The Walking Dead Are Reincarnated at Credit Suisse

(Bloomberg Opinion) -- Credit Suisse Group AG was not long ago ranked alongside Deutsche Bank AG as a basket-case bank whose CEO was a possible “dead man walking.” Yet Tidjane Thiam has shaken off that prognosis by essentially copying his Swiss rival UBS Group AG. He’s shrunk his firm’s trading unit to focus on wealth management, all while cutting costs. And it’s paid off. The difficult thing will be finishing the final leg of his turnaround without any nasty surprises.

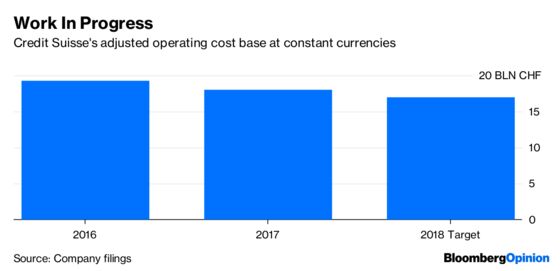

Credit Suisse’s second-quarter performance showed the recovery in full flow, with results beating expectations pretty much across the board — although analysts have been lowering the bar over the past few months. Thiam has slashed expenses and jobs without harming growth. Net revenue rose 7.5 percent, to 5.6 billion Swiss francs ($5.7 billion), even as costs fell. This is what investors like to see.

The wealth-management arm wasn’t immune to some of the rich-client jitters seen at rival banks, with transaction revenues taking a hit at home and abroad. But higher interest income and lower expenses lifted profit, and the bank’s ability to suck in money from wealthy customers hasn’t been dented. On an annualized basis, net new assets increased by 6 percent in the first half, which helps offset pressure on margins.

And while the investment bank’s trading division performed worse than its Wall Street peers, with net revenues falling 6 percent, the capital markets and advisory part of the business reported its best quarterly revenue in years. Thiam’s strategy involves allocating less capital to traders and more to advisory bankers and wealth managers. That seems to be paying off, even at a time of global political tensions over trade.

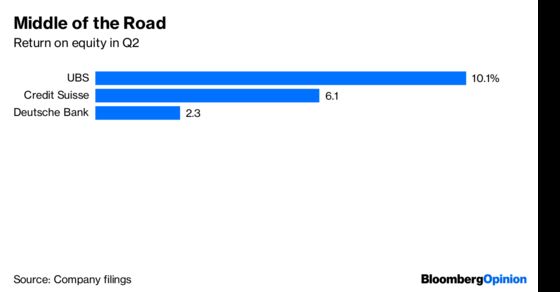

The catch, as always with Credit Suisse, is profitability. Return on tangible equity in the first half was 7.2 percent, higher than the year-ago figure of 5 percent, but well below its 2019 target of 10 to 11 percent. Thiam is clear on what’s still to do: Reduce the bank’s stock of unwanted assets that drag on earnings, and keep cutting costs. These are achievable targets, but much could happen over the next year to make the environment tougher.

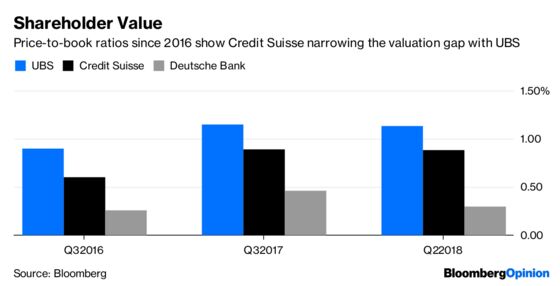

Investors have rightly rewarded Thiam for restoring some shareholder value, especially when compared with other recovery stories like Deutsche Bank. Credit Suisse trades at a 10 percent discount to book value, compared with Deutsche Bank's much steeper 70 percent. But returns aren’t yet at a UBS level, which trades at a 10 percent premium. After three straight annual losses, Thiam has yet to build up a track record of returning cash to shareholders.

Reports of Thiam’s demise were premature, but living isn’t so easy either.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering finance and markets. He previously worked at Reuters and Forbes.

©2018 Bloomberg L.P.