(Bloomberg Opinion) -- Americans like to celebrate the wealthy. The Chinese, Crazy Rich Asians aside, tend to be a lot less indulgent.

That goes some way to explaining Jack Ma's plans to retire as Alibaba Group Holding Ltd.'s co-founder and the almost daily unwinding of China’s once high-flying (debt-fueled) private conglomerates, including HNA Group Co. and Dalian Wanda Group Co.

Ma said Monday he’s stepping down as executive chairman in September 2019, marking his 55th birthday, to focus on philanthropy and education. Chief Executive Officer Daniel Zhang will succeed him at Asia’s most valuable company, though Ma will stay on the board until 2020.

Ma's impact can't be understated: The online marketplace the former English teacher founded with 17 others in Hangzhou has transformed China. Alibaba is the nation’s top e-commerce player, has created the country’s Alipay, dominant payments system, runs cloud-computing and wealth-management companies and expanded its reach to India and Southeast Asia. With so many Chinese using its services, the company also aggregates the kind of personal data Beijing can only envy.

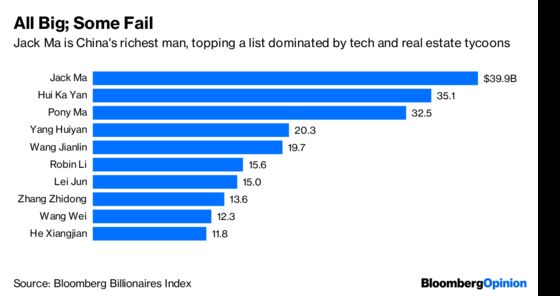

In the process, Ma also became China's richest man. That's a potentially dangerous position to be in, as any student of Chinese history knows.

Time and time again, Chinese billionaires on lists of the super-wealthy – people whose activities tend to sap the business of state-owned players – have been cut down to size. The latest round focused on those private conglomerates that, in less than a decade, accumulated assets like trophy buildings in the U.S. The global spree stoked concern about the projection of so-called soft power. Two years ago, wary of capital flight and mountains of corporate debt, Beijing began targeting the conglomerates.

Fosun International Ltd., which acquired France’s Club Med SAS resort chain several years ago, is back in the buying game. But founder Guo Guangchang knows how risky debt-fueled acquisitions can be: He briefly “vanished” in 2015, just as Fosun’s overseas acquisitions were peaking.

Wanda's Wang Jianlin remains one of China's richest men, but the real estate and mall operator has been on a great unwinding mission ever since it fell foul of over-borrowing in July 2017.

Under Wu Xiaohui, whose ties to Deng Xiaoping gave him considerable political capital, Anbang Insurance Group Co. paid over the odds for Manhattan’s Waldorf Astoria hotel, and even attempted to buy Starwood Hotels & Resorts Worldwide LLC. He was sentenced to 18 years in prison for fraud in May.

HNA, roiled by the sudden death in France of Co-Chairman Wang Jian in July, is now busy shrinking back toward the regional airline it once was. The conglomerate has sold more than $17 billion in assets this year alone, and is now planning to dispose of its entire stake in Deutsche Bank AG.

China’s tech giants, from Alibaba to Tencent Holdings Ltd., have been similarly acquisitive. The difference is they haven’t had to rely on debt. While they’re unlikely to be compelled to unwind their expansion in the same way as the conglomerates, tech’s too-big-to-fail status is at risk.

Tencent’s Pony Ma has been famously low-profile, but Beijing’s freeze on new games threatened his company. Meanwhile, Alibaba’s more gregarious Ma raised some eyebrows when he met with President Donald Trump to discuss the creation of 1 million new U.S. jobs – three months before President Xi Jinping had his first meeting with his American counterpart.

Ma may be wise, then, to talk of stepping down now, before the heat is turned up. He remains in the 36-member Alibaba Partnership that oversees the company, so even with a stake of about 5 percent, his stamp on the New York-listed firm won’t be lost. Ma is still admired for Yoda-like wisdom at a time when his rival Richard Liu, founder of JD.com Inc., the second-largest e-commerce company, faces allegations of rape.

China needs its private-sector entrepreneurs to provide the jobs its famously inefficient state firms can’t. Ma’s impending retirement may be part of a bigger cautionary message that they should perform that task without getting too big.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2018 Bloomberg L.P.