biggest economies contracted for the first time since 2016, dropping a seasonally-adjusted 0.6 percent in the second quarter when expressed in current U.S. dollars, while imports declined 0.9 percent.

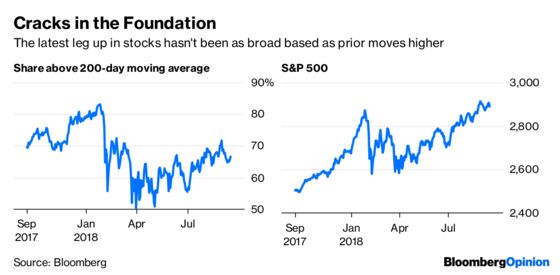

BAD BREADTH

U.S. equities dropped on Monday as a fresh round of tariffs loomed, with technology-related stocks dragging the S&P 500 Index down for the first time in six days. Even before declines, there was rising concern about the underlying strength of equities. While last week’s rally saw the S&P 500 finish 0.3 percent from a record, it came with relatively shallow breadth, according to Bloomberg News's Elena Popina. About 67 percent of members are trading above their 200-day moving average, compared with 72 percent when the benchmark hit its latest high in August and 83 percent during the high prior to that in January. On top of that, there’s elevated demand for options that provide protection against a sell-off in tech companies. Specifically, contracts that pay off if the Nasdaq 100 falls are in greater demand than similar hedges against losses in both the S&P 500 and the Russell 2000 Index, according to Bloomberg News’s Sid Verma and Dani Burger. The three-month metric, known as skew, is one point above the five-year average, placing appetite for hedges in the 76th percentile, data compiled by Bloomberg show. In addition, the Cboe SKEW Index breached 150 last week, reflecting a surge in demand for out-of-the-money put options versus calls on the S&P 500, according to Bloomberg News's Yakob Peterseil and Verma. The elevated level may be a sign that some investors believe a blow-up in U.S. stocks — returns two or more standard deviations below the mean, also dubbed a ‘black-swan’ event — isn't out of the question.

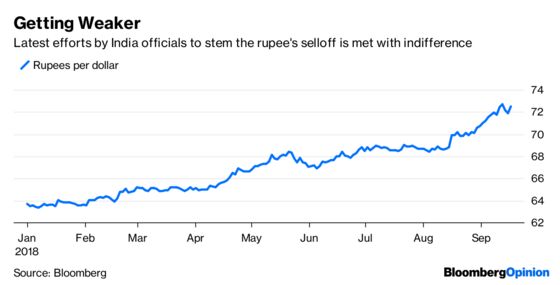

INDIA UNDERWHELMS

The situation in India, one of the bellwether emerging markets, is quickly spiraling out of control — at least judging by that country's financial markets. The rupee slumped about 1 percent on Monday to bring its decline for the year to some 12 percent. The S&P BSE Sensex of Indian equities lost 1.3 percent, suggesting the rupee's weakness is no longer a net benefit to the economy but rather a headwind. What makes Monday's weakness concerning is that India’s government announced steps late on Friday to boost capital flows and curb the ballooning current-account gap. The measures included easing restrictions on overseas borrowing by local manufacturers, potentially relaxing the cap on foreign ownership of individual company bonds, tax breaks on rupee debt sold abroad and limiting “non-essential imports,” according to Bloomberg News's Subhadip Sircar and Kartik Goyal. Market participants weren't impressed. “The measures announced were more at the margin,” said Ashish Vaidya, head of trading at DBS Bank Ltd. in Mumbai. “More concrete measures like detailing the import control measures or opening a dollar window for oil refiners will be positive.”

Government bonds briefly sold off on speculation the Reserve Bank of India will need to boost interest rates to support the rupee. Benchmark 10-year yields climbed as high as 8.18 percent before reversing to drop three basis points to 8.10 percent.

TEA LEAVES

There's been a lot of whispering among market participants lately about whether it's time to start worrying about the health of the housing market. Sales have slowed along with price gains, and nobody is sure whether that's because of declining consumer demand or a lack of inventory. Perhaps some answers will be revealed this week along with a slew of housing data. On Tuesday, an index of confidence among homebuilders compiled by the National Association of Home Builders/Wells Fargo is forecast to drop to the lowest level in a year. Then on Tuesday, the Commerce Department is expected to say that housing starts jumped 5.7 percent in August after a disappointing 0.9 percent increase in July. Finally, on Thursday the National Association of Realtors is expected to say that existing home sales rose by a modest 0.6 percent in August after dropping 0.7 percent in July to the lowest level since early 2016 and the fourth-straight monthly decline.

DON'T MISS

The S&P 500 Has a Tangible Net Worth Problem: Stephen Gandel

Value Versus Growth Plays Out in Emerging Markets: Nir Kaissar

Prime Time Returns for U.S. Money-Market Funds: Brian Chappatta

Financial Crisis Killed Hedge-Fund Performance: Barry Ritholtz

Here's One Likely Cause of the Next Crisis: Mark Whitehouse

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.