China’s Imperial Growth Delusion Just Won’t Die

(Bloomberg Opinion) -- The big state-owned Chinese enterprise is back. But this time, it isn’t looking sturdy enough to prop up the economy.

As growth stumbles, Beijing is falling back on a tried and trusted solution: using large, government-backed companies to spur activity. That’s squeezing out private and small firms.

The economy certainly merits concern. Trade frictions and Beijing’s crackdown on the underbelly of the financial system have combined to sap confidence. Higher borrowing costs, weak household spending and rising prices point to the beginnings of what could be a wider consumption downgrade. Meanwhile, fixed-asset investment growth is near record lows, and the fiscal situation is looking increasingly constrained.

A superficial reading suggests the renewed pulling of state levers is working: Chinese industrial-company profits are humming along, climbing 16 percent in July from a year earlier. Earnings at state-owned enterprises rose 24 percent, almost double the 13.4 percent rate for private companies.

A closer examination presents worrying signs. While upstream industries such as mining and energy posted gains of more than 100 percent, manufacturing sectors like machinery and equipment slowed sharply.

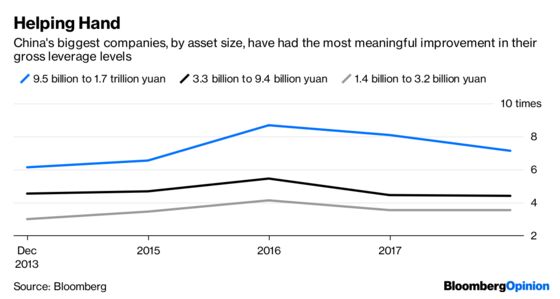

Drill down through other encouraging data and there’s a similarly mixed picture. A measure of Chinese companies’ ability to service their debt has improved, leverage levels have stopped rising, and their liquidity in the form of cash to short-term debt is at its highest level in a decade.

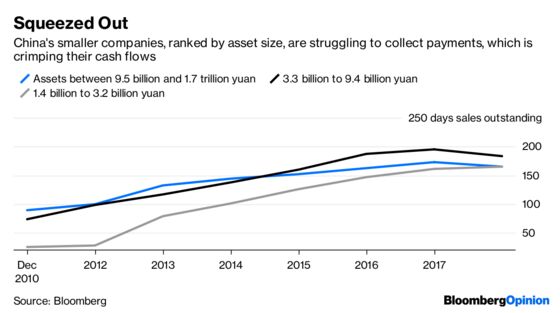

But for private companies, measures of debt are still broadly climbing. They also lack the preferential access to cheap credit of their state-owned counterparts. Operating conditions for small companies are getting worse, they’re holding inventory for longer, and the time it takes them to convert working capital into cash is increasing, Goldman Sachs Group Inc. found in an analysis of more than 4,000 Chinese companies.

Key to the resurgence of gargantuan national champions such as China State Construction Engineering Corp. have been supply-side reforms including strict curbs on environmentally unfriendly companies and factory closures in industries with overcapacity. President Xi Jinping’s Belt and Road Initiative has also driven business their way.

These policies have pushed out marginal players. Meanwhile, the wide-ranging campaign to reduce debt has hurt demand and left private, smaller companies in the lurch. The number of money-losing private industrial companies jumped about 40 percent as of June from a year earlier, while the number of unprofitable state-backed firms stayed flat.

China has a long history of using state-owned behemoths to drive economic activity — dating back to imperial times. Such industrial giants first appeared during the Qing dynasty in 1864, as the government attempted to revive a weakened economy after the end of the Taiping Rebellion. What little industrialization resulted from the so-called Self-Strengthening Movement “was characterized by a focus on heavy industries’ serving the government’s military and defense purposes,” as historians William Goetzmann and Elisabeth Koll wrote in “A History of Corporate Governance around the World: Family Business Groups to Professional Managers.”

One difference this time: Beijing has talked about bolstering small and medium enterprises through legal protections and providing more credit. Under former Premier Zhu Rongji in the 1990s, the plan was explicitly to “grasp the large, let go of the small.”

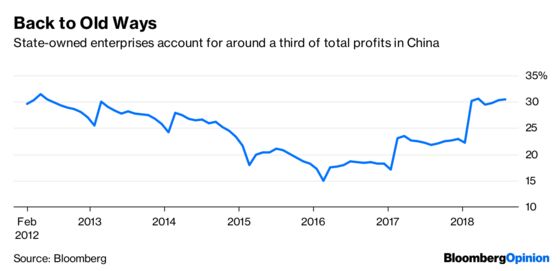

History shows that private companies have far higher productivity. Their average returns on assets have been 4 to 6 percentage points higher than SOEs over the past two decades. The more the state sector contributes to gross domestic product, the worse it is for the economy’s long-term efficiency and productivity. Given that state enterprises now account for almost a third of all Chinese profits, up from 15 percent in early 2016, that should be a concern.

Even over the past decade, repeated mergers and de-mergers of several national champions (some of which are now being recombined) haven’t produced any real victors. Efficiency, earnings and returns on equity have declined. China combined two rail equipment makers in 2015 into CRRC Corp., a company with a market value of about $130 billion: Return on equity has fallen since then to about 11 percent from 13.5 percent pre-merger, and margins have been flat at about 5 percent. Listed SOEs have traded at discounts to their private peers.

Effectively suppressing private companies — especially now, when the state’s purse is looking smaller and its ability to prop up state-backed giants is constrained — isn’t sustainable. State-owned companies depend on government spending rather than solely demand like their private-sector peers, but fiscal revenues are falling sharply. Even though industrial SOEs look to have improved, they still carry the bulk of stressed debt in the system.

In the latest example of the squeeze, Beijing is planning to extract more in tax from companies to replenish state coffers for an aging population. China’s social security tax rate is the highest in the world at around 43 percent, versus 13.3 percent in the U.S. and 30 percent in Japan, according to Nomura Holdings Inc. The tax changes could dent profits by 2.5 percent next year and cut investment by around 1.1 percent, the Japanese brokerage estimates. Private enterprises, or employers, are the biggest contributors to social security tax in urban areas, paying almost twice as much as SOEs.

Running the private sector dry has never helped Chinese emperors. This time won’t be any different.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2018 Bloomberg L.P.