(Bloomberg Opinion) -- Energy trading houses often seem to be the equity market’s equivalent of hand-made watches: exclusive, available only to the super-wealthy, oddly low-margin, and made in Switzerland.

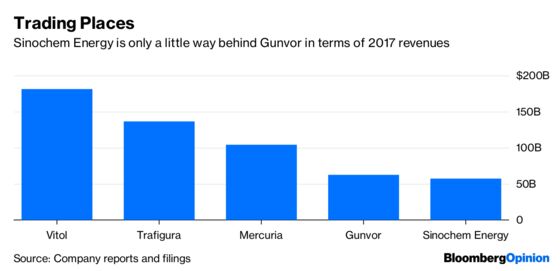

So the impending initial public offering of China’s state-owned Sinochem Energy Co. might appear reason for excitement. Like the traditional big beasts of the business — Vitol Group, Trafigura Beheer BV, Mercuria Energy Group Ltd. and Gunvor Group Ltd. — it’s been veiled in the secrecy of a closely held company. The 571-page filing posted to the Hong Kong exchange Monday offers a rare chance to look at its books.

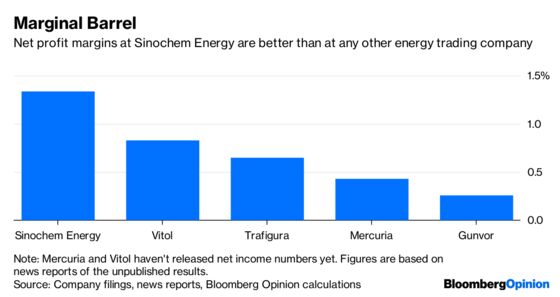

At first blush, it looks appealing. Commodity traders typically operate in wide-open competitive markets where margins are thin as paper — one reason why they have to transact in such enormous volumes to make any money at all. Vitol’s reported $1.5 billion of net income in 2017 was just 0.8 percent of its $181 billion revenue, and still represented the best margin among the big four European traders — but Sinochem Energy is carving out 1.3 percent.

That may not sound like much, but set against 392 billion yuan ($57 billion) of revenue, it comes to some 5.32 billion yuan of net income a year — enough to give the unit of Sinochem Corp. a market capitalization in the range of $10 billion if it was valued on the average of the price-earnings multiples applied to Glencore Plc, Archer-Daniels-Midland Co. and Bunge Ltd.

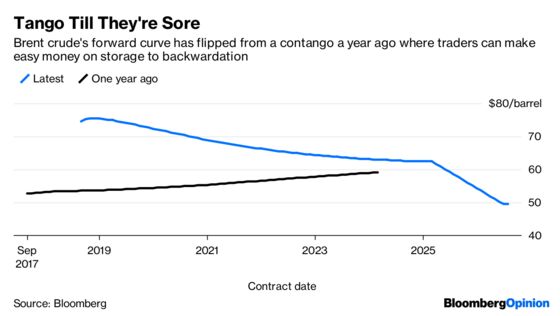

So what’s not to like? For one thing, business has been tough for energy traders of late. One of the easiest ways to make money — hoarding crude in your storage facilities and crude carriers and selling at higher longer-dated futures prices — has flipped into reverse, with all but the nearest-dated crude contracts now in backwardation, the anomalous condition where nearer-term contracts are the costlier ones.

Profit at Vitol fell about 25 percent in 2017, a person familiar with the results told Andy Hoffman and Javier Blas of Bloomberg News in March, while at Gunvor it dropped 49 percent. At Trafigura, net income slumped 53 percent from a year earlier in the six months through March.

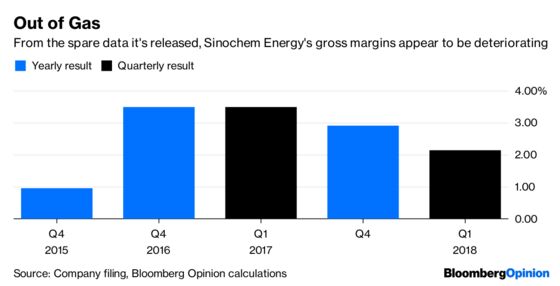

Sinochem Energy doesn’t seem to have escaped: In the three months through March, net income came to 1.21 billion yuan, 46 percent below the same period a year earlier, according to Monday’s filing. The biggest factor looks to have been a deterioration in gross margin, to 2.1 percent from 3.5 percent a year earlier.

Of course, the elephant in the room is that Sinochem Energy isn’t just another energy trader — it’s an energy trader operating in China. That might go some way toward explaining those normally handsome margins. The costs of petroleum products in China are regulated by the government with an eye on market prices, so the money that Sinochem Energy gets for its refinery products (and, by extension, the price at which it sells crude to domestic refiners) is determined by Beijing.

That may look like a benefit, but it contains the seeds of a major problem. One other reason that commodity traders tend to be closely held is managers are less likely to carry out trades that enrich themselves while piling risks onto the balance sheet when they’re also the owners of the company. (Have a look at the travails of Noble Group Ltd. for an example of how badly things can go wrong when the incentives of managers and shareholders aren’t aligned.)

At Sinochem Energy, that principal-agent problem is compounded: Shareholders don’t just have to worry about the incentives of managers, but of the party and state bosses who are ultimately in charge.

It doesn’t add up to an altogether reassuring picture. Sinochem Energy’s most recent quarter was dreadful, forecasts for future earnings are absent, and plans for how shareholders’ cash will be invested are — how shall we say it? — a little threadbare:

Spinning off this trading business may speed the ambitions of Sinochem boss Frank Ning in creating a giant merged chemicals company with China National Chemicals Corp. or ChemChina (itself deeply entangled with Mercuria), but appealing to investors appears to have been an afterthought.

Monday’s filing is a preliminary attempt to sell this deal to shareholders. Sinochem Energy’s advisers will need something a bit more convincing than what’s been presented so far if Ning hopes to get a good price.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.