(Bloomberg Opinion) -- Long before Volkswagen AG created a separate umbrella structure for its luxury brands, Ford Motor Co. had something similar. Established in 1999 by then chief executive Jacques Nasser, Ford’s Premier Automotive Group (PAG) would eventually comprise Aston Martin, Jaguar, Land Rover and Volvo Cars.

Ford’s $12.6 billion loss in 2006 and an ensuing autos sales collapse meant it could no longer afford such trinkets. Within four years, new boss Alan Mulally had sold all the PAG brands at a knockdown price.

A decade later, Ford investors might wish he’d kept them. A $7 billion restructuring of Ford’s mostly unprofitable international operations is looming, and the shares have tumbled to levels similar to the end of the 2009 recession. By contrast, Aston Martin’s Kuwaiti and private equity owners are preparing an IPO, China’s Zhejiang Geely Holding Group Co. wants to do similar with Volvo (although it’s holding fire for now), and Jaguar Land Rover is by far the biggest contributor to the profits of India’s Tata Motors Ltd.

Last year, Volvo, JLR and Aston Martin generated $6.8 billion of Ebitda between them — about 60 percent of what Ford achieved. Indeed, judging by Tata’s market value and the admittedly optimistic valuation estimates mooted for Volvo and Aston Martin, the castoffs might be worth more than Ford, whose market capitalization has fallen to $37 billion.

Ford is struggling because it doesn’t make enough SUVs, is losing ground in China, and appears to have fallen behind in electric vehicles. How its new boss Jim Hackett must wish he had Jaguar’s I-Pace electric vehicle to call on, or its lineup of luxury Range Rovers. Sweden’s Volvo promises that all of its cars will have an electric option from next year and its sales are growing well in China. A $2.6 million Aston Martin Valkyrie supercar would be the perfect retort to anyone suggesting that Ford has gone stale.

So did Mulally err by selling Ford’s luxury assets? Not really. For starters, he had little choice. The company avoided a government bailout only by mortgaging its assets, including the Ford brand name, to fund a mammoth restructuring. It had to slim down and bring in cash. With everything else that was going on, you can forgive Mulally for not wanting to nurse a collection of loss-making European car brands back to health.

Freed from Ford’s ownership, Volvo, JLR and Aston Martin have all benefited from having more focused management, as well as the careful nurturing of their brands and not having to scrap with each other for investment. They’ve been lucky too. In 2008, rising pump prices threatened to kill off SUVs. But a decade later, gas-guzzler sales are booming again. That’s pretty handy for JLR as SUVs make up about 85 percent of its sales, according to estimates from Evercore ISI.

Meanwhile, thanks to Ferrari NV’s supercharged share price, Aston Martin’s backers argue that it too deserves to be valued at a luxury fashion label’s earnings multiple. Similarly, the Softbank Vision fund’s $2.25 billion punt on General Motors Co.’s Cruise autonomous car unit is helpful for those pitching Volvo as a public company. It has driverless partnerships with Autoliv Inc. and Uber Technologies Inc.

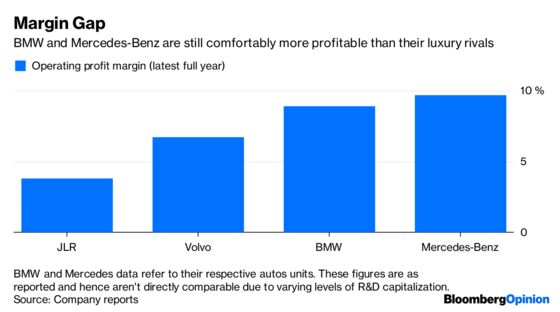

Yet despite all the recent buzz around PAG’s old roster, once shouldn’t overstate the strength of these companies. Compared to Mercedes-Benz and BMW, JLR and Volvo are sub-scale. The Germans sell four times as many vehicles annually, which helps spread the cost of technology investments. That’s one reason why BMW and Mercedes’ profit margins are higher.

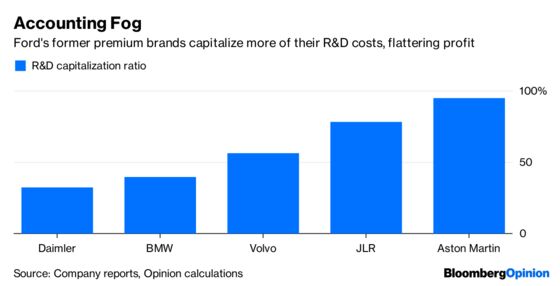

Volvo, JLR and Aston Martin’s reported profits are also flattered by their capitalizing of large research and development spending, rather than expensing more of it via the profit and loss statement. That may explain why they don’t generate much cash. Both Volvo and JLR reported negative free cash flow in the most recent fiscal year, while Aston Martin only broke even. JLR and Aston Martin still use Ford engines.

Having cruised during its first years with Tata, JLR has hit a particularly rough patch. Brexit, falling diesel sales, pricing pressure and heavy spending have all taken a toll. Last year’s 3.8 percent operating profit margin is very low when you consider the sticker price of its vehicles.

Nor is the broader context for carmakers worry-free. Sales have been pretty buoyant for about eight years now, but the industrial cycle is getting old and trade tensions don’t help. The values of listed autos companies have fallen, which probably explains why Volvo has paused its IPO plan.

So while it would be easy to look wistfully at Jaguar, Land Rover, Volvo and Aston Martin as the premium cars that got away, it would be too simplistic. If another recession hits, Ford will have four fewer problems to deal with. Investors may yet thank Mulally for that.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2018 Bloomberg L.P.