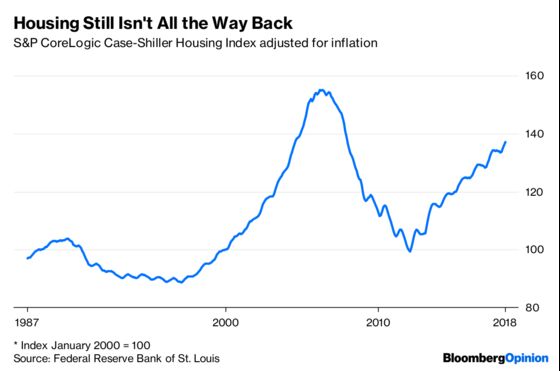

(Bloomberg Opinion) -- The housing market has made a remarkable — if partial — recovery since the disaster that befell it 10 years ago. In the years since the crisis, the market has recouped about two-thirds of the value it lost in the crash:

But unlike in the early 2000s, when housing became a vehicle for broad-based middle-class wealth, today’s bull market is shutting out many lower-earning and younger Americans. This is partly because of policy choices. But it also illustrates some of the pitfalls of relying on housing as the pillar supporting a country’s middle class.

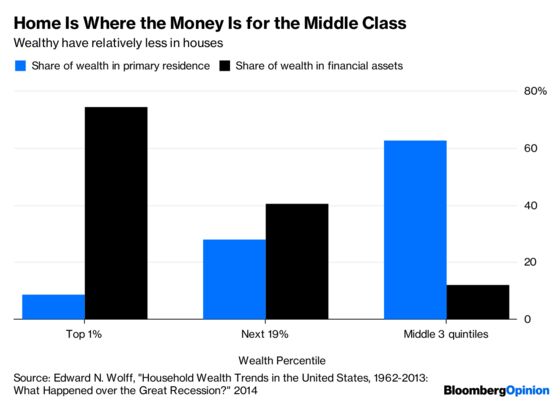

Traditionally, homeownership has been the most reliable path to building wealth in the U.S. Lower- and middle-income Americans tend not to own a lot of stocks — instead, they keep most of their wealth in their houses:

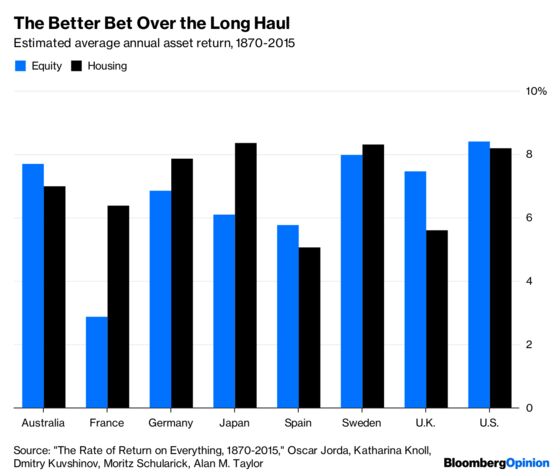

This isn’t such a bad thing, in general. Yes, a house isn’t a diversified investment portfolio — it’s vulnerable to local market downturns, and it’s correlated with one’s job, so having a lot of money tied up in a house is fairly risky. But on the bright side, paying a mortgage is a good way of disciplining yourself to save money at a high and constant rate; over time, saving is the key to building wealth. And although some will claim that houses don’t yield as good a return as stocks, that has only been generally true in the past few decades. Historically, when rental yield is included, real estate has actually done pretty well:

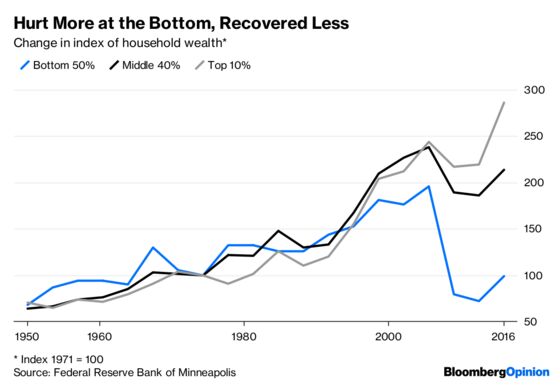

Unfortunately, less affluent homeowners took quite a bath in the housing meltdown and financial crisis. The result for many was the undoing of decades of wealth-building:

Why has the housing recovery not done more to reduce wealth inequality, or to restore wealth for those at the bottom of the distribution?

