Millennials Dreaming of Retiring at 30 Have a Math Problem

(Bloomberg Opinion) -- At a time of stagnant wages, high student debt and dead-end jobs, it’s no surprise that millennials in their 30s are now dreaming of dropping out of the rat race and retiring early. But presenting this as a goal achievable to anyone prepared to live frugally and invest carefully looks like a sham. We do not quit our jobs as equals.

Last week’s New York Times story, “How to Retire in Your 30s With $1 Million in the Bank,” was the latest in a line of profiles touting financial freedom in the name of FIRE — “Financial Independence, Retire Early.” Parsimony, or cost minimization, is prioritized over greed, or revenue maximization.

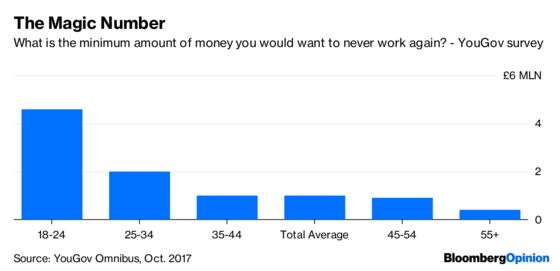

The principles of nickel-counting and index investing are laudable, but the case studies look extreme. One 43-year-old retiree and his wife attained a $1.2 million fortune after five years of “drastically” cutting costs. One small detail: He earned a six-figure salary and owned a four-bedroom house. If you’re going to down-size, it helps to have size to begin with.

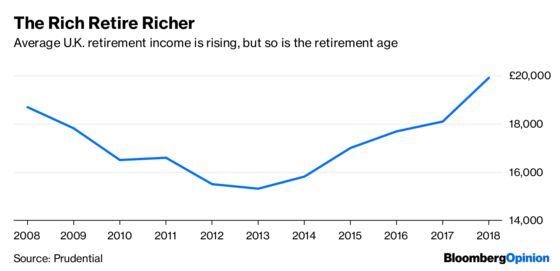

Those without a head-start will find such goals a stretch. In the U.K., the median salary is around 20,800 pounds ($27,000) after tax, according to data from the tax authorities. Assume half of that goes on needs and 30 percent on wants. That leaves 4,160 pounds for savings per year. All things being equal, on this wage alone it would take 55 years to save 230,000 pounds, assuming zero interest, or 430,000 pounds, assuming 2 percent compound interest. Even a life of monastic discipline, spending only on housing and necessities, would require 25 to 30 years of work to get to the above, admittedly broad-brush, numbers that still fall short of the minimum pension pot experts say non-homeowners require.

Turbo-charging returns without a gift from the Bank of Mom and Dad means taking risks. Here again, the gospel of FIRE seems to preach sensible, low-cost, passive investing in index funds, rather than extremes like trading cryptocurrencies. But even the S&P 500’s annualized total return of 14 percent over the past five years would only turn into a million dollars if there was $600,000 there in the first place. And those budgeting for their retirement future based on recent returns may end up as disappointed as savers who found themselves able to retire early at the peak of the dot-com bubble — until it burst.

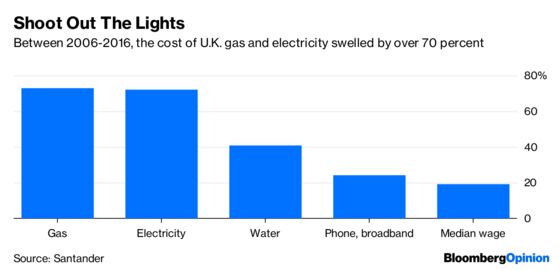

Moreover, feel-good frugality like home-brewed iced coffee or cheap online entertainment at home doesn’t offer immunity to financial risks after retirement. A 2016 Schroders study of retirement in Australia, where pension contributions are mandatory, found that retirees spent less, but became more sensitive to price increases in necessities like utilities and food. The net impact between 2005 and 2015 was a rise in overall income requirement, putting greater pressure on funding. Not all costs can be predicted.

There’s still a lot to like about FIRE, which is as much cultural as it is financial. People are reassessing their relationship to work after the financial crisis, which exposed glaring injustices in the way capitalism functions. Freedom from debt and a scale-back from full employment to partial retirement — whether through freelance work, barista shifts at Starbucks or bagging groceries — is being re-evaluated as worth the cost. That’s fair.

But there’s still something of the rat race about this race to retirement. Not everyone has access to a Volkswagen camper van, or income from a rented apartment. Dropping out of work early in the belief that easy, non-demeaning freelance work will always be available seems very optimistic. Fingers will still get burned.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering finance and markets. He previously worked at Reuters and Forbes.

©2018 Bloomberg L.P.