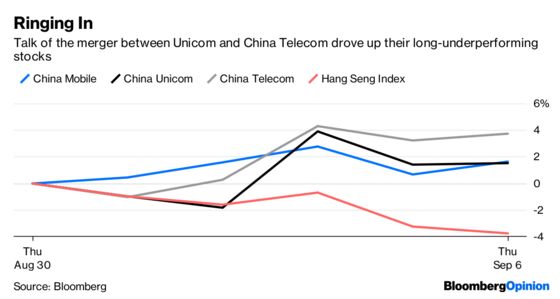

(Bloomberg Opinion) -- State technological, geopolitical and social objectives are the driving force behind what could be China’s biggest-ever telecom merger. Shareholders celebrating the deal might do well to remember that.

Beijing’s motivation is to seek an edge over the U.S. in 5G. The next-generation wireless technology may be 100 times faster than 4G, enabling a revolution in connectivity of everyday objects from refrigerators to traffic lights. It will also pave the way for driverless cars and, some fear, make spying a lot easier.

Whoever leads the world in 5G may lay the soil for development of the next Apple Inc. or Amazon.com Inc. “5G is the glue that makes smart cities work,” said Bernstein Research analyst Chris Lane.

Those grand ambitions sound exciting, but what do they mean for investors in the companies that will build these networks? China’s Ministry of Industry and Information Technology said in May last year that 5G would involve investments of $411 billion by the country’s telecom operators between 2020 and 2030. The figure sent “shockwaves” through the sector, according to HSBC Holdings Plc.

Merging the parents of Unicom and China Telecom will reduce the burden by enabling them to share investment in a single network, but the ministry’s figure is still more than five times their combined market value. China Mobile Ltd., by far the biggest of the trio of operators, has a market capitalization of about $195 billion.

China often treats its state-owned companies as tools of government policy — shuffling assets, merging and splitting corporations to suit strategic aims even after they have been listed. Such maneuvers haven’t always worked out well for investors.

Unicom itself is the result of a $29 billion merger with the former China Netcom Group Corp. carried out a decade ago. The rationale for that deal was to strengthen Unicom’s ability to compete with China Mobile as the country prepared to move to 3G.

Between listing in Hong Kong in 2000 and the Netcom purchase, Unicom stock returned about 30 percent including dividends, according to data compiled by Bloomberg. In the decade since then, it’s lost about 26 percent.

The three Chinese carriers trade at enterprise-value-to-Ebitda multiples of just over three, compared with 9.3 times for AT&T Inc. and 7.8 times for Verizon Communications Inc. That valuation discount partly reflects the anticipated costs of upgrading to 5G — but also investors’ recognition that the companies must do the bidding of Beijing, which may have wider social objectives. For instance, carriers have been under pressure to keep customer tariffs down, and this year lost the right to charge roaming fees across the country.

Investors in China Tower Corp., which listed in Hong Kong only last month, may be among the first losers if the current merger plan goes ahead. A Unicom-Telecom combination would reduce its number of long-term cellphone tower tenants to two from three. China Tower shares fell 14 percent this week through Wednesday, before rebounding 3.9 percent Thursday. The stock is still trading below its IPO price.

To be sure, China’s also giving its telecom operators a leg up: Beijing is allocating spectrum to the trio later this month at no cost to the companies beyond a small annual fee, enabling them to preserve cash for network spending. U.S. carriers, on the other hand, will have to fork out billions of dollars in auctions.

Perhaps China’s 5G rollout will unleash a boom that, besides benefiting consumers and creating opportunities for gear-makers and entrepreneurs, will also drive profits for the service providers. Investors in Chinese telecom companies just need to know they’re not the first thought on the government’s mind.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2018 Bloomberg L.P.