When Will the Bleeding Stop in Emerging Markets?

(Bloomberg Opinion) -- Hedge funds haven’t been this bearish for years.

In the last month, funds quickly sold down their positions in emerging markets to levels last seen in August 2015, when China scared the world with a surprise devaluation, and early 2016, when Beijing terminated a silly experiment with circuit breakers in a futile attempt to rescue the stock market.

Emerging markets are in pain. Currencies alone are down 13 percent for the year as contagion starts to spread across continents, from Argentina to Indonesia. Bonds and stocks have tumbled.

When will the bleeding stop?

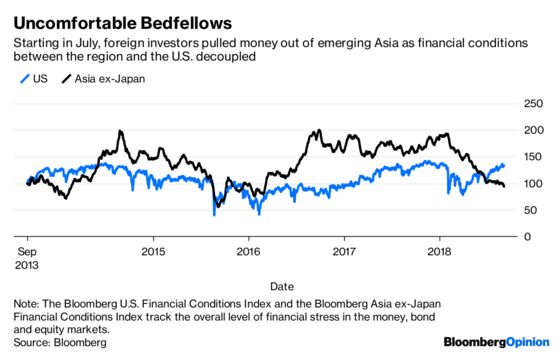

In a case of role reversal, the U.S. is starting to look rather like an emerging market. On a seasonally adjusted basis, the American economy grew 5.4 percent in the second quarter, almost as fast as China (if you can trust Beijing’s numbers). While the S&P 500 Index is staging a record bull run, China, the proxy for emerging markets, was in solid bear territory even before the recent sell-off started.

Money is coming back onshore in the U.S., Fed rate hikes or not.

Adding to the EM challenges, this American expansion now requires much more dollar funding than before, as the Federal Reserve shrinks its balance sheet. Until financing conditions reach equilibrium between the U.S. and emerging markets, expect the suffering to continue.

A good potential solution, much discussed in China, would be to echo President Donald Trump’s big corporate tax cut, especially considering China’s effective tax rate is the world’s 12th-highest. Don’t set too much store by the bureaucracy, though – changes are unlikely to come until early 2019, if at all.

The other path to equilibrium is a slowdown in the U.S. After all, the world is getting smaller. Can America really grow at a developing-nation pace when almost every other economy on the planet is flagging?

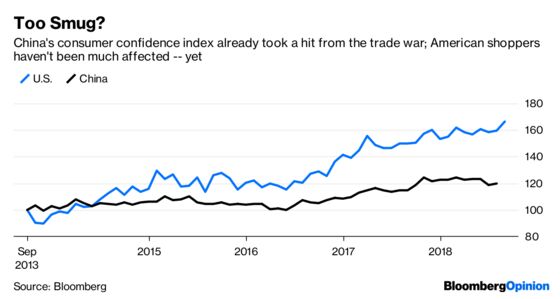

U.S. tariffs on as much as $200 billion of Chinese goods, which may go into effect as soon as Friday, will hurt American shoppers. According to the Peterson Institute for International Economics, 23 percent of the imports targeted by this round in the trade war are consumer goods such as computers, furniture and agricultural products. Any brake on consumer spending will rein in the economy.

Even so, it will be at least two months before negative sentiment shows up in U.S. consumer-confidence indexes such as those from the University of Michigan and the Conference Board.

A virus needs to burn through the system before the patient can start recovering. Emerging-market turbulence will be around for a while.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2018 Bloomberg L.P.