India’s GDP Fracas Could Hurt Modi and Maul Rupee Bears

(Bloomberg Opinion) -- Just as some analysts were starting to believe in a reset for the Indian rupee, with the government becoming more relaxed about letting it weaken, history got in the way.

The history in question is past GDP data, which haven’t been officially released after India reworked its calculation methodology in early 2015. But the report of a subcommittee tasked to suggest ways to link the old and the new GDP series was recently made public. The panel’s calculations suggest growth averaged a tad above 8 percent in the 10 years through fiscal 2014, compared with 7.4 percent since then.

The opposition Congress Party lost no time in pouncing on the report. India’s economy, it said, had fared better under its last Prime Minister Manmohan Singh than it has in the four years of Narendra Modi’s leadership.

How does this history lesson tie in with the outlook for the rupee? Before the GDP back-series, some officials and analysts were beginning to shrug off this year’s 8.3 percent depreciation of the currency, the worst in Asia, as par for the course. The Reserve Bank of India would “let go” of the rupee, Bank of America Merrill Lynch wrote in an Aug. 15 note, “because there is only so much they can do to limit the sell-off.”

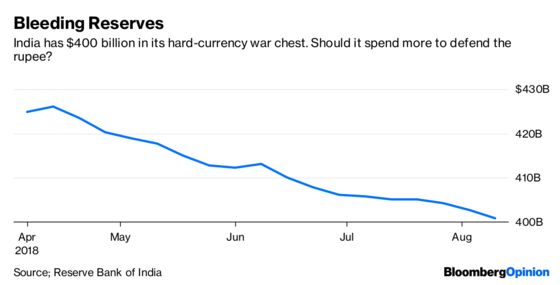

Technically, a hands-off approach may be the right position. The currency may still be overvalued, based on India’s inflation differential with trading partners and rivals. Besides, the nation has already spent $24 billion defending the rupee since April, which is when President Donald Trump’s administration added India to the U.S. Treasury’s monitoring list of potential currency manipulators. While there’s little chance of a country with a current-account deficit actually being punished for manipulation, with Trump you can’t be sure.

Politically, though, Modi can ill afford a laissez-faire stance. Could he allow the Congress Party to claim that the rupee at 80 to the dollar (it’s around 70 at present) is a symbol of the prime minister’s failure to deliver the “good days” he promised in 2014? Modi might have bitten the bullet if he could give his social-media warriors the cover of GDP data that make his performance look good while rendering the previous regime’s record indecipherable.

Now that a direct, unflattering comparison with the past has suddenly sprung up, however, my bet is he can’t let the rupee go. Every milestone in that weakness – 70, 71, 72, 75, 80 – would make him vulnerable to ridicule on Twitter, Facebook and WhatsApp. And that’s one thing no Indian politician who has to fight reasonably fair elections can endure.

Five years ago, Team Modi succeeded with great aplomb in nailing the Singh government with simple but lethal social-media memes around anemic growth, high gasoline prices, a weak rupee and a string of corruption scandals. Now, the Congress Party wants to return the compliment in next year’s elections by using the same narrative of expensive gasoline, a wilting currency and alleged improprieties in the purchase of Rafale fighter aircraft from France’s Dassault Aviation SA.

In the absence of reliable employment data (the Modi administration has stopped surveys), all that was missing from the Congress Party’s attack was clinching evidence that the prime minister’s policies were growth-unfriendly. The subcommittee on past GDP has given it that weapon.

Never mind that the new GDP series is still full of holes. At least now the opposition can stop blaming Modi for fudging data and instead rush to take credit for the 10.8 percent expansion it apparently delivered in fiscal 2011. As for the 5 percentage-point decline in growth on its watch in the two subsequent years, the shocks are reverberating even now. Firms that made bold, debt-financed investment bets in the expectation of rapid economic growth are now being dragged through bankruptcy courts; the banking system is grinding its way through more than $200 billion in stressed corporate loans.

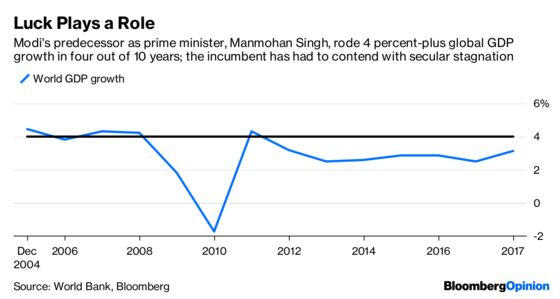

However, that story is too complicated for Modi’s supporters to tell in WhatsApp groups. Good luck to any finance minister who tries to explain on Facebook the not-so-minor detail that world output grew by more than 4 percent in four of the 10 years of Singh’s tenure, while the fastest expansion in the global economy during the Modi years was 3.15 percent in 2017.

Recovering from a major loss in a battle of perceptions isn’t easy. Slapping a note on a published report saying figures aren’t final and should “not be quoted anywhere” – after they’ve been quoted everywhere – only helped highlight the government’s embarrassment. There’s no way Modi can give his detractors still more ammunition by shrugging off a weak rupee.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2018 Bloomberg L.P.