(Bloomberg Opinion) -- It should have been a good day for the euro Tuesday after Eurostat said the euro-area economy grew faster in the second quarter than initially reported. But instead, the Bloomberg Euro Index that measures the shared currency against its major peers fell the most in two months, dropping as much as 0.92 percent. The seemingly illogical response by foreign-exchange traders becomes logical when considering what ultimately moves the currency.

Of course, the euro is more susceptible to fallout from the economic troubles in Turkey than any other major currency, so turmoil there could be having an impact. But it's becoming increasingly clear that the European Central Bank may not be able to bring an end to its currency-debasing quantitative easing measures later this year as planned. That was made clear by remarks Monday by Claudio Borghi, the head of the budget committee in Italy’s lower house. He told Bloomberg News in an interview that the ECB should keep providing a shield to the government securities of all monetary union members to avoid a breakup of the entire euro system. Borghi's comments came as speculators drove up Italy's bond yields on concern the country's fiscal situation will deteriorate on tax cuts and new benefits spending pledged by the populist government. “Either the ECB guarantee will come or everything will be dismantled,” Borghi said in a reference to the euro system. If it comes down to that, it means the ECB will need to keep flooding the financial system with more euros at the risk of overwhelming demand.

The euro has long been dogged by concern among traders that the shared currency could break up at any moment despite an assurance by ECB President Mario Draghi during the height of the euro crisis six years ago that the central bank would do "whatever it takes" to keep it from breaking apart. That could be true, but coming to the aid of Italy and its $2.24 trillion of debt would be a much harder ask than a Greek bailout. Maybe that's why the euro's share of global currency reserves has dropped to 20.4 percent from 24.8 percent at the time of Draghi's pledge.

THE CROWD LOVES U.S. STOCKS

Barring some calamity, the bull market in U.S. stocks is one week away from becoming the longest in history. The current rally started on March 9, 2009, with the S&P 500 Index gaining 320 percent, not including dividends. If the S&P 500 is able to make it to Aug. 22 without collapsing, the current bull market will swipe away the top spot from the one that lasted between October 1990 and March 2000 and delivered about a 400 percent return to investors. Perhaps the most remarkable thing about the current rally is that investors are getting more confident in U.S. equities. A monthly survey of 243 investors with a total $735 billion under management by Bank of America Merrill Lynch found that allocations to U.S. stocks jumped 10 percentage points in August to a net 19 percent overweight, the highest since January 2015. That makes America the most popular equity region for the first time in five years, according to Bloomberg News's Natasha Doff, citing the firm’s analysts. A net 67 percent of recipients said the U.S. was the most favorable region for corporate profit expectations, the highest proportion in 17 years. Even so, there's no shortage of high-profile market mavens suggesting caution. "If there were ever a moment to harvest gains and reduce risk, it is August 2018,” Scott Minerd, the chief investment officer at Guggenheim Partners, wrote in a Twitter posting Tuesday. "And if it turns out not to be the moment, I don’t think you are giving up much upside.”

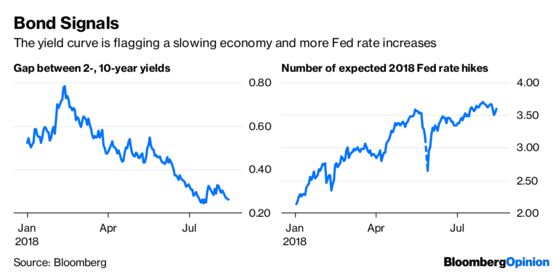

NEGATIVE BOND SIGNALS

The other thing that’s so remarkable about the level of bullishness toward U.S. stocks is the signals being sent by the bond market. After a brief and moderate steepening in late July, the so-called yield curve has started to flatten again. The difference between two- and 10-year Treasury note yields contracted to 26 basis points on Tuesday and is less than two basis points away from the low for the year set on July 17. The narrower it gets, the more likely the economy is in for a big slowdown — at least going by historical performance. And an inversion, where long-term yields fall below short-term yields, is a reliable predictor of recessions. Some investors and strategists believe that an inversion is inevitable as long as the Federal Reserve keeps raising interest rates. But wouldn't the turmoil in emerging markets cause the Fed to pause? Not necessarily, according to FTN Financial chief economist Chris Low. "The Fed’s models do not include international variables," Low wrote in a note to clients Tuesday. "As long as they are focused on stabilizing the U.S. unemployment rate, they will hike until growth slows significantly, or until the international situation is bad enough to have a significant impact on U.S. markets." Traders are pricing in 1.6 more Fed rate hikes by year-end, which is little changed over the past three months.

