What OPEC’s Good Year Really Means

(Bloomberg Opinion) -- The latest U.S. assessment of how much money OPEC rakes in from oil exports confirmed one thing: Cutting supplies worked.

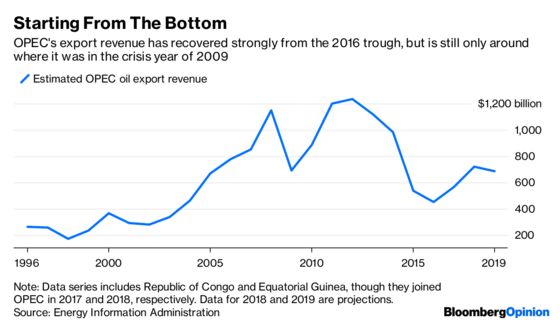

In its annual OPEC Revenues Fact Sheet, released Tuesday, the Energy Information Administration estimates OPEC’s export revenue was $567 billion in 2017, up 26 percent in real terms. That’s despite the group’s average crude oil production dropping slightly compared with 2016. Such is the magic of higher prices and collective supply restrictions.

Yet the numbers also show just how big a hole OPEC now finds itself in. Because 26 percent growth is great, obviously, but just how great depends on where you’re starting from:

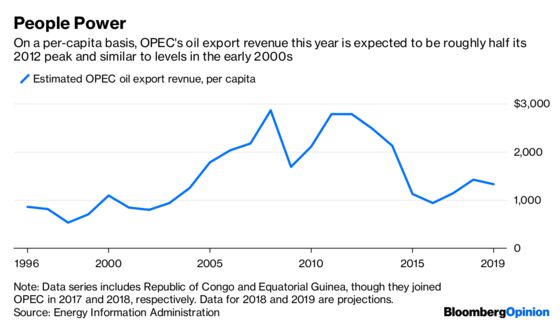

The scale of OPEC’s challenge becomes even clearer when you factor in population growth:

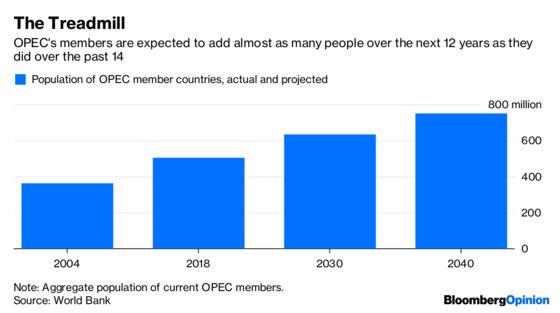

The EIA’s projection of just over $1,400 of revenue for each person in the OPEC countries this year is similar to what it was in 2004 (just over $1,250 in real terms). Back then, though, Brent crude oil averaged about $50 a barrel in real terms against a projection of almost $72 this year. Of course, having to share the spoils between an extra 140 million people — an increase of 38 percent — will tend to do that to the math. What’s more, the equation only gets harder: The World Bank projects OPEC’s population to rise by another 129 million by 2030.

Beneath the headline numbers there are vast disparities. Nigeria’s per-capita oil-export income last year was just $179 and change, the lowest in the group and a mere 1.5 percent of Qatar’s, which led with almost $12,000 per person. What’s more, in absolute terms, Nigeria accounts for more than half the expected increase in OPEC’s population by 2030.

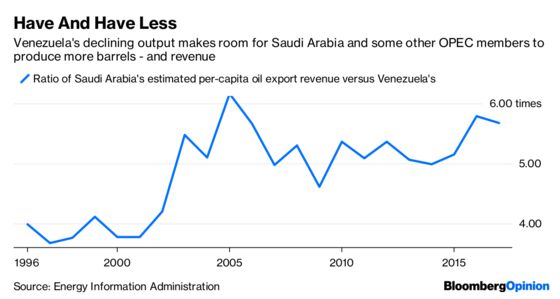

Let’s not forget Venezuela, where revenue per capita has slumped over the past several years on a combination of lower prices and lower production, with the latter making an outsize contribution to the supply cuts that have helped the wider group. The ratio of revenue for those living in OPEC kingpin Saudi Arabia versus those unfortunate enough to be in Venezuela tells that story. And given current production trends, that ratio will almost certainly tick higher this year:

If you’re wondering why the likes of Saudi Arabia are attempting to shift their economies away from being overly dependent on oil revenue — and quickly — these charts go a long way to explaining it. Saudi Arabia’s per-capita income from oil exports last year of almost $5,100 was less than half the level of five years before. And while it is bound to be higher this year on a combination of rising production and prices, a return to the heady levels of $10,000-plus per man, woman and child is unlikely absent a price-spike. There are, as usual, plenty of potential spike scenarios out there, encompassing everything from Iranian conflict to the effects of tighter regulations on marine fuel, but even today’s prices are having an impact on demand. Don’t forget, also, that higher prices encourage higher oil production in North America and other non-OPEC regions.

In a report also published on Tuesday, Bassam Fattouh and Andreas Economou of the Oxford Institute for Energy Studies examined the balancing act Saudi Arabia is striving to maintain this year. They conclude that OPEC’s de facto leader is trying to manage the oil market for now within a band of $70 to $80 a barrel as it tries to earn enough income without hurting demand (and also keeping on the right side of the White House ahead of midterms).

That is an extraordinarily narrow channel to navigate in the face of so many buffeting forces. The latter include chronic challenges presented by competing energy technologies, non-OPEC supply and efforts to fight climate change.

But these are compounded by another big one: OPEC’s own weaknesses. Countries like Saudi Arabia are attempting to manage transitions in both the energy market and their own societies, and all on reduced income from oil exports supporting expanding populations. Future price spikes may offer windfalls but would also do structural damage to oil demand. The apparent win of the past year should be set in the context of this broader fragility.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.