Turkey Is Following a Familiar Emerging-Market Script

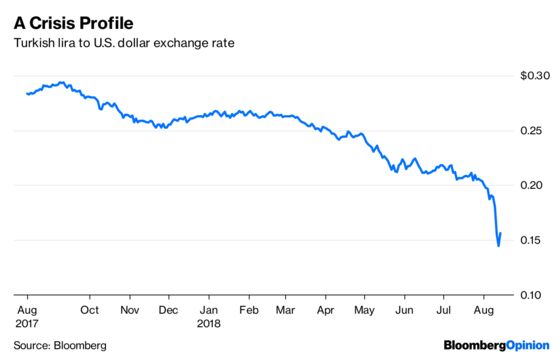

(Bloomberg Opinion) -- As it happens, I went to Turkey this past week for a wedding, rather than to watch an economic disaster unfold. But as luck would have it, I got to do the latter. Just as I arrived the Turkish lira’s value against the U.S. dollar was plunging by more than 20 percent:

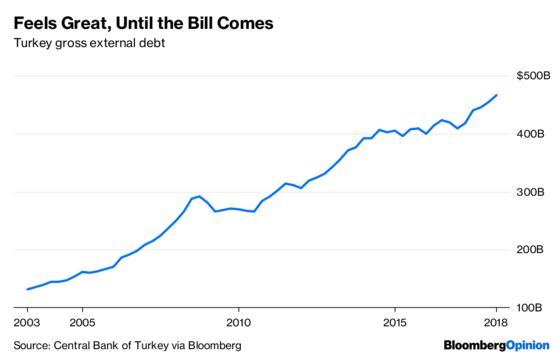

That certainly helped me buy souvenirs for my friends back in the States. And it will be good for Turkey’s tourism industry, as well as exporters of goods such as autos and textiles. But overall, it’s bad news for Turkey. The country has been borrowing a lot of money from foreigners:

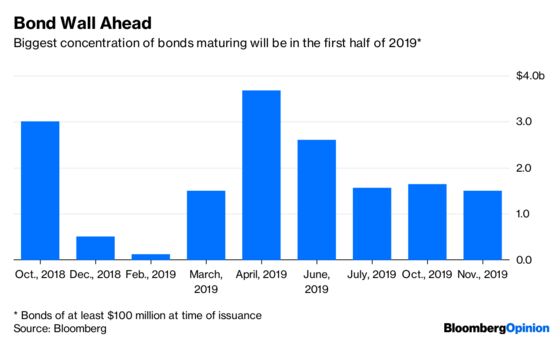

Unlike the U.S., whose government and companies issue bonds denominated in domestic currency, much of Turkey’s borrowing is done in foreign currency. When the lira falls against the U.S. dollar, that makes dollar-denominated debt costlier to repay. Bloomberg News recently reported that at least $16 billion of Turkish foreign currency-denominated bonds are coming due in the next year:

As Paul Krugman noted, this can easily lead to a downward spiral. Unable to pay their dollar- or euro-denominated debt, Turkish companies will go bankrupt, or at least cut back on investment, hurting the economy and causing more people to move their money out of Turkey. That would send the Turkish currency lower, leading to even more waves of defaults and an even bigger slowdown.

That’s the narrative for a type of crisis common to emerging markets. It resembles what happened to Southeast Asian and East European countries in the late 1990s, and to Latin American countries in the 1980s, ’90s, and ’00s. Turkey itself suffered this kind of episode in 2000-01; ironically, that disaster helped bring the current regime to power.

Exactly how these crises happen is a mystery. Economists have tried to explain sudden outflows of capital from emerging markets as coordinated attacks by currency speculators, or herd behavior or a variety of other phenomena. These sudden, catastrophic cascades can be triggered by seemingly minor events — for example, Turkey’s lira plunged after U.S. President Donald Trump made tariff threats against the country as part of an escalating dispute over the jailing of an American pastor. Trump makes tariff threats against a lot of countries, and often walks them back in short order — Turkey just happened to be at a point where an erratic, unreliable signal managed to push it into the danger zone.

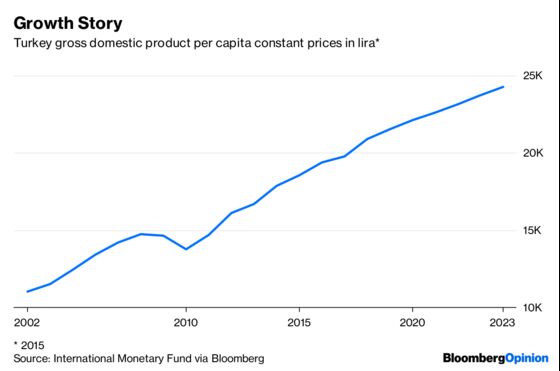

The more important question is why Turkey’s economy was so vulnerable in the first place. On the surface, Turkey’s economy seems to have been doing just fine under its president, Recep Tayyip Erdogan, who served as prime minister from 2003-14. The country’s per capita income has more than doubled in purchasing power parity terms since Erdogan became prime minister:

This happy trend has continued in recent years. Turkey is now an upper-middle-income country, with a per-capita gross domestic product similar to that of Hungary, Greece or Poland. On my trip, the visible signs of growth were everywhere — towering new apartment and office complexes, businesses teeming with customers.

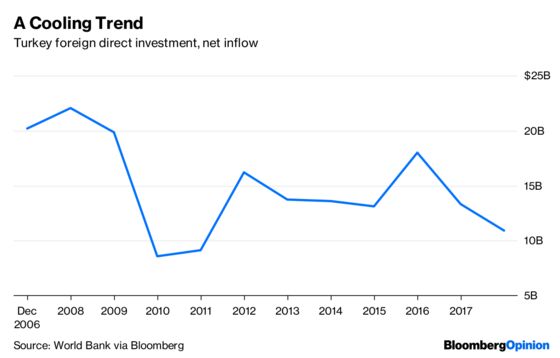

But underneath the surface, there are signs that not all is well. Some Turkish economists have fretted that the growth relies too much on debt, noting that Turkey only started to run big current account deficits after Erdogan’s party came to power. Meanwhile, foreign direct investment has cooled in recent years, suggesting that fewer investors see Turkey’s growth as being driven by real productivity improvements:

Partly to shore up his political popularity after an abortive 2016 coup attempt, Erdogan has committed himself to ever more grandiose construction projects, including a canal through Istanbul and a giant new airport in the city. Just the other day, he promised a huge airport for a city of only 80,000 people. Meanwhile, he has encouraged the real estate industry with a raft of policies, from tax cuts to cheap mortgages to amnesty for illegal construction projects.

The awe inspired by Erdogan’s construction boom is palpable. “None of this was here before Erdogan,” a wedding guest remarked, gesturing at the Istanbul skyline. But borrowing foreign money to fund domestic real estate speculation has never been a sustainable strategy for economic development. There’s a good chance that Erdogan’s megaprojects will turn out to be white elephants, that real-estate speculation will lead to high debt and waves of defaults, and much construction will turn out to be uneconomical.

The currency crisis may well be the start of tough times for Turkey. Capital outflows themselves are manageable with capital controls, as China demonstrated after its 2015 stock market crash. But the longer-term damage of an economy with high debt levels, with too many resources oriented toward real estate and construction, could be harder to escape.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.