SEC Shouldn’t Open Up Unicorn Hunting to Mom and Pop Investors

(Bloomberg Opinion) -- Securities and Exchange Commission Chairman Jay Clayton says he’s looking at ways to open up the private market to mom-and-pop investors, allowing them the chance to get in on fast-growing companies like Uber Technologies Inc. and Airbnb Inc. Instead, he should be looking for a quicker way for companies to move from private to public markets, and back.

Earlier this week, Clayton, speaking at a conference for entrepreneurs in Nashville, outlined a proposal to make it easier for less-than-wealthy individuals to invest in private companies. Right now those investments are restricted to high-net-worth individuals. Clayton said the SEC will take a few months to deliver a “lengthy” paper on the matter, but not long after that the games would begin. “I think you could move pretty quickly on this kind of thing,” Clayton told the Wall Street Journal.

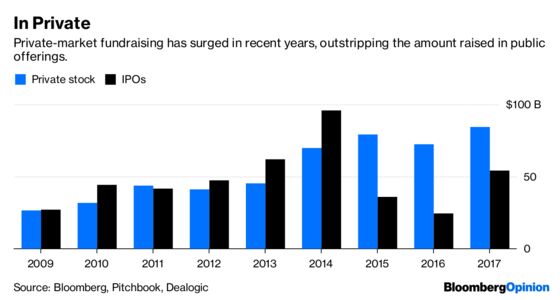

The proposal seems to mark an end to Clayton’s silly war on private markets. Ever since becoming head of the SEC nearly a year and a half ago, Clayton has repeatedly cited the shrinking number of public companies as a major problem. He has said the fact that Uber, Airbnb and other larger tech companies are staying private longer has robbed individual investors of the ability to get access to potentially high-return investments, as well as cut off a needed funding source for less-well-known companies that would like to go public. To remedy that, Clayton has proposed loosening regulations, which he says are discouraging companies from going public, but have also limited fraud.

Clayton’s new proposal is a recognition that the issue may not be that public markets are regulation-clogged and broken, but that private markets actually work quite well. The bad news is, Clayton’s proposal could put an end to that.

Yes, the private market has allowed Uber, AirBNB and other so-called tech unicorns to flourish. But there have also been widespread instances of aggressive accounting, failed businesses, and outright fraud — Theranos Inc., most notably. That, in part, has caused the hype around the tech unicorns that rose in 2015 and 2016 to subside. But it’s done so without the calamitous economic impact that accompanied the bursting of the dot-com and housing bubbles.

The private market’s ability to limit hype and investment is a feature, not a bug. If Clayton opens the market up to all investors, that feature is likely to go away, and fraudsters looking to take advantage of limited disclosure requirements are sure to flood in.

But what about those small, legitimate businesses that can’t get access to venture capital, perhaps because they aren’t on the coasts? Is there a way to grease the wheels for them to gain access to funding?

If Clayton is in the market for ideas, I have one of my own to sell—limited-life public companies, and I will throw in the trademark for free. The idea would be that smaller companies could go public as long as they promise to return a portion of the equity they have raised, say 10 percent, each year. Most small businesses don’t make very good public companies because they have a limited life span. My imagined structure solves that, being self-liquidating, with the companies using up their capital to buy back investors’ stakes until the company is either private again, or gone. Like a common stock, the value of the investment vehicle would rise and fall based on the company’s ability to pay out more, or less, than expected. But the constant capital return should limit investor losses. Financial disclosure could be limited, and in return companies could be required to set up a pre-funded capital-return account, or prove to an auditor that the company has the ability to do that.

I’m not sure this financial structure would take off. I could see how some entrepreneurs would say its cost of capital might be too high, especially given the current level of interest rates. But if the SEC is really looking to narrow the gap between public and private markets that Clayton thinks is holding back our economy, why not try something new? Giving individual investors the ability to lose their money in risky markets won’t cause funding resources or the economy to grow. In fact, it will likely do the opposite.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2018 Bloomberg L.P.