(Bloomberg Opinion) -- Foxconn Technology Group turned in a stellar top-line performance last quarter. But the bottom line was a resounding disappointment.

To understand what went wrong, look past the headline numbers and dive into the P&L.

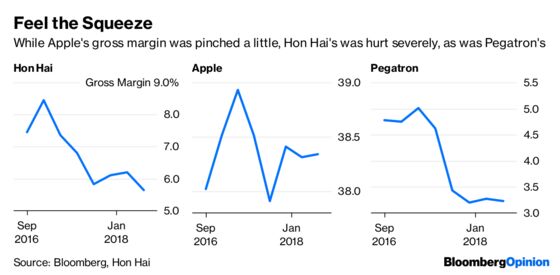

Revenue at flagship Hon Hai Precision Industry Co. climbed 17 percent from a year earlier, in line with the 17.3 percent growth its major client Apple Inc. posted for the same period. Yet Hon Hai’s net income dropped 2.2 percent, missing estimates by 12 percent.

One major upside for Apple was that while iPhone shipments grew barely 1 percent, revenue climbed. That was a function of higher average selling prices, because the tech giant can get away with costlier phones.

The more expensive iPhone exacted a toll, however, as its costs climbed almost the same amount, resulting in a slight squeeze to Apple’s gross margin.

This also played out at Hon Hai, but was magnified: The cost of goods sold, or COGS, rose 18.5 percent. The result was a 117 basis-point shrinkage in Hon Hai’s gross margin, to the lowest level in six years. For a company that lives on the margins, that’s a big squeeze.

Limited growth in actual shipment volume, as seen with the iPhone, can hurt Hon Hai because it means some of its production resources risk lying fallow, and idle hands are the (margin) devil’s workshop. This doesn’t fully account for the pain, though. The fact that Apple was also hurt at the COGS level indicates low factory utilization at its major assembler isn’t an adequate explanation.

It’s worth noting that Hon Hai’s main rival, Pegatron Corp., last week disclosed similar struggles, with revenue up 13 percent but gross margin down by 1.4 percentage points. And that firm can’t blame the iPhone so much.

Instead we need to look further, at what goes into COGS. While labor and depreciation are among the factors, neither is as significant as the prices of components that go into devices. A key plank of Foxconn’s business model is having component procurement flow through its own books, even when the client chooses the parts and negotiates the terms.

But when the price of items like DRAMs, processors and multilayer ceramic capacitors (or MLCCs) climb, even big players like Foxconn and Apple face a pinch.

Hon Hai’s investor relations team wasn’t available to answer questions, and Foxconn Chairman Terry Gou doesn’t brief on the goings-on at his $48 billion empire outside of the AGM. But the financials of other companies help complete the picture.

Yageo Corp. may be the single best example of what’s happening in component land these days. The maker of boring little items like capacitors and inductors (sorry, Yageo) has given investors an exciting ride in the past year. Because of a shortage of parts such as MLCCs, Yageo increased revenue by more than 150 percent in 12 months. That wasn’t just by churning out more, but by charging more – a lot more. From gross margins of 29 percent in the second quarter of 2017 (already well above historical averages) analysts expect the Taipei-based company to turn in an astonishing 66 percent gross margin for the most recent period.

Similar stories of high component prices are are being told across the electronics supply chain. The saving grace for Samsung Electronics Co.’s earnings last quarter was its memory chip division, which offset weakness elsewhere. And according to DRAMeXchange, operating margins of the top-three DRAM suppliers – Samsung, SK Hynix Inc. and Micron Technology Inc. – surpassed 60 percent for the period, a figure the research firm describes as unprecedented.

While it’s important to look at the world’s most valuable company for hints on how the supply chain is faring, it’s wise to look deeper into the machinery.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2018 Bloomberg L.P.