Amazon Makes Good on Business-to-Business Threat

Amazon.com is no longer a looming threat for sellers of factory-floor basics, lab equipment and office products.

(Bloomberg Opinion) -- Amazon.com Inc. is no longer a looming threat for sellers of factory-floor basics, lab equipment and office products. It’s a full-blown competitor.

The e-commerce giant rattled distributors of industrial parts, IT and medical supplies in 2015 when it launched a business-to-business platform that promised to make ordering supplies as easy and price-transparent as ordering diapers or toothpaste. On Tuesday, it said that platform, Amazon Business, had hit an annualized rate of $10 billion in global sales. That compares with $1 billion in U.S. sales in its first year of existence before Amazon expanded the platform into other countries including the U.K., Germany and Japan.

For context, W.W. Grainger Inc., the largest U.S. industrial distributor, had about $10.4 billion in sales last year and is expected to bring in $11.3 billion this year. This isn’t a perfect comparison, but it’s striking how neck-and-neck Amazon has become with incumbents after only a few years. In its characteristically vague fashion, Amazon says the platform now serves “millions of business customers.” It could be 2 million or 10 million, I have no idea. But that compares with “more than 1 million” U.S. customers as of July 2017 and either way, the ongoing growth seems like bad news for Grainger.

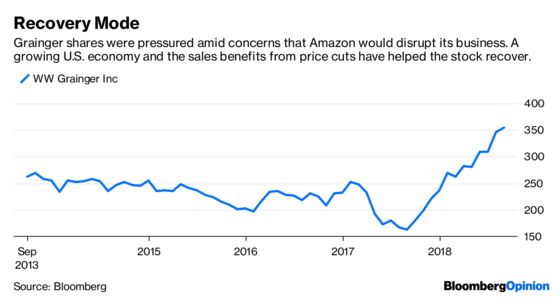

The $20 billion company has weathered Amazon’s push into its territory better than I had expected. Grainger is one of the best performing stocks on the S&P 500 Industrial Index this year amid booming volume growth that’s due in part to draconian price cuts it implemented to stay competitive in the age of Amazon. The true test for the company will be the back half of the year, when it faces tougher comparisons as it laps those cuts made in 2017. Grainger is expected to report third-quarter results in mid-October.

RBC analyst Deane Dray has argued volume growth may be tempered without additional cuts as Grainger still doesn’t offer the lowest prices. That would put additional pressure on gross margins that are already expected to settle at the lowest level in more than a decade in 2018. Over the longer term, I still struggle to see how Amazon’s entrance into the industrial distribution market doesn’t herald a deeper, more structural reset of incumbents’ profitability.

As a final note, Amazon’s steady march into the world of business-to-business commerce underscores the potential of its logistics investments. In its Tuesday statement, Amazon noted that third-party sellers drive more than 50 percent of the $10 billion in global sales. Those are the types of vendors that may be interested in tapping Amazon to not only provide a marketplace for their products but to deliver them as well, opening up a much wider customer pool than sellers of consumer-facing goods. Businesses tend to be more profitable customers for shipping companies because they order in bulk and drivers don’t have to make as many stops.

This is a space to watch.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2018 Bloomberg L.P.