(Bloomberg Opinion) -- There are some politicians in the Italian government who dream of escaping the economic shackles that accompany membership of the euro and the European Union. The nightmare currently engulfing Turkish assets should be a warning that freedom isn't all it's cracked up to be.

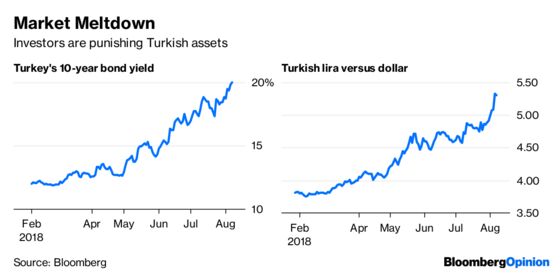

Turkey's currency has lost almost a third of its value against the dollar in the past six months and dropped to a record low this week. The nation’s 10-year borrowing cost touched 20 percent on Tuesday as traders judged insufficient the central bank’s efforts to stem the lira's slide by modifying reserve requirements.

Turkish assets are getting crushed by the combination of a diplomatic showdown with the U.S. over a detained American pastor that could lead to economic sanctions, and a fast-deteriorating economic backdrop. A fight between the government and the central bank over monetary policy that's been going on for months has accelerated outflows.

Turkish President Recep Tayyip Erdogan is vehemently opposed to the higher interest rates that a truly independent central bank would probably introduce to combat inflation running at the fastest pace in 15 years. The speed of the lira's descent, though, has investors rightly concerned that the nation may be forced to introduce capital controls or seek a bailout from the International Monetary Fund – or both.

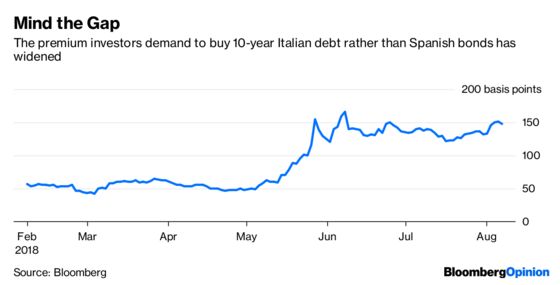

Now, Italy isn’t Turkey. But the tension between members of Italy's coalition government about how to run the economy has made investors increasingly wary of Italian bonds.

Italy's 10-year borrowing costs averaged 2 percent in the first quarter of this year; they rose to 2.6 percent in the past three months. And, as the spread to Spanish yields shows, the increase is mostly due to investor mistrust of the recently formed government rather than concern about the European Central Bank's planned halt to its bond-purchase program.

The coalition has advocated populist economic policies that could cost more than 100 billion euros ($116 billion), including a flat tax, a citizen's income and a lower retirement age. Finance Minister Giovanni Tria has pledged to honor EU rules that limit budget deficits to 3 percent of gross domestic product.

But those rules aren't "the Bible," Deputy Premier Matteo Salvini, leader of the League party, said in an interview published Monday. "The budget parameters can't be a way to say we can't do it," his coalition partner, Deputy Premier Luigi Di Maio, who heads the Five Star Movement, said that day.

The pre-election worries that the incoming government would seek to take Italy out of the euro have faded. But if its politicians prove willing to go to war with EU partners in drafting a populist budget that breaks the rules, investors will demand ever-higher premiums for lending to the country.

Again, Italy isn't Turkey. But the surge in Turkish borrowing costs is a reminder that when your debts are worth more than 130 percent of gross domestic product – as is the case with Italy – you depend on the kindness of strangers to keep buying your bonds. And investors get to vote on your economic policies not just at election time, but every day.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2018 Bloomberg L.P.