(Bloomberg Opinion) -- I’ve long thought that Crown Prince Mohammed bin Salman’s life overlaps in curious but important ways with one Elon Musk, CEO of Tesla Inc. And now, MBS even has his own take on Musk’s “funding secured” meme.

The long-awaited initial public offering of Saudi Arabian Oil Co., or Saudi Aramco, has been put on hold, according to my colleagues in Bloomberg News. Given it is already two-and-a-half years since the sale was first mooted, “on hold” sounds a lot like “how about never?” For their part, the Saudi authorities, citing preparations made to date, insisted late Wednesday evening that the IPO hadn’t been cancelled — as Reuters had earlier reported — but that it would go ahead at a time of the government’s own choosing.

In any case, it’s fair to say that MBS’s confident proclamations about the mother of all IPOs were a tad premature and that $2 trillion valuation he spoke of was decidedly not secured (still, at least no one could mistake $2,000,000,000,000 for a joke about weed).

One obvious explanation for deferring the IPO further still is that while oil prices are far better than they were in early 2016, oil at $70-ish a barrel isn’t enough to pull the trigger. Obvious, but shallow. There’s a much bigger problem: Like Musk’s $420-a-share take-private tweet, the whole concept of the Aramco IPO was far too premature.

Bassam Fattouh and Laurence Harris of the Oxford Institute for Energy Studies nailed the issue in a report published in March 2017:

[T]he IPO can’t be isolated from the range of recent reforms and adjustments taking place in Saudi Arabia and the pace of these reforms will be key in determining the valuation of Saudi Aramco.

Put another way: MBS dropped the bombshell of an Aramco IPO as part of a marketing blitz for his bigger plan to reform the Saudi economy, and in doing so got things precisely backwards.

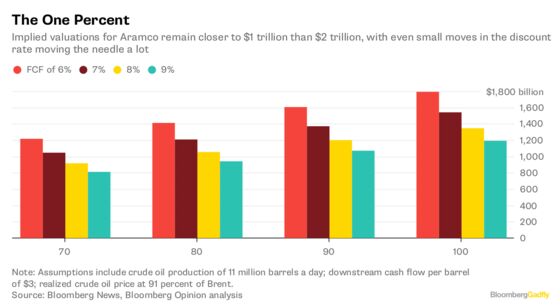

When I took a stab at valuing Aramco a few months ago, two things were clear. One, getting to $2 trillion under any reasonable set of assumptions was nigh on impossible. Two, the biggest determinant of whatever that number was going to be was the discount rate investors would put on Aramco’s free cash flow. This was, above all, a dividend story. Long-term oil-price assumptions mattered (another reason why it’s shallow to focus on today’s price) but the risk premium was the big swing factor, with a 1 percentage point move shifting things by $200 billion or more.

And that risk premium was tied inextricably to the Saudi reform project. State-owned oil companies, even one as highly respected as Aramco, are a tough sell to minority shareholders (see this). But they’re an easier sell if investors are comfortable with the state they’re in. Thus, for example, selling shares in Aramco wasn’t a necessary step in reforming Saudi Arabia’s subsidized domestic energy prices. But getting the latter done would tee up an eventual IPO nicely, both by showing evidence of wider economic reforms and removing a big burden from Aramco’s financial statements. Needless to say, stuff like rounding up princes and detaining them at Riyadh’s Ritz-Carlton or getting into a spat with the Canadians don’t settle nerves.

The same logic applies to the other reason MBS gave for the IPO, namely capitalizing the Public Investment Fund. This diversification of state funds — swapping some money out of Aramco to invest in other sectors — is often confused with efforts to diversify the Saudi economy, but shouldn’t be. The latter is the thing that will make or break the country as oil’s prospects start to dim.

The PIF can play a vital role in that by seeding non-oil businesses at home but it’s far from clear it will, having committed billions to foreign investments like a stake in Uber Technologies Inc. and funds run by SoftBank Group Corp. and Blackstone Group LP. Also, of course, it has apparently discussed helping to take Tesla private — according to Musk, anyway — and is reportedly toying with putting money into another U.S. electric-vehicle developer, Lucid Motors Inc. These make the PIF look more like a state hedge fund than a state accelerator. In any case, like those economic reforms, turning the fund into a more transparent organization with a clearer mandate would be something sensibly done before talking about injecting Aramco’s supposed trillions into it.

As it stands, the plan of having Aramco pay the PIF for its stake in Saudi Basic Industries Corp. achieves much of what Riyadh wants in the immediate term. The government insists an IPO could follow any such deal, depending on other factors. But why bother, given Aramco can borrow relatively cheaply and hand the money to the state anyway in what would amount to an elaborate dividend recap? In reinforcing the cat’s cradle of ties between the various fiefdoms of the kingdom, it doesn’t do much for the narrative of reform. But it does bring in cash and would avoid the hassle of listing shares.

In doing so, it would also underline what was always the case: Aramco’s IPO became the teaser for the Saudi reform program when it should properly be the coda.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.