(Bloomberg Opinion) -- Financial markets are god-like in their ability to shrug in the face of extreme policy shifts. The conflagrations of Donald Trump's election and the U.K. Brexit vote were quickly smothered by faith in "synchronized" economic growth, low inflation and central bankers' willingness to keep interest rates low.

February's spike in market volatility seemed finally to prove the complacent hordes wrong, only for it to nose-dive once more – just as populism kept spreading.

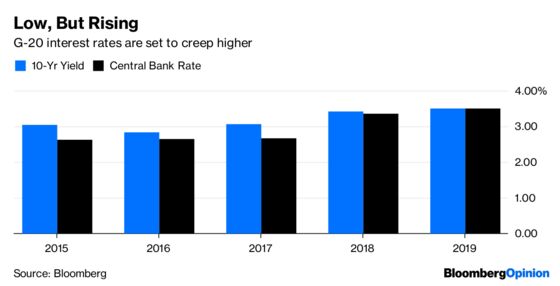

Things are unlikely to continue as they are. While predicting the return of volatility has been ultimately as futile as calling the top of history's longest-running bull market, it seems arrogant to assume we are past the worst of the political risk. Interest rates are rising and more governments are promising short-term gains whatever the long-term cost. A bet against volatility has room to get pricier and more painful.

The political consensus is changing. About 41 percent of G20 countries' economic output (plus Spain) is governed by populists, up from about 4 percent in 2007, according to Bloomberg Economics. Defining populism is obviously tricky – the U.S. under Trump is classed as populist while the U.K. isn’t – but there have been some sensible appraisals of what the common economic thread might be. Allianz Global Investors has predicted more protectionism, more inflation, a higher cost of borrowing and divergence between national “winners" and "losers" in a beggar-thy-neighbor world of protectionism.

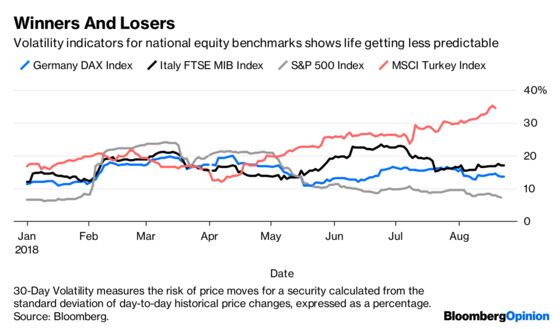

This tendency towards short-termism is eroding investor confidence and pushing up volatility in markets already at risk from rising interest rates and the withdrawal of U.S. dollar liquidity. Turkish President Recep Tayyip Erdogan has fanned the flames of his country's overheating economy by opposing rate hikes and deepened a diplomatic spat with Trump by calling for a boycott of U.S. goods. In Italy, the shock collapse of a highway bridge that cost the lives of at least 43 people has been cheaply politicized by the government in its budget talks with the European Union. Sentiment is febrile.

In this Darwinian world, where the dollar rules the roost and where top central banks are desperate to preserve stability, volatility in relative safe havens like the U.S. is likely to be lower than at the periphery. Investors are less jumpy when Trump tweets than they used to be. As unwelcome as his scatter-gun tweet-storms might be, there is confidence the technocrats are still in charge. Currency volatility in emerging markets is far outpacing that in the G7.

Still, it's likely that this uncertainty will seep into the core eventually. We are on a long journey towards higher volatility globally, as Miton Group portfolio manager David Jane puts it, and the conditions that led to February's spike in the VIX – rising rates, retrenched liquidity and hedge funds betting against price swings – are still there.

Political risk is hard to quantify, but Trump's bite has plenty of time to get worse than his bark. Look how his offhand tweet about South Africa’s land reform plans still sent the rand tumbling on Thursday. As the policy script gets torn up and rewritten, investors need to brace for more turbulence.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering finance and markets. He previously worked at Reuters and Forbes.

©2018 Bloomberg L.P.