(Bloomberg Opinion) -- Not so long ago, Singapore’s biggest bank used to be gung-ho about its trading operations. So much so that when DBS Group Holdings Ltd. moved its headquarters of nearly four decades, it made sure the dealing room was 40 percent larger.

It must have been a rather empty hall in the June quarter.

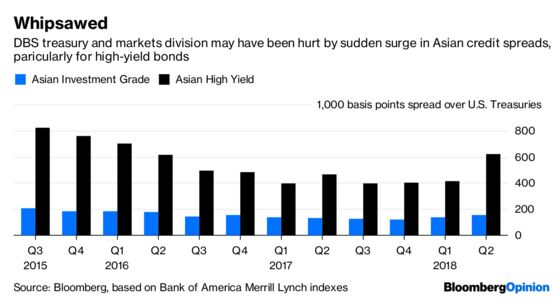

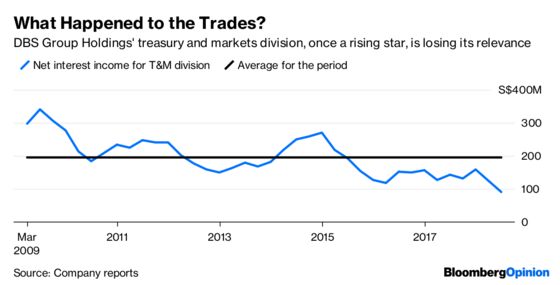

Net interest income of just S$91 million ($66 million) in treasury and markets, not even half of the division’s quarterly average for the past 10 years, can be blamed partly on flat yield curves, which crimped the “carry” – the profit potential of holding longer-dated securities by borrowing short-term funds. A ballooning of Asian credit spreads, triggered by U.S.-China trade tensions, could also have contributed to the division’s S$50 million loss, a big swing from a S$112 million pretax profit in the previous quarter.

However, given that the decline in treasury and markets is not a flash in the pan (interest income of the division has been steadily ebbing for more than three years), there could be more structural forces at play here.

Let’s call it the shadow of robots – or trading algorithms.

As Nisha Gopalan and I wrote last month, with the “flow” business of trading bonds, stocks and foreign-exchange for clients comprising 51 percent of investment banks’ global markets revenue of $109.8 billion last year, automation of even vanilla trades is no small risk. DBS’s earnings report is an indication of that threat even for commercial banks that have sizable trading operations.

The core banking business, meanwhile, is in good shape. Customer loans grew 12 percent from a year earlier in the quarter, even as the net interest margin swelled to 1.85 percent – an 11 basis-point improvement. The bad-loan problem of 2016 is now in the rear-view mirror.

Still, DBS shares fell as much as 3 percent after the bank pruned full-year loan growth guidance to between 6 percent and 7 percent, from 8 percent. That’s partly because of the unexpected property cooling measures recently announced by Singapore, but mostly because CEO Piyush Gupta is now more pessimistic on trade loans.

Singapore’s state-owned investment firm Temasek Holdings Pte has now heard two dramatically different assessments of the consequences of a global trade war from two of its banks. Temasek has a little more than 29 percent of DBS and is also the third-largest shareholder in Standard Chartered Plc, whose CEO Bill Winters said rising tariffs were “no big deal for us” and may even be a good thing in the medium term.

Whom should Temasek boss Ho Ching believe? DBS bumped up the dividend for the first half of the year by a staggering 82 percent. Meanwhile, StanChart’s first interim dividend since 2015 fell short of expectations this week. Maybe Winters should walk his optimistic talk by writing bigger checks?

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2018 Bloomberg L.P.