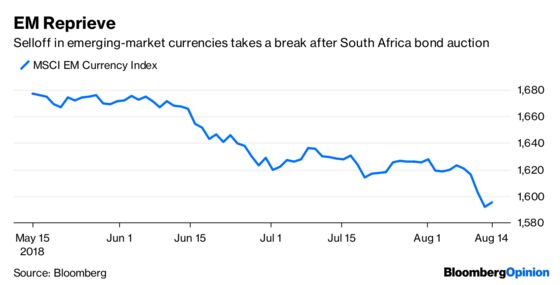

SOUTH AFRICA TO THE RESCUE

For the first time in what seems like weeks, emerging markets were relatively calm on Tuesday following a Turkey-induced sell-off Monday that roiled financial assets worldwide. While the respite gave investors a chance to mull whether the recent turmoil in developing nations has the potential to develop into a full-blown crisis, one event Tuesday gave credence to the idea that it won't. Despite the fact that South Africa's rand is one of the three worst-performing major currencies since the end of March, the nation was still able to draw big demand for bonds it offered on Tuesday. Traders placed 9.77 billion rand ($694 million) of orders, or more than four times the 2.4 billion rand of securities on sale, at the scheduled weekly Treasury auction, according to data published by the central bank. That marked the strongest demand at a South Africa bond auction since March, according to Bloomberg News's Robert Brand and Colleen Goko. "It feels like the contagion risk is fading a bit," Delphine Arrighi, a money manager at Old Mutual Global Investors in London, told Bloomberg News. "Some of the re-pricing we have seen in the last two days seemed overdone" for some markets, she said. South African bonds due in 2026 have lost 11 percent this month in dollar terms, the worst performance after Turkish debt, which is down 36 percent, according to Bloomberg Barclays indexes.

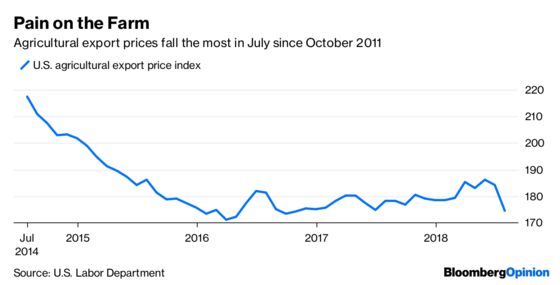

PROOF OF AGRICULTURE PAIN

Traders have been driving down the price of agricultural products for much of the past three months on concern about the fallout from a budding global trade war. The Bloomberg Agriculture Subindex is down about 12 percent since late May. The data is starting to show that those concerns were justified. Prices for U.S. farm exports dropped in July by the most in more than six years as a trade war with China heated up, Labor Department figures showed Tuesday. Agricultural export prices fell 5.3 percent from the prior month, the biggest drop since October 2011, as soybean prices plummeted 14.1 percent, according to Bloomberg News' s Jeff Kearns. Export prices for corn, wheat, fruits and nuts also slumped in July. The overall export price index dropped 0.5 percent, the most since May 2017, the department said. The figures exclude the price effect from any tariffs. China slapped 25 percent tariffs on American soybeans in July and also targeted other farm goods in retaliation for U.S. duties on a range of merchandise. The world’s biggest buyer of soybeans has shunned U.S. supplies amid the escalating trade conflict, threatening to curb exports after the harvest.

TEA LEAVES

Fans of U.S. economic data will have quite a day on Wednesday. Among the flood of reports due to be released are those for retail sales, industrial production, business inventories, housing and foreign demand for American financial assets. The one that is likely to get the most attention is retail sales, which will provide some insight into the health of the consumer a day after a Federal Reserve Bank of New York report showed that U.S. household debt rose 3.5 percent in the second quarter from a year earlier to a record $13.3 trillion. The median estimate of economists surveyed by Bloomberg is for retail sales to have risen 0.1 percent in July from a year earlier, down from a 0.5 percent gain in June. Excluding autos and gasoline purchases, sales likely increased 0.4 percent. "While the weakness — and possible contraction — in headline retail sales will be distorted by autos, the underlying trend will nonetheless support Bloomberg Economics’ estimate for consumer spending to moderate in the current quarter following a gangbusters second quarter," Bloomberg Economics' Carl Riccadonna and Tim Mahedy wrote in a research note.

DON'T MISS

Bond Market Says Fed Isn't World's Central Bank: Brian Chappatta

Yale Researchers Jump the Gun on Crypto Winners: Aaron Brown

Indonesia’s Tough Love Won’t Crisis-Proof the Rupiah: Shuli Ren

Will This Buyout Embarrass the Stock Market?: Chris Hughes

India Can't Afford to Turn Its Back on Free Trade: Mihir Sharma

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.