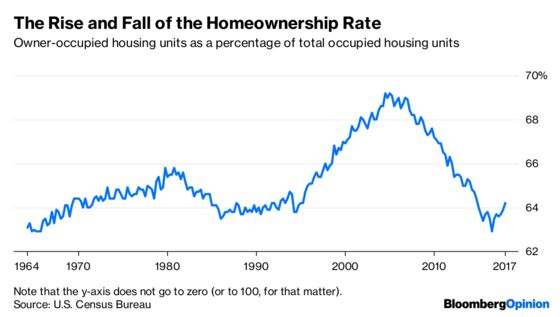

A clue can be found in the lower homeownership rate:

This obviously means that fewer Americans are benefiting from the rise in housing prices than in the early 2000s. But it’s also a reminder of how many people lost their homes in the collapse of the housing bubble. Foreclosure forced many mortgage borrowers to sell at the bottom of the market — now the houses they used to own are in the hands of wealthier people or companies, who are profiting handsomely from the price rebound. The government’s failure to help keep people in their homes during the crisis means that many lower-income Americans are having to start all over again building wealth from nothing.

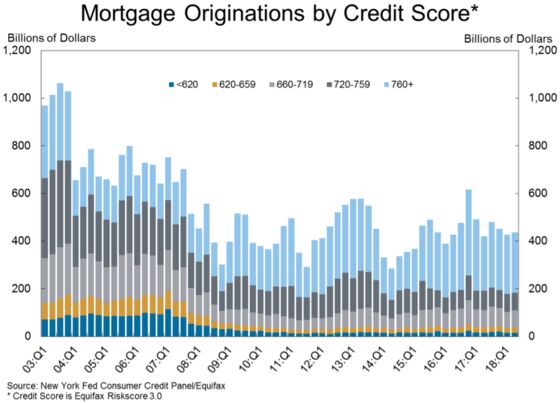

The fall in homeownership also reflects the fact that less creditworthy borrowers have been shut out of the housing market since the financial crisis. The Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit shows that while mortgages for people with higher credit scores have increased, loans for those with less-than-stellar ratings have dried up:

This might be because of post-crisis wariness about lending to subprime borrowers. It might be the inadvertent result of well-intentioned regulation by the Consumer Financial Protection Bureau, which seeks to protect poorer borrowers from predatory mortgage lending. In any case, the decline of mortgage lending to less-creditworthy borrowers means that ownership of the nation’s housing stock is increasingly concentrated in the hands of the wealthy.

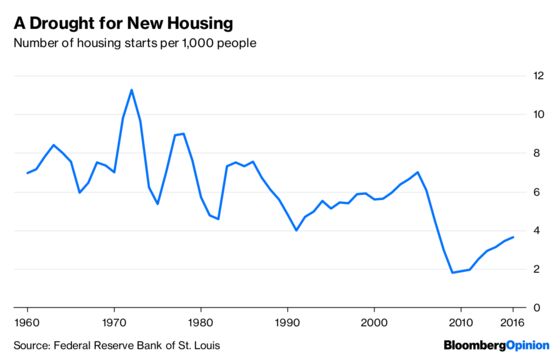

A third reason the housing price recovery isn’t doing much to narrow wealth inequality is that it’s partly due to a restriction in supply. Around the country, there are increasing reports of so-called Nimbys — anti-development interests that say “not in my back yard” to new housing. That story is consistent with the fall in housing starts, which are historically low relative to the country’s population:

Why would Nimbyism become more powerful after the crisis? Homeowners lost a lot of money in the crash — money that they had planned on using for their nest eggs. In order to preserve their retirement savings, it makes sense that many would use their influence over local politics to enact harsh zoning laws, development restrictions and other policies to limit supply and thus force housing prices back up.

But raising wealth by restricting supply is bad — not just for renters, and for local economies, but for people looking to buy into the housing market. When few new homes are getting built, young first-time homebuyers — and people looking to buy back into the market after losing their homes — are forced to bid for the existing housing stock at ever-higher prices. That lets older and wealthier people cash out, but it means that everyone else has to go into greater debt to get in on the ground floor of the American dream.

Nimbyism illustrates the downside of using housing as a nation’s middle-class wealth engine. Local political power tends to be concentrated in the hands of wealthy homeowners, who can use the law to extract even more wealth from the young and the poor. But overall housing wealth isn’t being created, because new housing isn’t getting built — instead, it’s just being redistributed, and in precisely the wrong direction.

Crisis foreclosures and post-crisis Nimbyism are two ways of leaving the middle class with little choice but to buy at the top of the market. The result is a transfer of wealth from the have-nots to the haves. Unless the government can implement policies to radically expand homeownership to the young and those with weaker credit — perhaps by providing matching funds to help them buy houses, coupled with measures to force cities to allow more housing development — then housing will likely continue to fail in its traditional role as the pillar of the American middle class.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.